Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Dixie Elixirs is stocked at 337 licensed dispensaries across Michigan, Maryland, and 5 other states, 165 of them in Michigan, with the deepest coverage in New Buffalo, Monroe, Detroit, Grand Rapids, and Kalamazoo. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

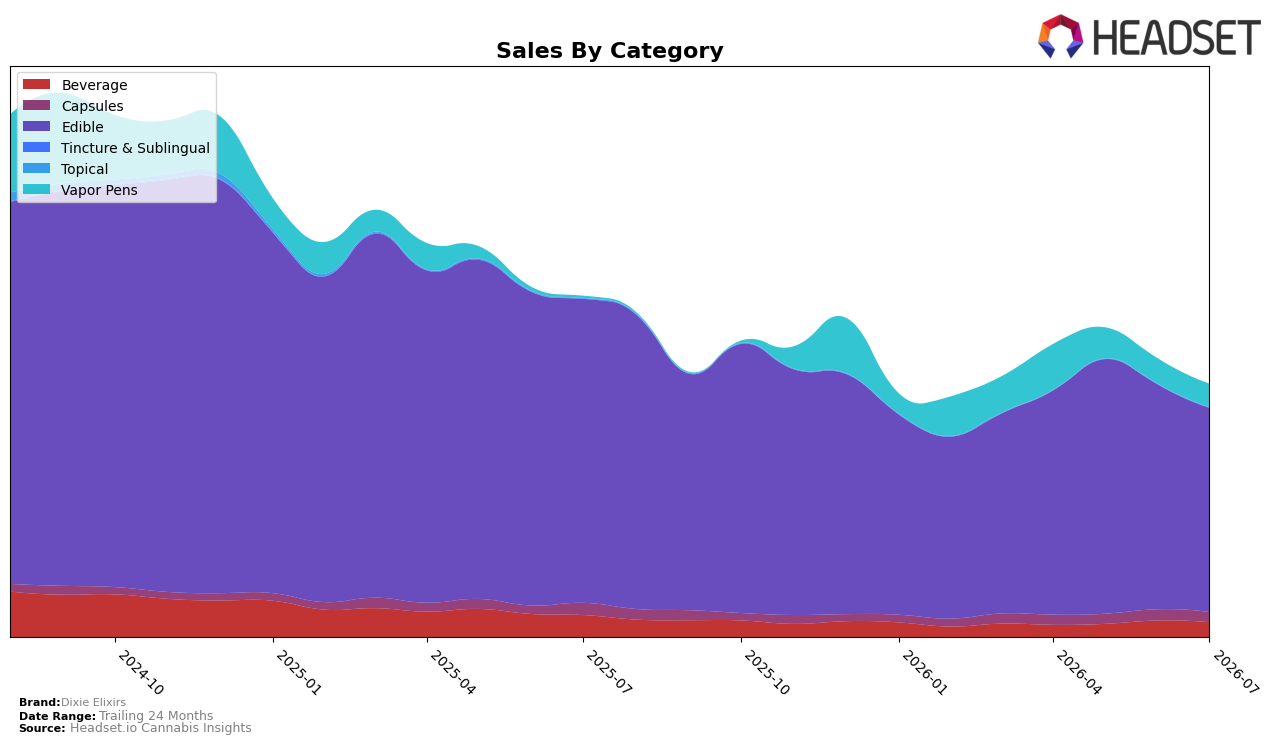

Dixie Elixirs concentrated 81.17% of July 2026 sales in Edible, where year-over-year declined 32.87% and month-over-month fell 9.14%, while Beverage held 5.76% with a 33.14% YoY drop and a 10.80% MoM decline; Capsules accounted for 3.90% with a 17.03% YoY contraction and 9.39% MoM slide. Vapor Pens rose to 9.17% share on a 1,195.05% YoY surge despite a 7.81% MoM dip, and average price across the brand eased 3.34% YoY; in Maryland Edible, the brand sat at rank 14. The pattern indicates over-reliance on a shrinking Edible base with nascent diversification into Vapor Pens that is growing from a small base but not yet offsetting sequential softness, implying immediate volume risk if Edible continues to contract.

With Edible share at 81.17% and down 32.87% YoY alongside Beverage down 33.14% YoY, the brand’s core ingestibles are compressing faster than the brand-level sales decline of 25.94%, while Capsules’ 17.03% YoY drop provides limited cushion; meanwhile, Vapor Pens’ 1,195.05% YoY expansion to 9.17% share signals a pivot that is partially masked by a 7.81% MoM step back. Holding rank 14 in Maryland Edible and a 9.14% MoM decline in its largest category suggests the brand’s pricing (-3.34% YoY) and assortment are not yet arresting share loss within core, so near-term positioning depends on accelerating Vapor Pens without further eroding Edible, effectively rebalancing mix away from categories posting double-digit MoM declines.

Competitive Landscape

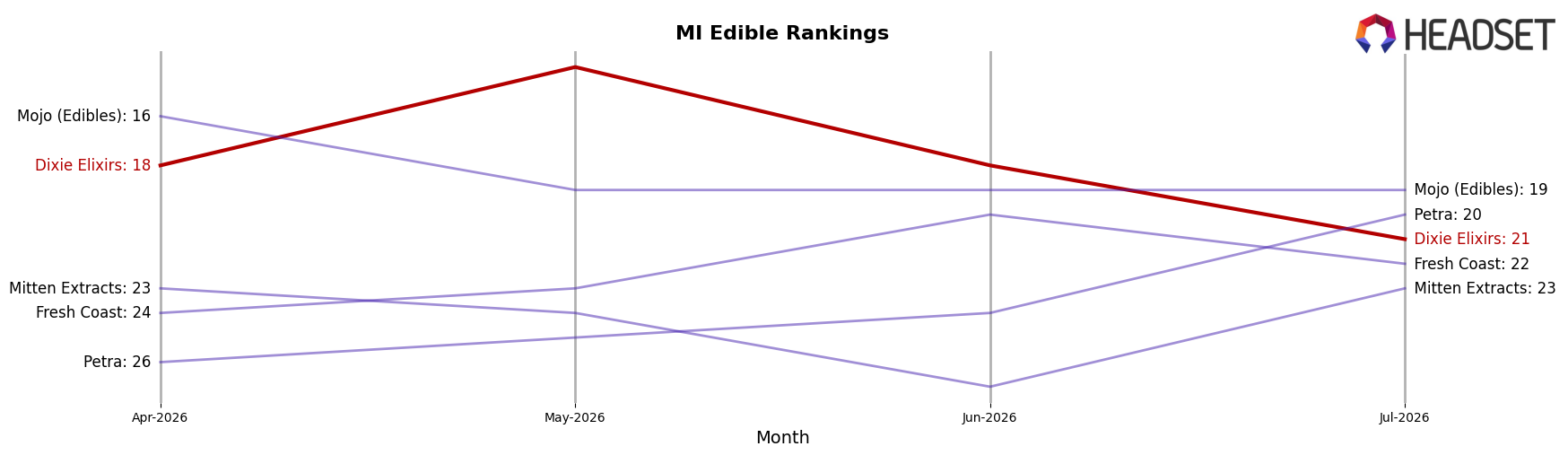

Dixie Elixirs is ranked #21 in MI Edible in July 2026, down 6 positions year over year from #15, and 3 positions lower than April 2026’s #18, while still trailing its October 2024 peak of #11; in contrast, Wyld held #1 year over year with a -23.3% sales change and MKX Oil Company slipped from #3 to #4 despite a 4.6% sales increase, indicating rank is being reshuffled more by relative momentum than absolute growth. With Choice steady at #2 on a -0.4% sales change and Good Tide fixed at #5 amid a -25.3% decline, Dixie Elixirs’ 6-rank YoY slide alongside only a 3-rank drop since April 2026 implies recent stabilization at a lower tier that will require share capture from flat or declining leaders to reverse.

Notable Products

CBG/CBD/THC 2:1:1 Synergy Berry Focused Gummies 10-Pack (100mg CBG, 50mg CBD, 50mg THC) posted the steepest decline at -41.7% while holding rank 7, and the CBN/CBD/THC 2:1:1 Synergy Sleepberry Gummies 10-Pack (100mg CBN, 50mg CBD, 50mg THC) fell -34.1% yet remained rank 1. In contrast, THC/CBN/CBD 2:1:1 Synergy Cherry Chill Gummies 10-Pack (200mg THC, 100mg CBN, 100mg CBD) rose +31.4% to rank 2, while Sour Smash Gummies 10-Pack (200mg) slipped -10.2% at rank 4. With eight of the top ten as Edible gummies and rank positions clustering at 1–5 and 7–10, the pattern implies reliance on a gummy-heavy lineup where sleep and focus variants are volatile month to month, signaling a need to rebalance toward steadier core flavors rather than specialty ratios.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.