Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Nectar is stocked at 198 licensed dispensaries across Massachusetts, Oregon, and 7 other states, 116 of them in Massachusetts, with the deepest coverage in Boston, Worcester, Northampton, Brockton, and Fall River. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

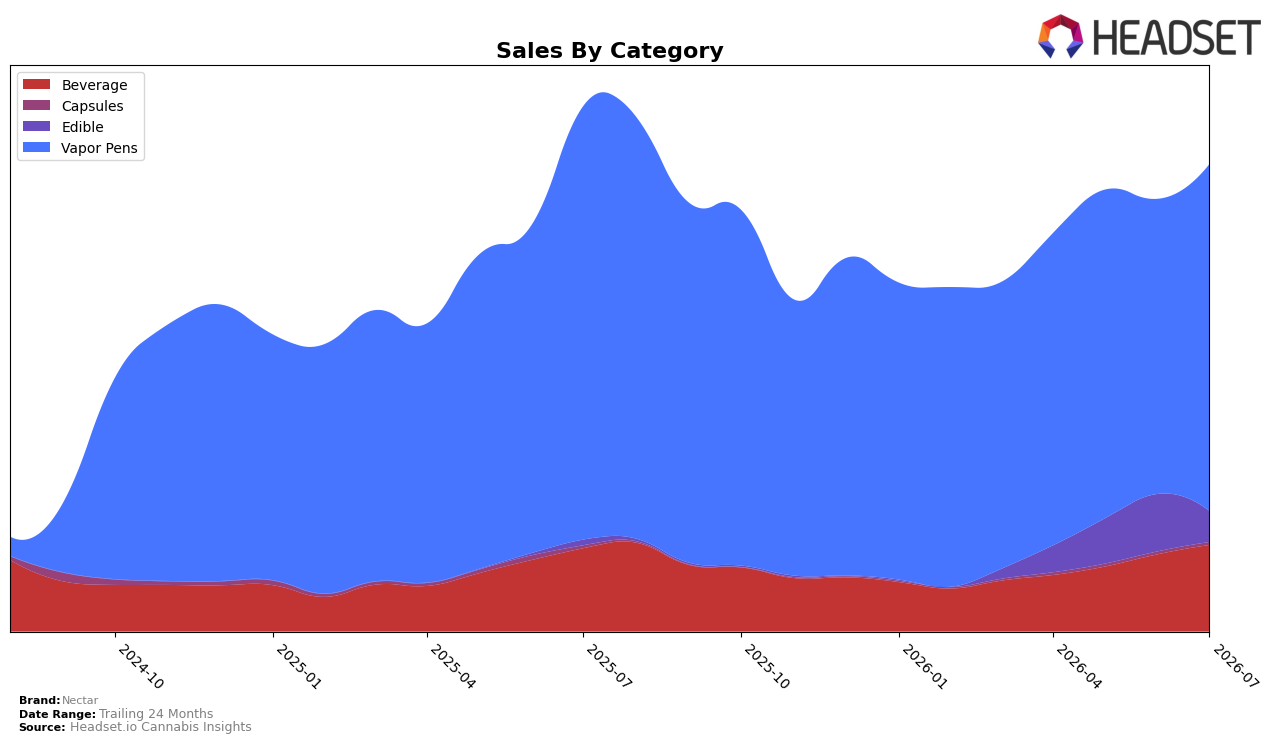

Nectar concentrated 74.38% of July 2026 sales in Vapor Pens with a 17.58% month-over-month lift but a 19.97% year-over-year decline, while Beverage held 18.50% share with 11.99% MoM growth and 3.89% YoY growth; Edible swung to 6.57% share on 487.99% YoY expansion but fell 46.29% MoM, and Capsules remained a 0.55% niche with 2.35% MoM and 0.68% YoY growth. Despite an overall brand sales change of -11.05% YoY and a 20.71% YoY drop in average price to $13.15, the mix shift toward a rebounding Vapor Pens MoM and a steadily positive Beverage YoY implies a portfolio leaning on quick-recovery inhalables while using value-priced formats to cushion annual declines.

Positioning-wise, a 29th place rank in Vapor Pens in Massachusetts alongside a 17.58% MoM rebound in that category suggests headroom if Nectar defends share while pricing down, whereas the 487.99% YoY surge but 46.29% MoM pullback in Edible signals trial-heavy, volatile demand better suited to promotional bursts than sustained volume. The combination of Beverage’s 3.89% YoY and 11.99% MoM gains with Vapor Pens’ 19.97% YoY decline indicates a barbell strategy: lean into consistent Beverage momentum to stabilize base sales while using targeted Vapor Pen activations to climb from rank 29 without overextending into Edible volatility.

Competitive Landscape

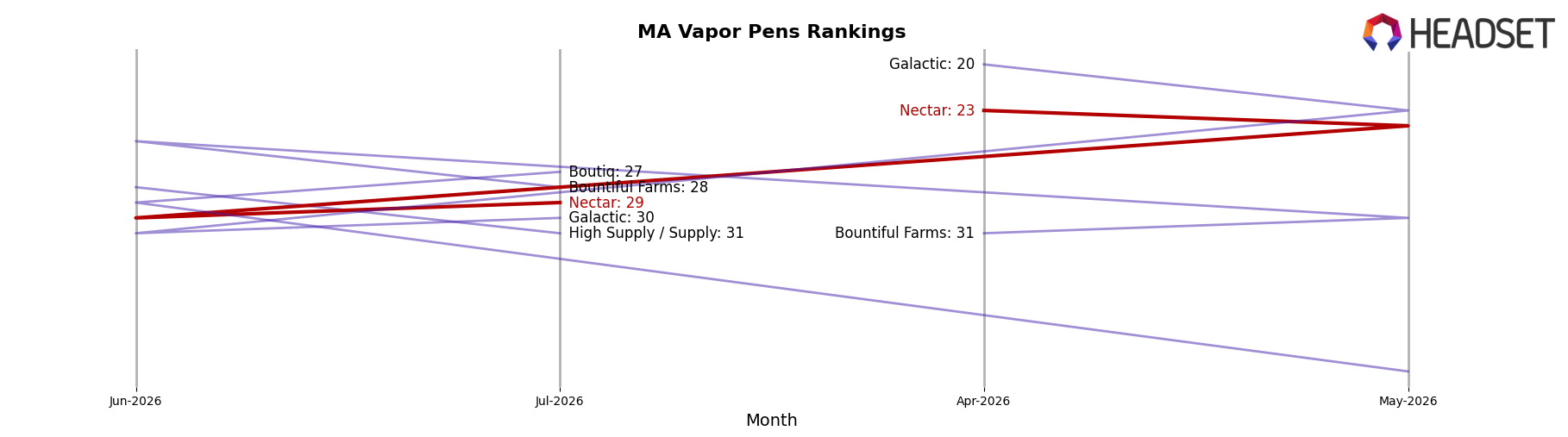

Nectar sits at rank #29 in MA Vapor Pens in July 2026, sliding 8 spots year over year from #21, and down 6 positions from April 2026’s #23, while still 9 places below its peak of #20 from August 2025; in contrast, Fernway held #1 both year over year and currently with 82.96% YoY sales growth, and Dime Industries advanced from #6 to #4 alongside 74.33% YoY growth, indicating Nectar’s relative share is being outpaced at the top of the set. With Select steady at #2 and up 10.97% YoY while Perpetual Harvest stayed #3 despite a -5.37% YoY decline, Nectar’s 8-rank YoY drop and 6-rank slide since April 2026 point to a trajectory where recovery to the historical #20 peak likely requires either mix repositioning or channel expansion to counter faster-moving leaders.

Notable Products

Cherry Lime Haze Seltzer (5mg THC, 355ml, 12oz) posted the steepest decline at -21.24% MoM and slipped to rank 3, while Mango Gummies 20-Pack (100mg) fell -27.43% MoM at rank 10; in contrast, Watermelon Gelato Seltzer (5mg THC, 355ml, 12oz) climbed +30.08% MoM into rank 2. With six of the top ten in Beverages, Sugar Free Blue Raspberry Runtz Seltzer (5mg THC, 355ml, 12oz) held rank 1 on +11.88% MoM as Strawberry Fields Seltzer (5mg THC, 355ml, 12oz) dipped -1.28% MoM at rank 6, implying the category is consolidating around a handful of winners even as laggards shed share. The Blue Milk Distillate Disposable (1g) entered at rank 4 with $48,356 alongside Skywalker OG Distillate Cartridge (1g) at rank 8, placing two Vapor Pens in the top ten while Pineapple Coconut Express Seltzer (5mg THC, 355ml, 12oz) eased -7.88% MoM at rank 9, indicating a dual-track mix where fast-rising beverages and newly scaled pens split near-term focus.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.