Market Insights Snapshot

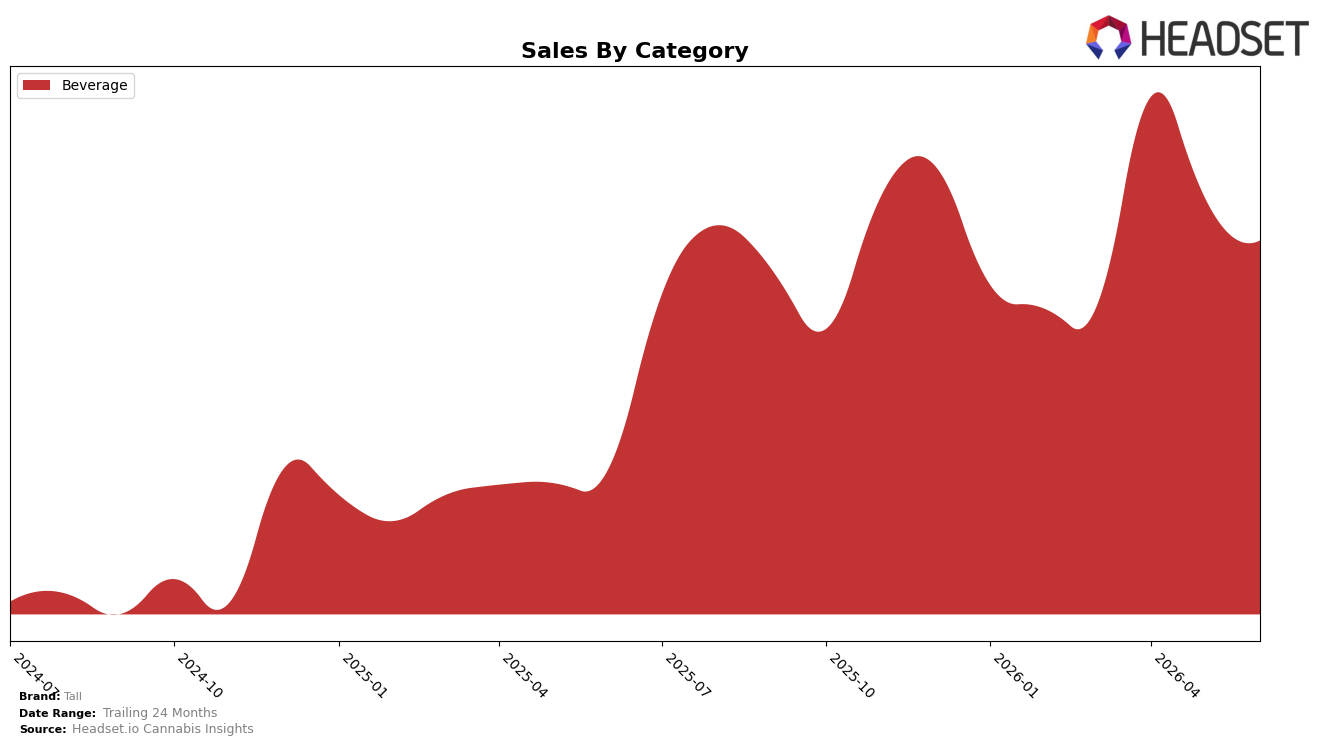

Tall concentrated 100.0% of June 2026 sales in Beverage, with year-over-year growth of 96.8% alongside a month-over-month decline of 8.5%, while the average price fell 12.8% YoY to $4.33. In Maryland Beverage, Tall held rank 5 in June 2026, indicating scale gains YoY despite a short-term pullback MoM; the pattern implies Tall is trading volume for price in a single-category footprint, tightening its price-to-volume engine within Beverage rather than diversifying.

The 96.8% YoY lift paired with an 8.5% MoM dip and rank 5 positioning signals a price-led share strategy where lower unit prices (-12.8% YoY) are fueling annual volume but exposing monthly volatility. With 100.0% category concentration and a top-five rank, the implication is that Tall’s near-term growth will hinge on stabilizing Beverage velocity at the current price tier; absent diversification, sustaining rank 5 or improving it will depend on converting the discounted price posture into repeat purchase rather than further price cuts.

Competitive Landscape

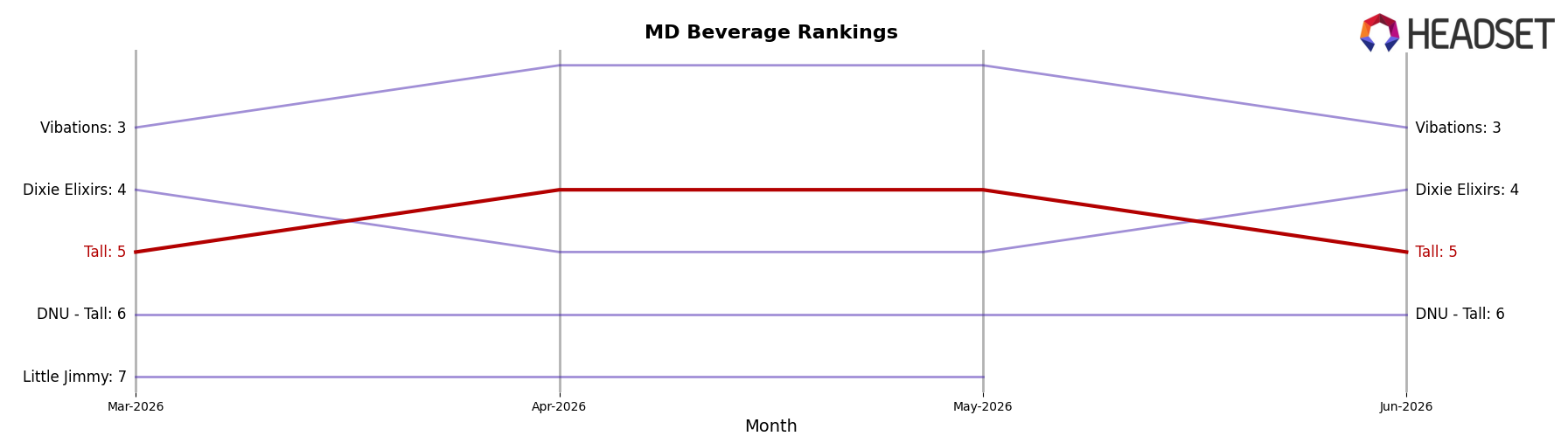

Tall sits at #5 in MD Beverage for June 2026, unchanged from #5 year over year, and it also held #5 three months ago while peaking at #4 in May 2026; in contrast, Keef Cola held #1 both this year and last year as its sales grew 16.35% YoY, while Vibations climbed from #4 to #3 on 116.95% YoY sales growth. Dixie Elixirs slipped from #3 to #4 with just 2.07% YoY growth, and Sunnies by SunMed is steady at #2 year over year with 44.74% YoY growth; the combination of Tall’s flat rank at #5 and nearby competitors moving up or down implies a stable share position that risks entrenchment unless Tall converts its May 2026 #4 peak into sustained rank gains.

Notable Products

Elevated- Yuzu Blood Orange Seltzer (5mg THC, 12oz) posted the largest month-over-month surge at +295.9% to rank 7 in June 2026, while Dark Berry Seltzer (5mg THC, 12oz) fell -35.8% to rank 5. Top slots tightened as Hibiscus Cherry Lime Seltzer (10mg THC, 12oz) slipped -7.5% at rank 1 and CBD/THC 1:1 Fuji Apple Pear Seltzer (10mg CBD, 10mg THC, 12oz) dropped -11.7% at rank 2, indicating share is rotating from legacy 10mg cores to newer 5mg Elevated variants. With eight of the top ten in the Beverage category and a single SKU jump of nearly +300%, the mix points to a pivot where lower-dose innovation can offset declines in several 10mg staples, implying near-term emphasis on flavor extensions and 5mg formats over volume pushes in mature 10mg lines.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.