Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

CQ (Cannabis Quencher) is stocked at 749 licensed dispensaries across Michigan, California, and 7 other states, 270 of them in Michigan, with the deepest coverage in New Buffalo, Detroit, Grand Rapids, Kalamazoo, and Lansing. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

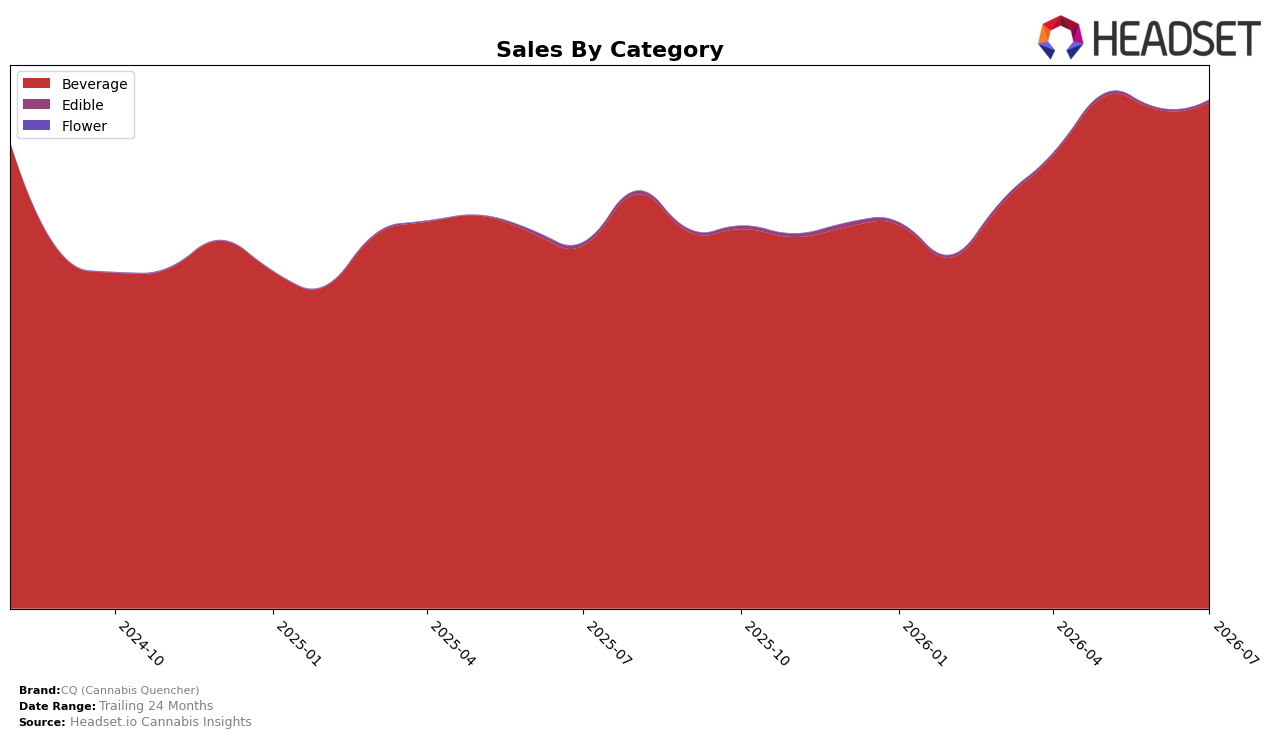

In July 2026, CQ (Cannabis Quencher) remained overwhelmingly Beverage-led with a 99.62% mix share while Edible held 0.38%, and Beverage sales grew 39.63% year over year alongside a 1.54% month over month lift; Edible moved in the opposite YoY direction at -35.08% but rebounded 28.01% month over month. Average price rose 9.95% YoY to $8.69 as Beverage pricing sat at $8.68 and Edible at $13.06, and the Beverage-led mix coincided with a Beverage rank of 4 in Illinois, implying CQ (Cannabis Quencher) is consolidating scale in its core segment rather than broadening into secondary formats.

The mix concentration and dual-speed growth imply a deliberate focus on velocity in Beverage, where a +39.63% YoY and +1.54% MoM trajectory supports price tolerance amid a 9.95% YoY price increase, while Edible’s -35.08% YoY underlines selective resource allocation despite a 28.01% MoM bounce. With Beverage at 99.62% share and a category rank of 4 in Illinois, the brand’s positioning hinges on deepening penetration and repeat in ready-to-drink use occasions rather than portfolio diversification, suggesting further uplift will come more from distribution and pack/size optimization than from expanding the Edible footprint.

Competitive Landscape

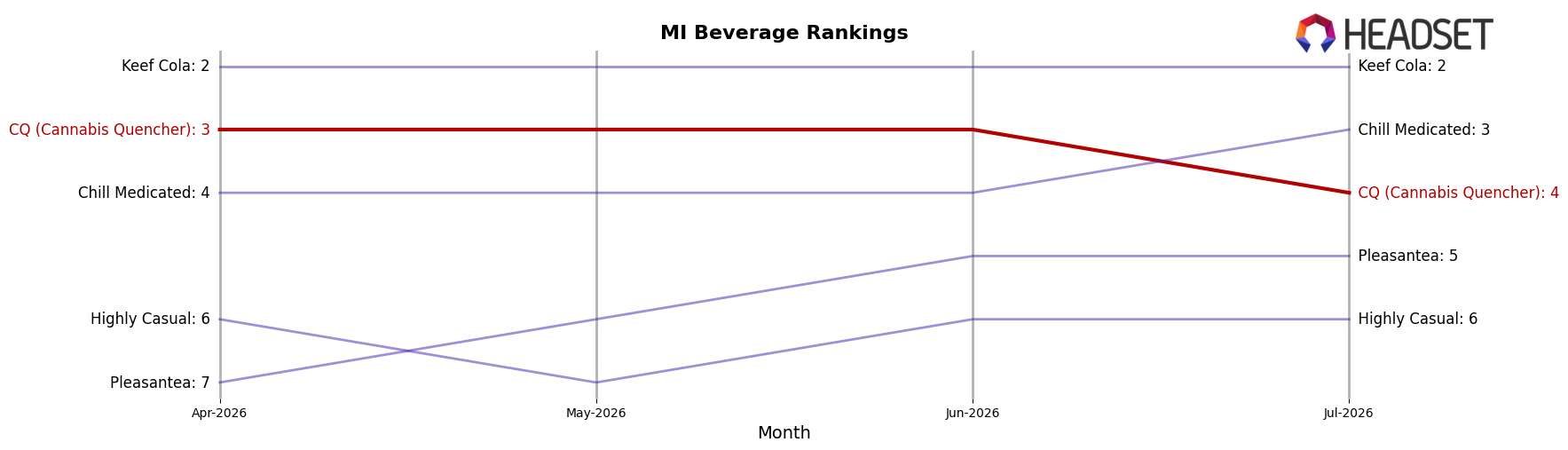

CQ (Cannabis Quencher) sits at rank #4 in MI Beverage in July 2026 after rising 4 positions year over year from #8, but it slipped 1 spot from its peak rank of #3 in June 2026 while holding within the top 5 for two consecutive months; meanwhile, Mary Jones held #1 year over year and in July 2026 as its sales grew 21.6% YoY, and Keef Cola stayed at #2 while contracting 3.6% YoY, indicating CQ is gaining relative position against a declining #2 yet losing ground to a stable #1; additionally, Chill Medicated jumped from #9 to #3 with 205.4% YoY sales growth while Pleasantea remained flat at #5 with 23.3% YoY growth, which implies CQ’s upward rank trajectory is positive but vulnerable to faster-rising challengers that can displace it from #3 without continued share capture.

Notable Products

Ginger Ale Soda (100mg THC, 355ml, 12oz) posted the largest movement in July 2026 with an 81% month-over-month gain, jumping to rank 1 while Dr. Quencher Soda (100mg THC, 12oz) slipped 10% and sat at rank 2. Old Fashioned Lemonade Live Resin Shot (100mg THC, 2oz) advanced 27% to rank 3, and Caffeinated Classic Cola Soda (100mg THC, 12oz) rose 10% at rank 4, indicating that carbonated formats are rebounding even as one flagship cola softens. Five of the top ten are Live Resin Shot SKUs, including Watermelon Lemonade up 33% at rank 5 and Strawberry Lemonade up 18% at rank 6, which concentrates growth in high-potency 2–2.2oz shots while Strawberry Infused Soda (100mg THC, 12oz, 355ml) edged down 3% at rank 10. The pattern implies CQ (Cannabis Quencher) is tilting its mix toward faster-turning shots and a single breakout soda leader, using Ginger Ale’s momentum and multiple double-digit shot gains to offset a weakening legacy cola line and stabilize the carbonated tier around a few winners.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.