Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Cresco Labs is stocked at 728 licensed dispensaries across Illinois, Michigan, and 6 other states, 191 of them in Illinois, with the deepest coverage in Chicago, East Peoria, Naperville, Normal, and Peoria. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

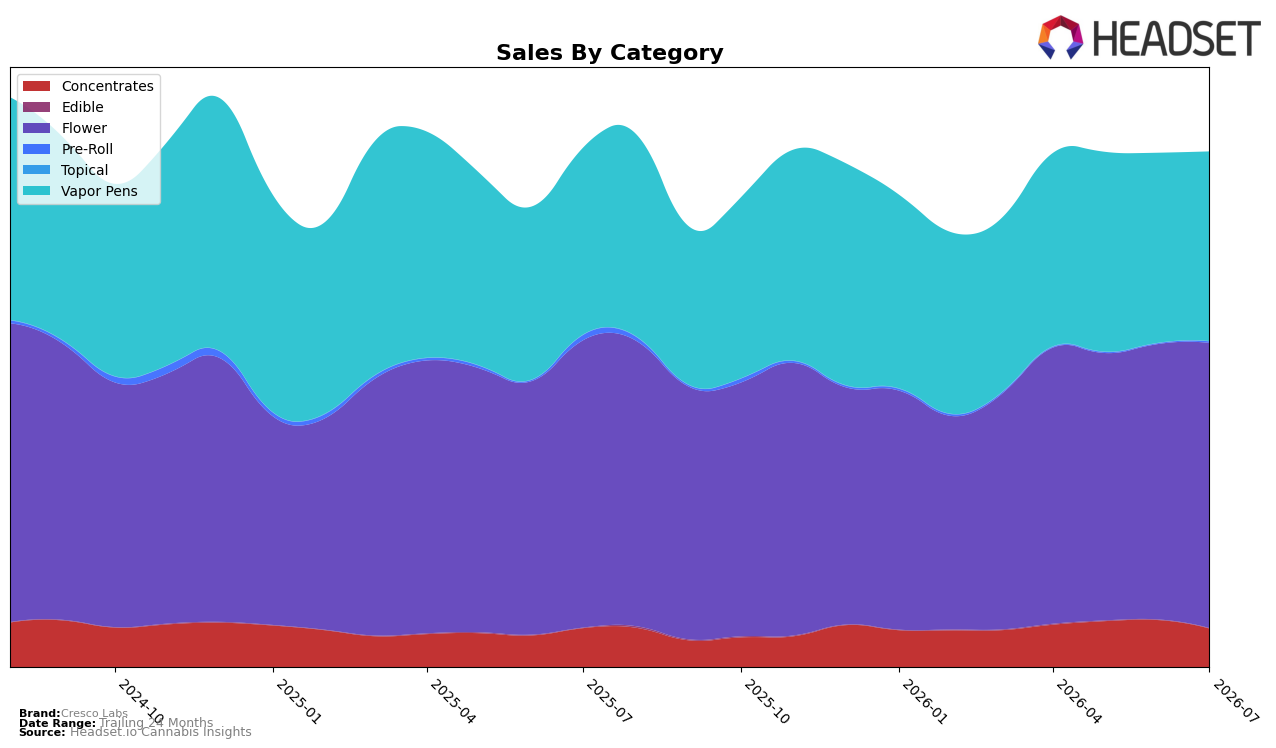

Cresco Labs concentrated 55.41% of July 2026 sales in Flower with a month-over-month increase of 3.53% despite a year-over-year decline of 76.66%, while Vapor Pens held 36.83% share with 1.42% year-over-year growth and a 0.26% month-over-month dip. Smaller lines moved sharply: Concentrates at 7.47% share fell 18.04% month over month and 88.70% year over year, and Pre-Roll, though only 0.25% share, jumped 114.24% month over month after a 74.50% year-over-year drop; Edible, at 0.04% share, declined 31.88% month over month and 32.40% year over year. With an average price down 21.14% year over year to $23.67 and Flower anchoring mix while Vapor Pens provide the only year-over-year growth, July 2026 points to a portfolio leaning on low-priced Flower for volume while premium-adjacent formats lack momentum.

The category shifts imply a defensive repositioning toward value-led inhalables: Flower regained short-term velocity (ranked 7th in Massachusetts Flower) as prices compressed 21.14% year over year, while Vapor Pens sustained 1.42% year-over-year growth without mix expansion, signaling a ceiling under current pricing. Steep pullbacks in Concentrates (down 18.04% month over month) and the micro-scale Edible share at 0.04% indicate deprioritization of niche formats, whereas the Pre-Roll rebound of 114.24% month over month from a 74.50% year-over-year trough suggests opportunistic re-entry rather than durable scale. Net, the brand’s positioning tilts toward defending share in Flower and maintaining relevance in Vapor Pens, with constrained risk-taking in minor categories limiting upside beyond rank 7 in Massachusetts.

Competitive Landscape

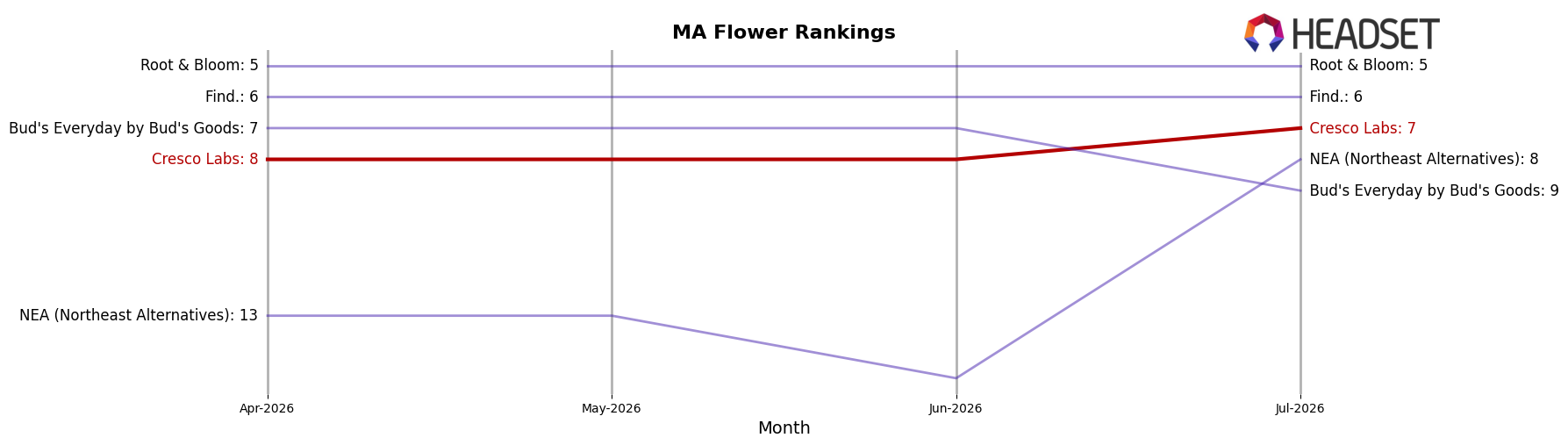

Cresco Labs sits at rank #7 in Massachusetts Flower in July 2026, a 13-position climb from #20 year over year, and a 1-spot improvement from #8 three months ago; this July 2026 position also matches its peak rank of #7, while the category leader Farmer's Cut advanced from #4 to #1 as its sales rose 56.7% year over year, and High Supply / Supply moved up from #2 to #4 despite a 19.1% sales lift. Against mid-tier gains such as Root & Bloom jumping from #10 to #5 on 118.9% growth and Perpetual Harvest edging from #3 to #3 with 36.9% growth, Cresco Labs’ ascent into the top 10 and tying its peak rank suggests the brand is regaining share but must convert the upward trend into further rank gains to avoid being boxed out by faster-rising peers.

Notable Products

OG Mojito (3.5g) posted the headline move with a 290% month-over-month surge to $150,414 and jumped to rank 1, while Bubblez (3.5g) fell 45% and slid to rank 4. Pineapple Express (3.5g) declined 17% at rank 10, contrasted by Pineapple Under The Sea (3.5g) up 44% at rank 3, indicating divergent traction within similarly themed flavor lines. Eight of the top ten are Flower SKUs, and Afghani Kush (3.5g) debuted at rank 2 as Kush Cream (3.5g) entered at rank 6, concentrating gains in core eighths while smalls and cross-weight formats remained peripheral. The pattern implies Cresco Labs is leaning into a hit-driven Flower lineup where breakthrough launches can rapidly reshuffle the leaderboard, suggesting portfolio bets on a few scalable strains over broader SKU proliferation.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.