Where to Buy

Canna Crispy is stocked at 65 licensed dispensaries across Oregon, with the deepest coverage in Portland, Salem, Eugene, Gresham, and Hillsboro. Search by ZIP code or city below to find the closest one.

Market Insights Snapshot

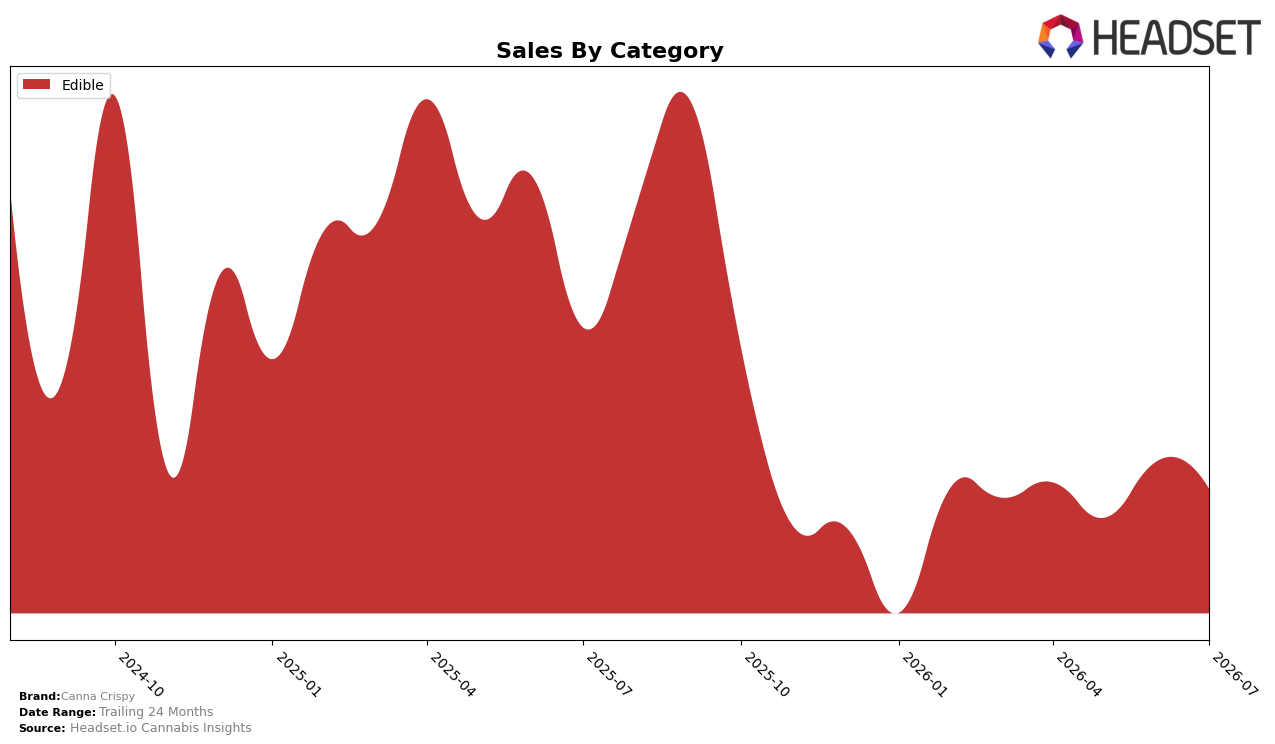

In July 2026, Canna Crispy’s mix sat entirely in Edible at 100.0% share, with Edible sales down 18.9% year over year and down 3.9% month over month, while average price declined 7.7% YoY. The brand ranked 27 in Edible within Oregon, and its brand-level sales trended -18.9% YoY against a 24‑month change of -4.1%, indicating a sharper recent contraction than its two‑year trajectory; the implication is concentration risk in a single category amplifying cyclical downside.

That 100.0% dependence on Edible, paired with a 7.7% YoY price reduction and a 3.9% MoM sales dip in July 2026, points to a price-led defense that has not offset volume softness; at rank 27 in Oregon Edible, mid-pack positioning limits visibility gains from discounting. The gap between the -18.9% YoY decline and the -4.1% 24‑month trend implies the brand’s current positioning is skewing toward share erosion rather than stabilization, suggesting diversification or subsegment focus within Edible would be required to reverse a downtrend that pricing alone is not addressing.

Competitive Landscape

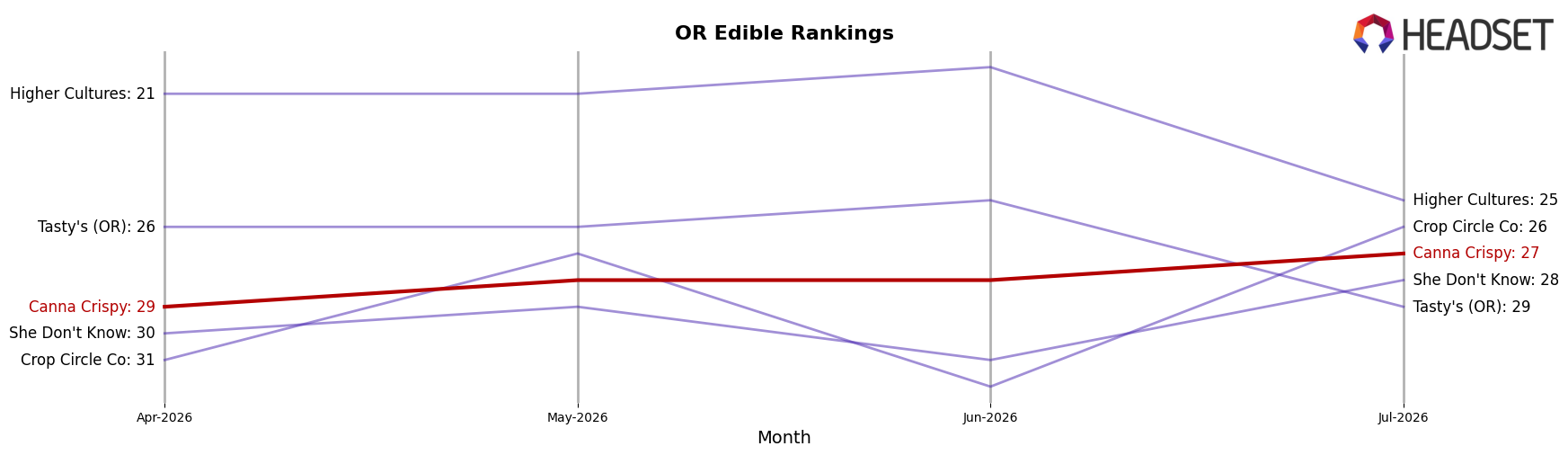

Canna Crispy sits at rank #27 in OR Edible in July 2026, down 2 spots year over year from #25, while improving 2 positions versus April 2026 when it was #29; the brand’s peak of #23 in September 2025 marks a 4-rank slide from its high, and the flat top tier suggests limited room for organic lift. By contrast, Wyld held #1 year over year with a 2.5% sales increase, while Drops stayed at #3 despite a 5.3% sales decline, indicating that stability at the top coexists with churn in mid-tier positions where Canna Crispy competes. The pattern implies that Canna Crispy’s slight YoY rank decline and quarter-on-quarter uptick point to a brand oscillating around the mid-20s, requiring disruptive moves to break past a relatively static top-5 and reverse the 4-rank gap from its September 2025 peak.

Notable Products

Indica Fruity Crispy Treat (100mg) delivered the standout move in July 2026 with a 231.3% month-over-month surge to rank 2, while Hybrid Original Crispy Treat (100mg) fell 22.8% to rank 6. Sativa Fruity Crispy Treat (100mg) grew 21.5% to hold rank 1, and Sativa Strawberry Crispy Treats (100mg) slipped 15.5% to rank 5. Eight of the top ten are Edible SKUs within the Crispy Treat family, indicating a concentrated portfolio where flavor-led Indica and Sativa variants are absorbing demand from weakening Hybrid placements. The pattern implies Canna Crispy is pivoting toward faster-velocity flavor/strain combinations, suggesting resource allocation should favor Indica and Sativa extensions over Hybrid refreshes.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.