Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

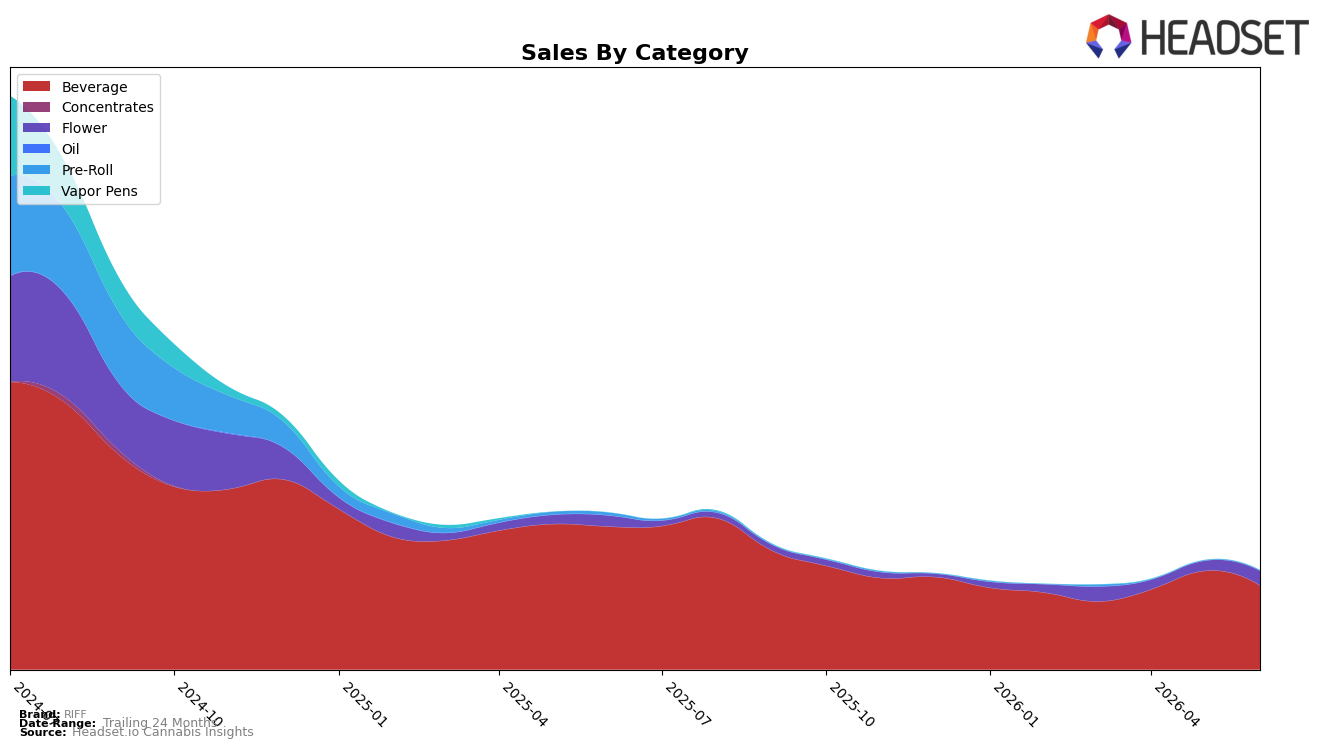

In June 2026, RIFF concentrated 85.28% of sales in Beverage, where year-over-year declined 41.31% and month-over-month fell 14.81%, while Flower rose 34.19% YoY and 46.47% MoM to 14.49% share, and Pre-Roll contracted 91.27% YoY with a modest 1.44% MoM uptick to 0.23% share. Average price increased 3.57% YoY to $7.32 as Beverage pricing sat at $6.52 and Flower at $26.17, indicating mix drag from Beverage and margin potential migrating to Flower. The pattern implies RIFF is pivoting from a shrinking Beverage base toward a higher-priced Flower segment that is expanding quickly, but the net effect still drives overall sales down 36.99% YoY due to Beverage’s outsized weight.

With Beverage share still at 85.28% and the brand ranked 18 in Beverage in Alberta, the 14.81% MoM decline there outweighs the 46.47% MoM Flower lift, and the 0.23% Pre-Roll share offers little buffering. The combination of a 41.31% YoY Beverage drop and a 34.19% YoY Flower rise suggests RIFF is overexposed to a contracting anchor category while its growth engine remains subscale, implying the brand’s positioning skews value-led in Beverage with a need to accelerate penetration where pricing power exists in Flower before the 24-month sales slide of 84.62% becomes path-dependent.

Competitive Landscape

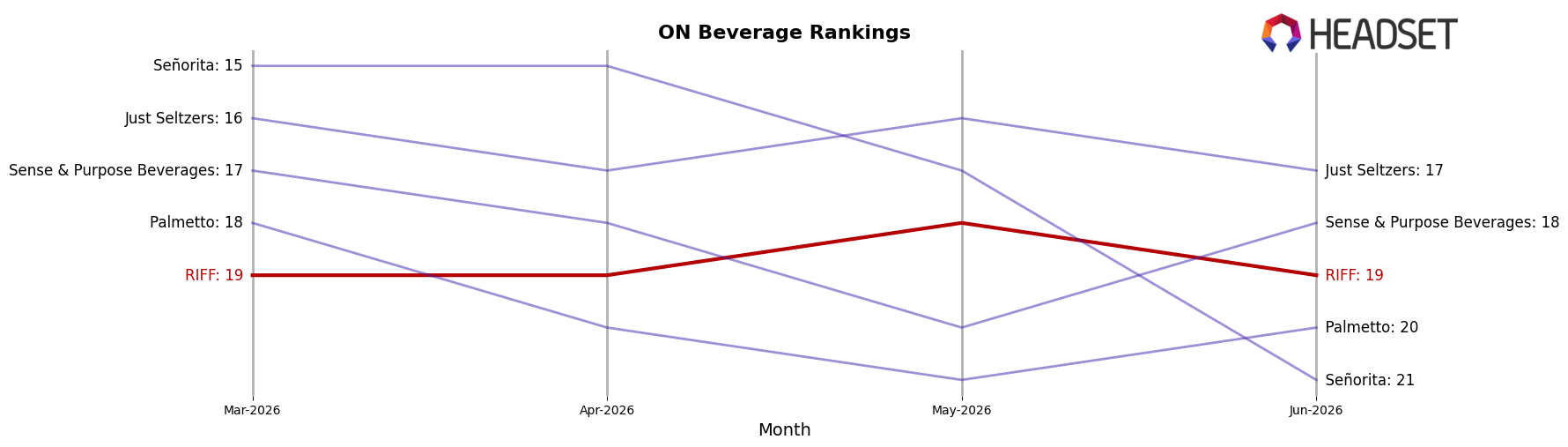

RIFF sits at rank #19 in ON Beverage for June 2026, slipping 1 position year over year from #18 while holding flat versus three months ago at #19; this contrasts with XMG holding #1 year over year at #1 despite a 36.99% sales decline and TeaPot jumping in rank from #10 to #5 on 129.54% sales growth. The gap also widened against Mollo, which improved from #4 to #3 with a 0.90% sales dip, while RIFF remains distant from its peak of #9 in July 2024 and unchanged quarter-over-quarter at #19; this pattern implies RIFF is stabilizing in the lower tier as faster-moving competitors reshuffle upward, signaling that share recovery will require a catalyst beyond category drift.

Notable Products

Boost- THC/CBG 1:1 Tropical Burst Carbonated Drink (10mg THC, 10mg CBG 355ml) posted the steepest movement in June 2026 with a -24.4% MoM drop and slid relative to Wild Raspberry Lemonade (10mg THC, 355ml) at rank 1 which fell -13.5%. Blue Raspberry Ice Lemonade (10mg THC, 355ml) held rank 2 while declining -13.8%, and Pink Certz (7g) rose 46.5% to rank 4. With four of the top five positions occupied by Beverage SKUs, the pattern implies RIFF’s mix is concentrated in drinks even as Flower is emerging as the counterweight driving incremental stability.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.