Where to Buy

Tasty's (OR) is stocked at 147 licensed dispensaries across Oregon, with the deepest coverage in Portland, Salem, Bend, Eugene, and Medford. Search by ZIP code or city below to find the closest one.

Market Insights Snapshot

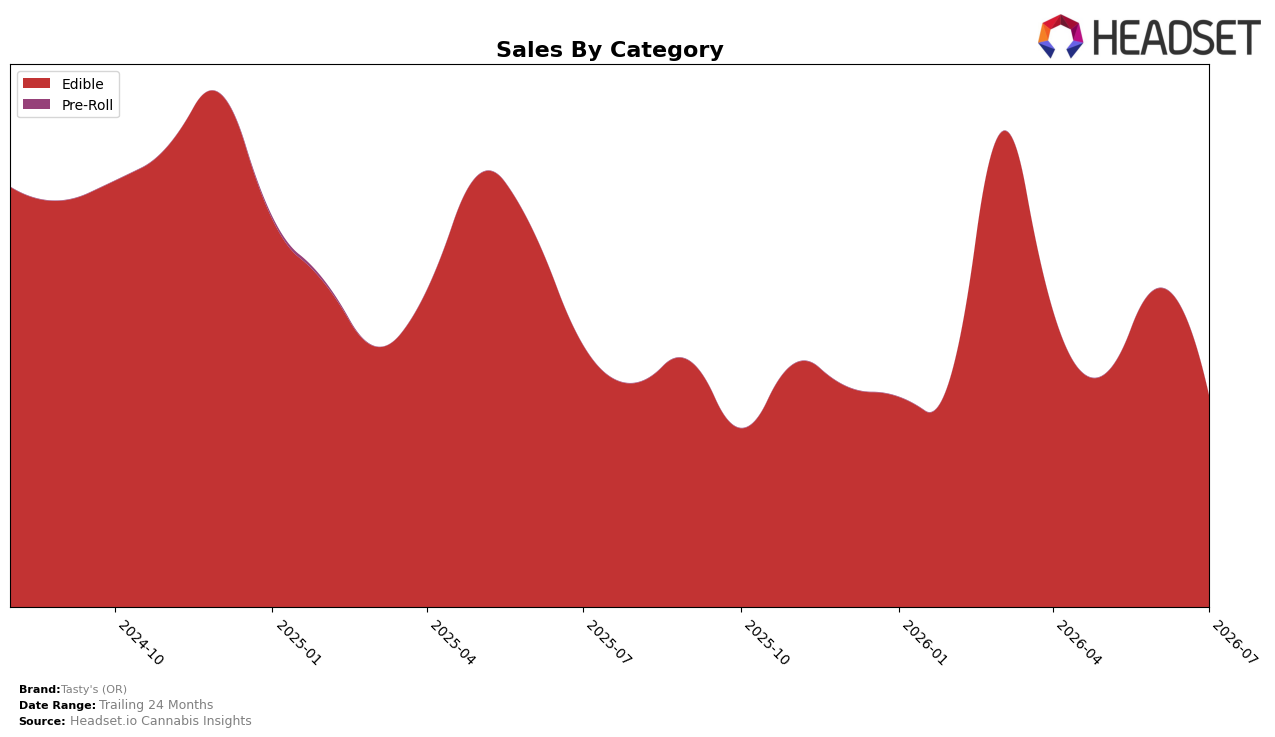

Tasty's (OR) operated as a single-category brand in July 2026, with Edible accounting for 100.0% of sales and placing the brand at rank 29 in Oregon Edible. Within that focus, year-over-year sales declined 19.3% and month-over-month sales fell 33.6%, while the average price dropped 10.0% year over year to $7.13 and implicitly slid further month over month alongside the volume pullback. The pattern points to a category-concentrated model where exposure to Edible magnifies volatility: rank 29 paired with a 33.6% monthly contraction suggests shelf velocity and promo depth are not offsetting the price drop, implying a need to recalibrate pack sizes or price tiers to stabilize share.

Given 100.0% reliance on Edible and a -19.3% year-over-year trajectory against a deeper -33.6% month-over-month dip, the brand’s positioning skews toward reactive pricing rather than demand-led pull, as indicated by a 10.0% year-over-year price decrease that did not prevent the rank from settling at 29. The concentration risk is clear: holding solely Edible share in Oregon means small shifts in promo calendars or retailer resets can translate into double-digit monthly swings, so positioning should pivot toward a differentiated Edible sub-segment or format where a lower price can translate to rank gains instead of coinciding with contraction.

Competitive Landscape

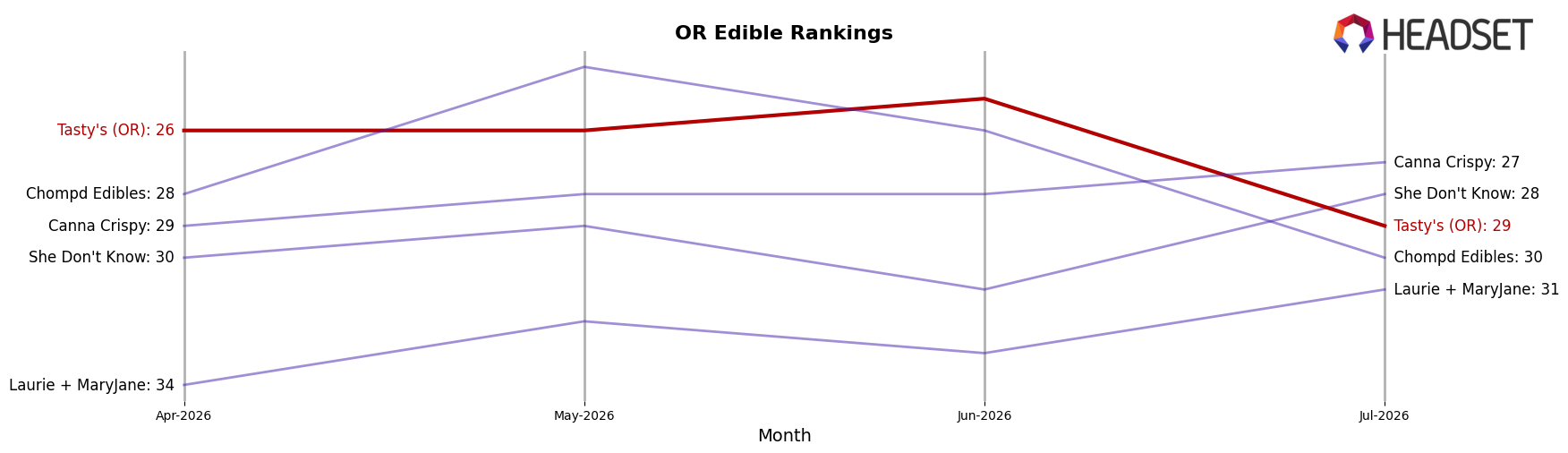

Tasty's (OR) sits at rank #29 in Oregon Edible for July 2026, sliding 2 positions year over year from #27 and down 3 ranks from April 2026’s #26, while still 8 spots below its peak #21 in March 2026; in contrast, Wyld held #1 both this year and last as its sales grew 2.5% YoY, and Mule Extracts stayed at #5 with a 7.5% YoY sales lift, indicating competitors are either stable or inching upward as Tasty’s (OR) drifts lower. The 2-rank YoY slippage alongside a 3-month decline from #26 to #29, versus flat ranks at #1 and #5 for named rivals and a −0.1% to −9.8% YoY sales range among top-5 incumbents, implies Tasty’s (OR) is losing relative share in a mostly static leaderboard where small growth at the top is enough to widen the gap.

Notable Products

Sour Peach Greenlit High Dose Gummy 10-Pack (100mg) delivered the standout movement in July 2026, vaulting to rank 1 with +185.4% MoM while Grape Gummy (100mg) slipped 8.4% at rank 2, and this divergence implies demand is skewing toward higher-dose differentiation over legacy core flavors. Sativa Pineapple Gummy (100mg) plunged 73.8% MoM at rank 3 as Lemon Drop Hard Candy 10-Pack (100mg) fell 26.0% at rank 9, and with all top-10 items in the Edible category and multiple hard-candy SKUs clustered in ranks 4, 5, and 9, the portfolio shows volatility concentrated in flavor-based line extensions rather than format shifts. Black Cherry Live Resin Hard Candies 10-Pack (100mg) rose 43.4% into rank 5 while the CBD/THC 1:1 Tangerine Dream Hard Candies 10-Pack (100mg CBD, 100mg THC) held near-flat at rank 4, and the spread between +185.4% and -73.8% MoM suggests consumers are bifurcating toward both potency-led gummies and away from certain single-flavor SKUs, pointing to sharper SKU-level selection pressure. The mix signals Tasty's (OR) is tilting commercial effort toward high-dose hero products while pruning or reformulating underperforming flavor variants to stabilize rank spread and protect the edible shelf footprint.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.