Market Insights Snapshot

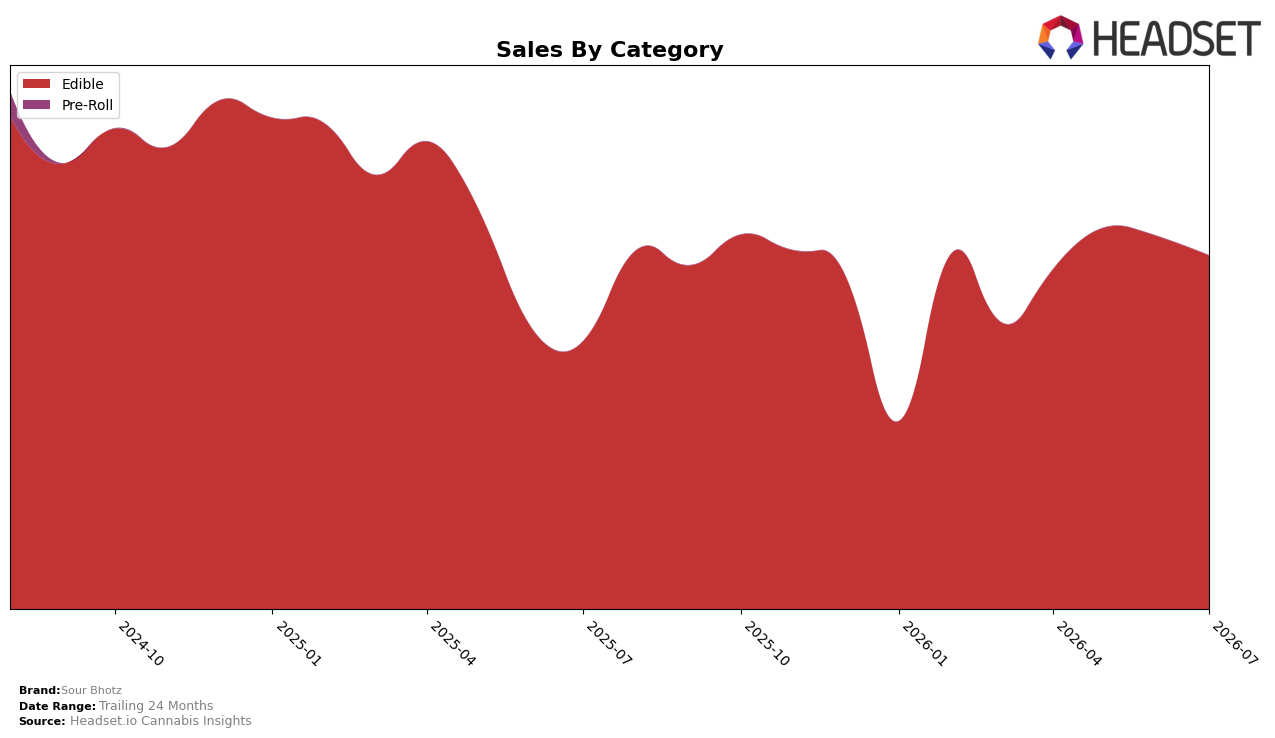

In July 2026, Sour Bhotz concentrated 100.0% of sales in Edible, with category sales up 32.1% year over year while month over month declined 5.1%, indicating a single-category reliance that lifted annual growth but softened versus June 2026. Average price fell 3.0% YoY alongside a ranking at 21 within Edible in Oregon, a combination that suggests unit velocity aided the yearly gain yet recent sequential softness limited upward rank movement. The pattern implies Sour Bhotz is capturing Edible demand on an annual basis but faces near-term pacing issues tied to price-led mix and a fully concentrated portfolio.

The consolidation in Edible—100.0% mix—paired with a 32.1% YoY sales lift and a 3.0% YoY price decrease points to a volume-led strategy that improved annual throughput but did not translate into month-to-month momentum given the 5.1% MoM decline and a state-category rank of 21. With no diversification ballast outside Edible and pricing below last year, the positioning leans toward value-driven penetration rather than premium differentiation, which in July 2026 likely traded off short-term rank gains for sustained annual share capture. This implies that, absent category expansion or a price architecture shift, maintaining July’s annual growth pace may require continued unit gains to offset MoM volatility within Edible.

Competitive Landscape

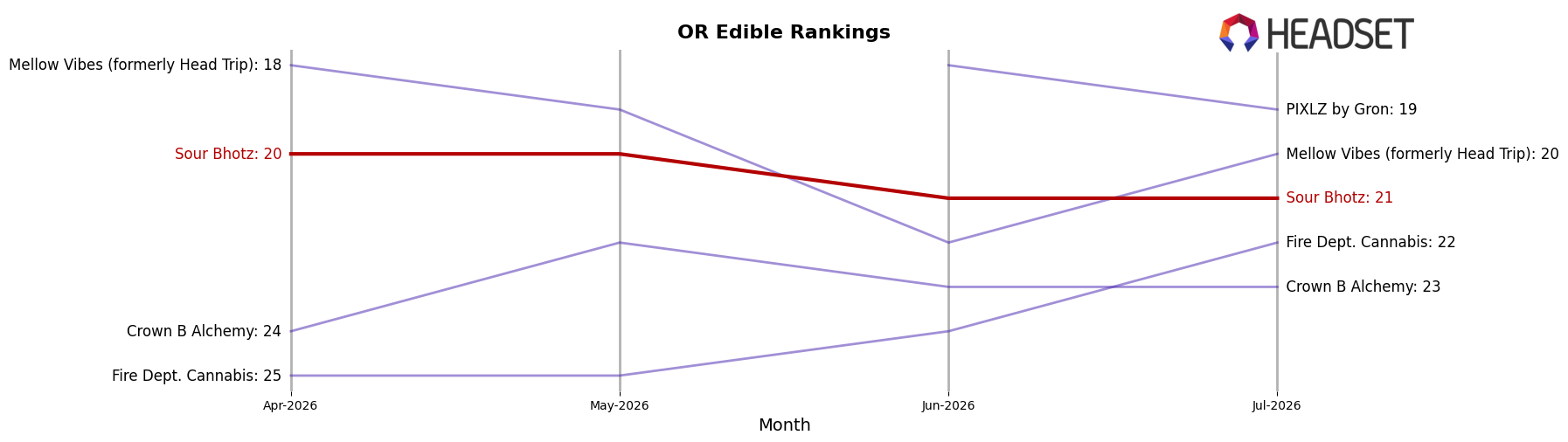

Sour Bhotz sits at rank #21 in OR Edible in July 2026, improving 2 positions year over year from #23 and slipping 1 position versus April 2026’s #20; against an earlier peak of #17 in January 2025, the brand is 4 spots lower, indicating partial recovery but not a return to best levels. In contrast, Wyld held at #1 with a 2.5% year-over-year sales increase while Gron / Grön stayed #2 with a 0.1% decline, and Drops remained #3 despite a 5.3% slide; this stability among leaders, coupled with Sour Bhotz’s 2-rank YoY climb and 1-rank quarter-on-quarter dip, implies the brand is inching upward within a relatively fixed top tier where dislodging incumbents will require share capture from positions #17–#20.

Notable Products

Pineapple Gummy (100mg) posted the standout surge at +909.6% month over month to rank 6, while Marionberry Gummy (100mg) jumped +276.0% to rank 4. At the top, Indica Cherry Cola Gummy (100mg) gained +80.5% to rank 1 even as Fruit Punch Gummy (100mg) fell -24.8% to rank 2, indicating mix shift toward novelty flavors rather than legacy leaders. Watermelon Gummy (100mg) declined -21.1% at rank 5 and Pineapple Orange Guava Gummy (100mg) contracted -85.3% at rank 10, yet eight of the top ten are Edible gummies, concentrating the lineup in a single category. The pattern implies Sour Bhotz is tilting toward flavor innovation within Edible gummies while pruning underperforming variants, consolidating share around a few fast-rising SKUs.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.