Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Temple is stocked at 37 licensed dispensaries across Maryland and Michigan, 24 of them in Maryland, with the deepest coverage in Baltimore, Columbia, Pikesville, Upper Marlboro, and Camp Springs. Search by ZIP code or city below to find the closest one.

Market Insights Snapshot

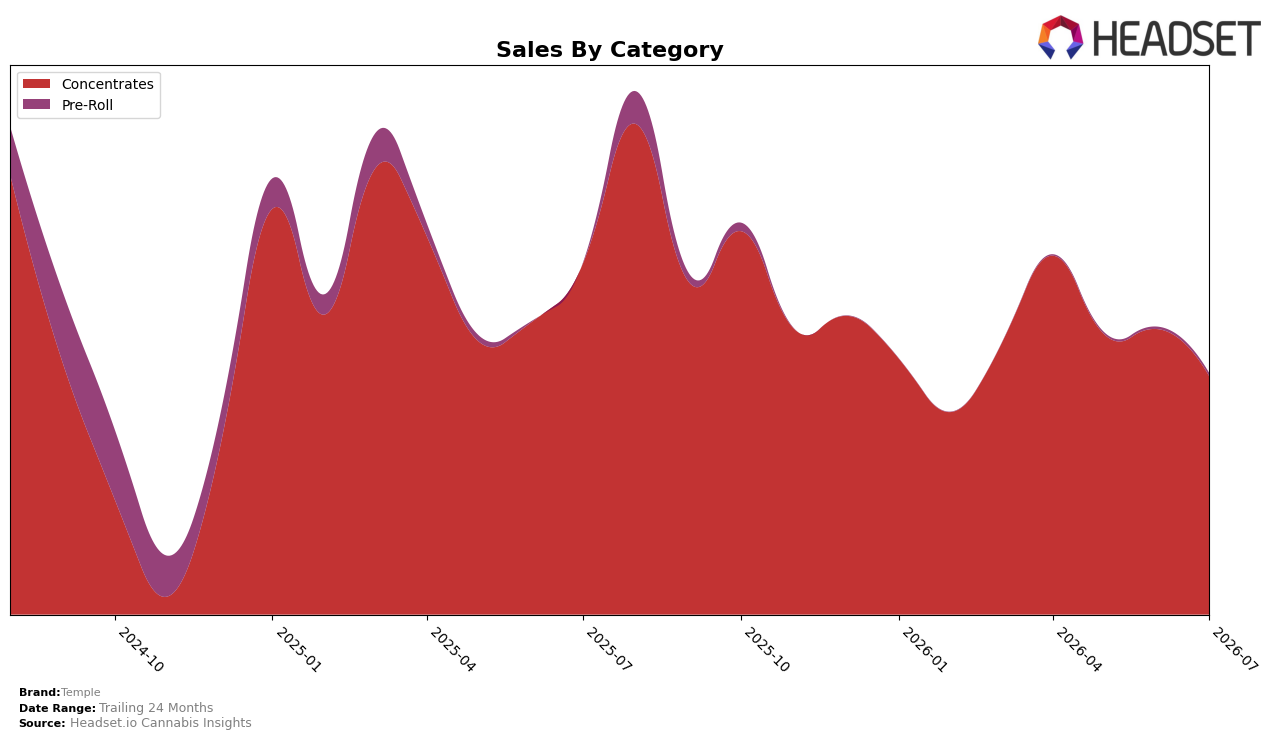

Temple’s category mix in July 2026 was concentrated, with Concentrates holding 98.85% share while Pre-Roll accounted for 1.15% share; Concentrates declined 32.09% year over year and 16.44% month over month, while Pre-Roll grew 653.18% year over year and 37.31% month over month. Despite a 7.55% year-over-year drop in average price to $44.70, the brand’s overall sales fell 31.37% year over year and 61.80% over 24 months, and the top market was Maryland with a Concentrates rank of 23. The pattern implies overexposure to a single category where price cuts have not offset volume softness, while small but rapid Pre-Roll growth offers a diversification lever that is currently too small to counterbalance core-category contraction.

With Concentrates at 98.85% share but down 16.44% month over month and 32.09% year over year, and Pre-Roll up 37.31% month over month and 653.18% year over year at only 1.15% share, the brand’s risk profile skews toward Concentrates cyclicality rather than mix-driven stability. Holding rank 23 in Concentrates in Maryland while the average price fell 7.55% indicates price-led tactics without commensurate share capture, implying that maintaining or improving category rank will require either deeper penetration within Concentrates or accelerating mix-shift into faster-growing Pre-Roll to reduce volatility.

Competitive Landscape

Temple sits at rank #24 in MD Concentrates in July 2026, down 5 positions year over year from #19, and 4 spots lower than April 2026 when it was #20; the gap from its peak rank of #17 in August 2025 to #24 now marks a 7-position slide that coincides with category leaders consolidating share. Meanwhile, District Cannabis held #1 year over year at #1 with 58.1% YoY sales growth, and Grassroots moved upward from #4 to #2 with 48.5% YoY growth, indicating that Temple’s relative decline is less about short-term volatility and more about being outpaced by faster-advancing peers; this trajectory implies Temple must arrest a multi-quarter rank erosion or risk further displacement from the top 20.

Notable Products

Bravado Nepalese Hash Ball (1g) posted a 668.9% month-over-month surge to rank 1, while White 99 Temple Ball Hash (1g) plunged 56.2% to rank 2, flipping the leadership order in July 2026. Gush Mintz Temple Ball Hash (1g) climbed 70.5% to rank 3 as Super Skunk Temple Ball Hash (1g) fell 75.8% to rank 6, concentrating gains in Nepalese and Gush lines while eroding older Temple Ball variants. With seven of the top eight SKUs in Concentrates and four of the top five being Nepalese or Temple Ball Hash formats, the mix implies Temple is consolidating around hash-led concentrates and deprioritizing slower Temple Ball strains despite one Pre-Roll entrant growing 37.3% at rank 8.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.