Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

IC Collective is stocked at 175 licensed dispensaries across Illinois and Oklahoma, 166 of them in Illinois, with the deepest coverage in Chicago, Springfield, Normal, East Peoria, and Addison. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

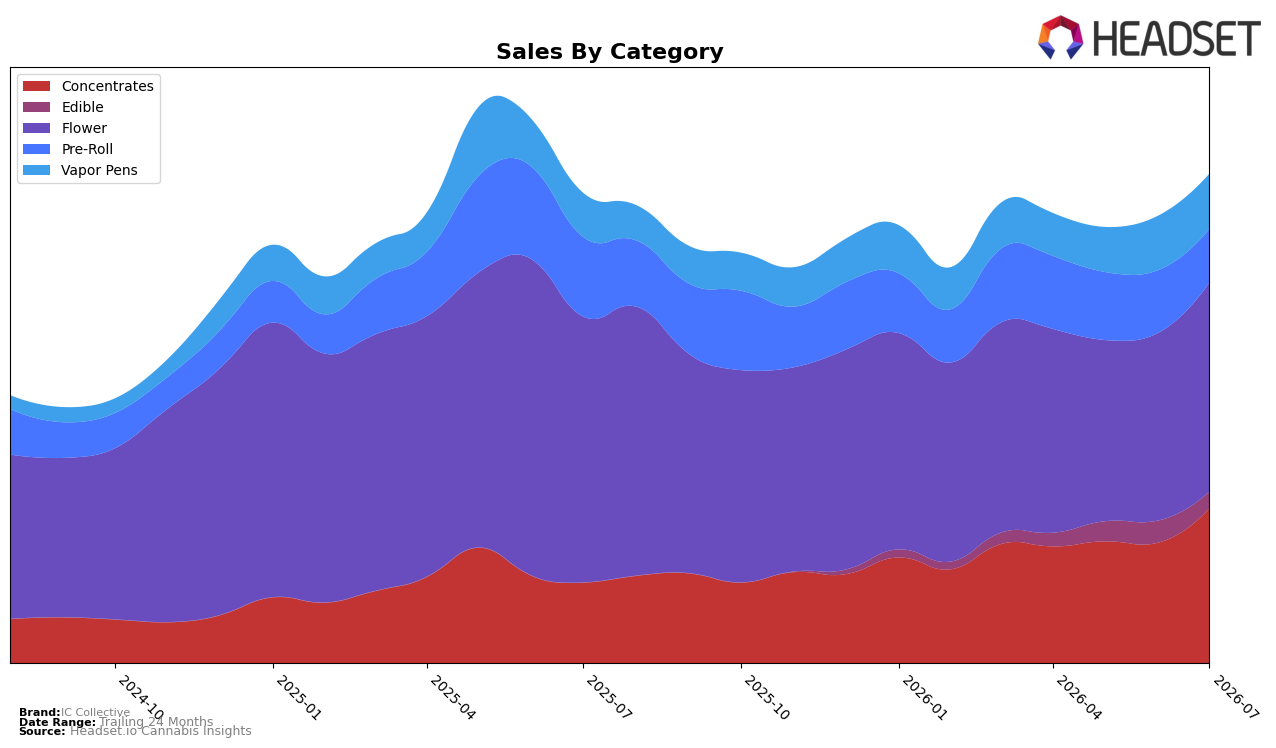

In July 2026, IC Collective’s category mix tilted toward higher-potency formats as Concentrates surged 93.1% year over year and 28.7% month over month to 31.7% share, while Flower, though still the largest at 42.8% share, fell 21.3% year over year and rose 11.6% month over month. Vapor Pens added steady volume with 25.2% year-over-year growth and 1.35% month-over-month growth to 11.2% share, whereas Pre-Roll contracted sharply with a 32.8% year-over-year decline and a 14.6% month-over-month drop to 10.9% share. With the brand’s average price down 0.38% year over year alongside a 4.1% year-over-year increase in total sales, the mix shift implies volume-led gains centered on concentrates and away from pre-rolls, positioning the brand to lean into potency-forward segments while maintaining its Flower base.

The pivot toward Concentrates and incremental Vapor Pen growth, combined with Flower’s 11.6% sequential rebound and IC Collective’s rank of 25 in Flower in Illinois, suggests a barbell positioning: defending mid-tier Flower rank while scaling higher-velocity extracts. The 25.7% month-over-month pullback in Edibles and the 14.6% month-over-month contraction in Pre-Roll reduce exposure to lower-priced, convenience-led formats, indicating a strategy that concentrates assortment and promotional intensity where elasticity supports share gains; this mix should reinforce differentiation in extraction-led SKUs while relying on Flower primarily for traffic rather than growth.

Competitive Landscape

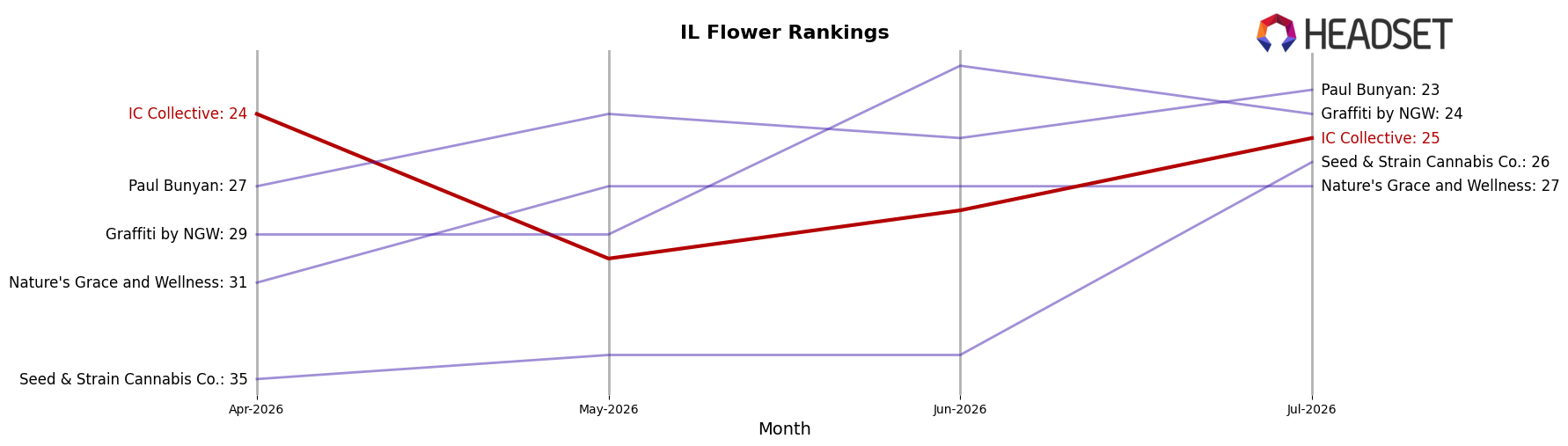

IC Collective is currently ranked #25 in Illinois Flower in July 2026, down 5 positions year over year from #20, and it slipped 1 spot versus April 2026 when it was #24; despite a historical peak at #18 in June 2025, the brand has not reclaimed a top-20 slot. In contrast, High Supply / Supply held #1 year over year and remains #1 even with a 3.05% YoY sales decline, while RYTHM stayed at #2 with 20.81% YoY growth; further updraft came from &Shine, which climbed from #8 to #4 alongside an 87.44% YoY sales increase. The combination of a 5-rank YoY slide and a 1-rank drop since April 2026, alongside competitors holding or gaining top-5 positions, implies IC Collective is ceding relative position and must reverse share loss to avoid further rank compression.

Notable Products

T.I.T.S.(3.5g) posted the standout move in July 2026 with an 85.6% month-over-month surge to rank 1, while T.I.T.S. Pre-Roll (1g) plunged 67.5% to rank 6. OMFG (3.5g) held rank 2 with an 8.6% lift, contrasted by I.C.K.O. Pre-Roll (1g) dropping 19.1% at rank 9. With three Flower SKUs in the top ten and Pre-Rolls spanning ranks 3, 4, 6, and 9, the split between rising Flower and declining Pre-Rolls implies IC Collective is concentrating demand and margin on packaged Flower over single-gram Pre-Rolls.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.