Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

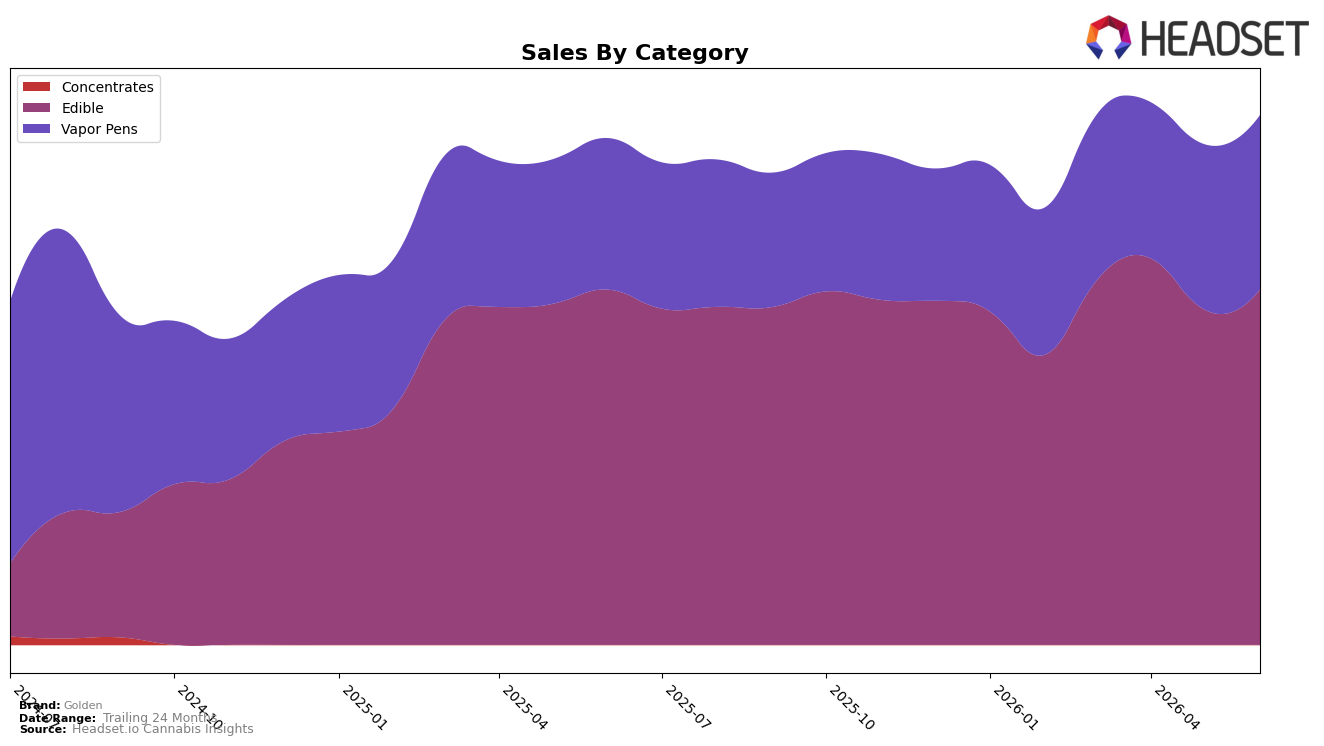

In June 2026, Golden’s category mix concentrated 67.11% of sales in Edible with Vapor Pens at 32.89%, while Edible grew 6.04% month over month and 5.14% year over year versus Vapor Pens at 5.42% MoM and 15.09% YoY. Average price rose 7.24% YoY to $10.17, with Edible priced at $8.92 and Vapor Pens at $14.26, indicating the higher-priced segment expanded share-adjacent demand without overtaking Edible’s 67.11% lead. The pattern implies a dual-track strategy where Edible stability at rank 15 in Oregon anchors volume while faster YoY growth in Vapor Pens strengthens premium yield potential.

Because Vapor Pens advanced 15.09% YoY against Edible’s 5.14% YoY while both climbed over 5% MoM, Golden can lean into margin by nudging mix toward the 32.89% Vapor Pens base without eroding the Edible core at 67.11%. With brand sales up 4.54% YoY and a 7.24% YoY price lift, the gap between demand growth and price suggests room to convert MoM momentum (6.04% in Edible vs 5.42% in Vapor Pens) into sustained share if Vapor Pens activation targets higher-ticket buyers and Edible protects rank 15 in Oregon; the implication is that pricing power resides in Vapor Pens while Edible sets the floor for throughput.

Competitive Landscape

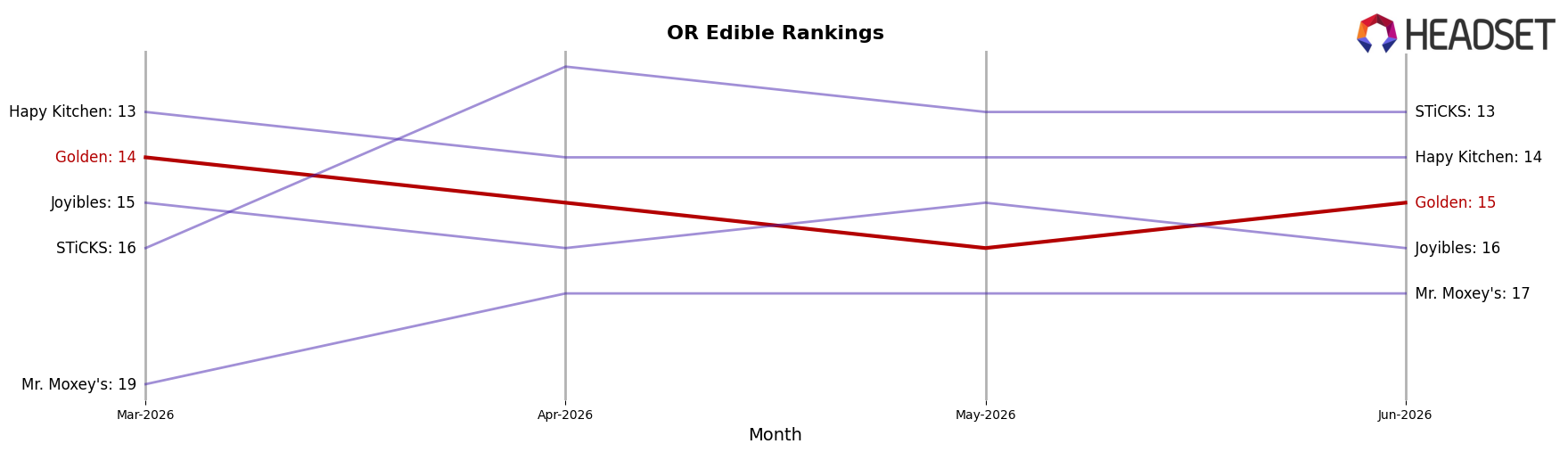

Golden sits at rank #15 in OR Edible for June 2026, unchanged YoY from #15, and slipped 1 position from March 2026 when it peaked at #14; that flat YoY rank paired with a 1-rank decline versus March indicates share stability without upward momentum. In contrast, Wyld held #1 YoY and in June 2026 while expanding sales by 45.3% YoY, and Gron / Grön stayed at #2 as sales contracted by 104.6% YoY, showing that category gains are concentrating at the very top even as the runner-up retrenches. Meanwhile, Drops remained at #3 with a 4.4% YoY sales decline, and Good Tide remained #4 with an 88.9% YoY increase, a divergence that makes lateral movement from #15 harder without a step-change in velocity. Taken together, a zero-position YoY change at #15 and a 1-rank dip since March 2026 imply a stall in rank trajectory amid polarization where leaders widen gaps and mid-pack churn limits ascension.

Notable Products

CBD/THC 2:1 Kiwi Strawberry Fruit Chews 10-Pack (100mg CBD, 50mg THC) posted the largest move in June 2026 with +58.9% MoM into rank 9, while Hybrid Apple Solutely The Best Fruit Chew Blast (100mg) fell -12.1% to rank 2. The top spot went to CBD/CBN/CBG/THC 3:3:3:1 Brown Butter Apricot Fruit Chews 10-Pack (300mg CBD, 300mg CBN, 300mg CBG , 100mg THC) with +27.9% MoM at rank 1 and approximately $19,747, as CBN/THC 3:1 Chamomile Peach Fruit Chews 10-Pack (300mg CBN, 100mg THC) slid -12.4% to rank 3. Seven of the top ten are Edible SKUs, and Vapor Pens held ranks 4 and 6 with small MoM moves of -1.4% and +8.2%, respectively. The pattern implies Golden’s mix is tilting toward functional multi-cannabinoid edibles, using CBD-forward gains to offset single-flavor softness and reducing reliance on Vapor Pens for headline growth.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.