Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

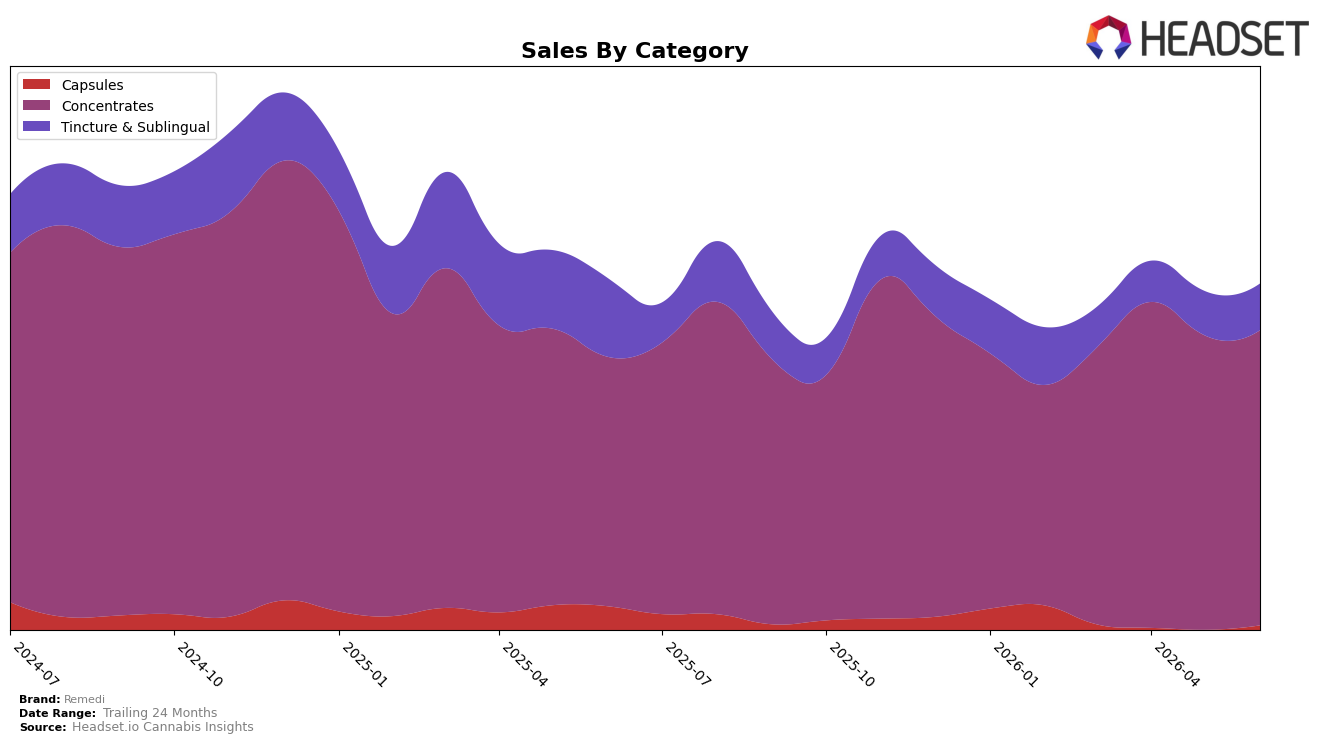

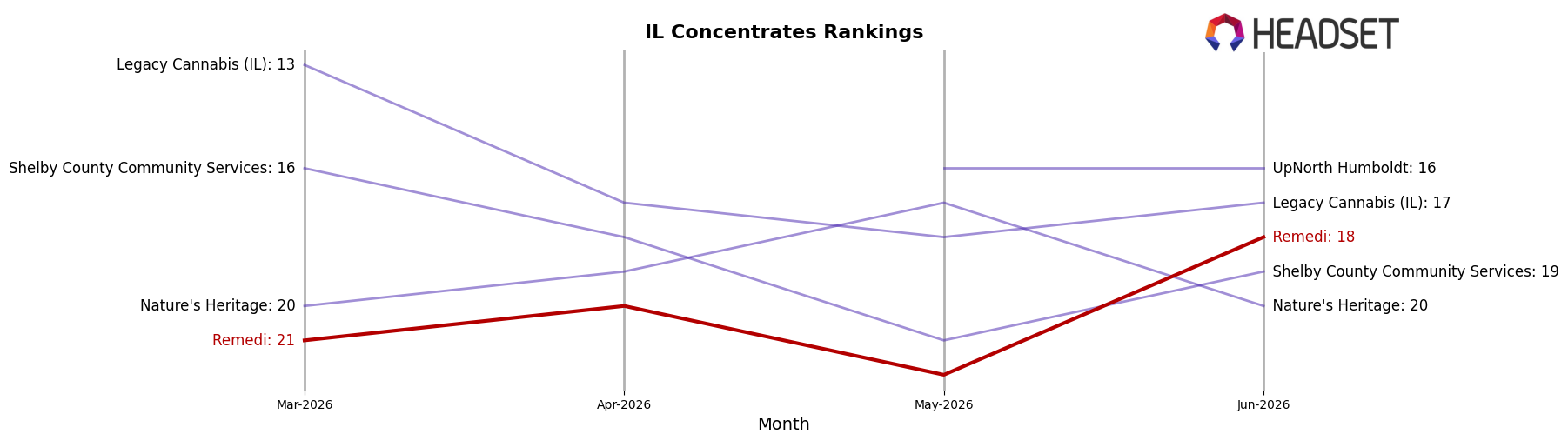

Remedi’s mix in June 2026 is concentrated in Concentrates at 83.34% share with year-over-year growth of 18.05% and month-over-month growth of 0.24%, while Tincture & Sublingual holds 14.17% share with a year-over-year decline of 38.46% but a month-over-month gain of 4.88%. Capsules represent 2.49% share after a 68.12% year-over-year decline yet a 96.32% month-over-month surge, indicating a small base rebound; paired with an 11.86% year-over-year decrease in average price and a 1.41% year-over-year drop in total brand sales, the mix shift concentrates volume into a growing flagship while secondary formats contract. In Illinois Concentrates, Remedi sits at rank 18, and this rank alongside the 18.05% category growth implies the brand’s category-led gains are not fully translating into share capture at the market level.

The pattern suggests positioning anchored to Concentrates that is benefiting from category momentum but constrained by price compression, as the 11.86% average price decline outpaces the 1.41% sales decline and leaves headroom for mix-led volume without commensurate value growth. The month-over-month 96.32% uptick in Capsules against a 4.88% rise in Tincture & Sublingual, combined with a 0.24% lift in Concentrates, implies trial or promotional elasticity at the margins rather than durable share movement; holding rank 18 in Illinois Concentrates while Concentrates’ share stands at 83.34% indicates a need to translate category strength into rank acceleration, or diversify selectively to stabilize against the 38.46% year-over-year drag in Tincture & Sublingual.

Competitive Landscape

Remedi ranks #18 in Illinois Concentrates in June 2026, improving 2 positions year over year from #20 and rising 3 spots from #21 in March 2026, marking a peak rank at #18 in June 2026. By contrast, IC Collective climbed from #7 to #3 with a 37.7% year-over-year sales increase, while Cresco Labs advanced from #9 to #5 on 43.4% year-over-year sales growth, indicating faster upward mobility than Remedi’s 2-rank year-over-year gain. Meanwhile, Aeriz held #1 year over year with a 3.2% sales increase and RYTHM stayed at #2 with 4.1% year-over-year sales growth, suggesting that stability at the top coexists with mid-tier acceleration that could compress space around #18. The pattern implies Remedi’s incremental rank improvement is occurring amid quicker advances by adjacent competitors, signaling that sustaining momentum will likely require gains exceeding a 2-position year-over-year climb to defend or improve its current #18 placement.

Notable Products

CBD/THC 1:5 Rest Capsules 20-Pack (20mg CBD, 100mg THC) posted the standout move in June 2026 with an 87.8% month-over-month gain and a jump into rank 8, while the CBD/THC 1:1 Relief Tincture (50mg CBD, 50mg THC, 30ml) fell 26.9% MoM at rank 7. Indica Relief RSO Syringe (0.5g) also declined 16.0% MoM at rank 2 even as Indica Rest RSO Syringe (0.5g) rose 12.8% MoM at rank 1, indicating divergence within adjacent RSO formats. With eight of the top ten SKUs in Concentrates and the lead SKU generating $32,937, the mix tilts toward RSO-led demand with selective traction in wellness formats, implying Remedi’s commercial direction favors core RSO dominance while testing higher-THC CBD blends for incremental growth.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.