Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Roll One / R.O. is stocked at 287 licensed dispensaries across Maryland, Ohio, and 5 other states, 94 of them in Maryland, with the deepest coverage in Baltimore, Silver Spring, Annapolis, Bethesda, and Columbia. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

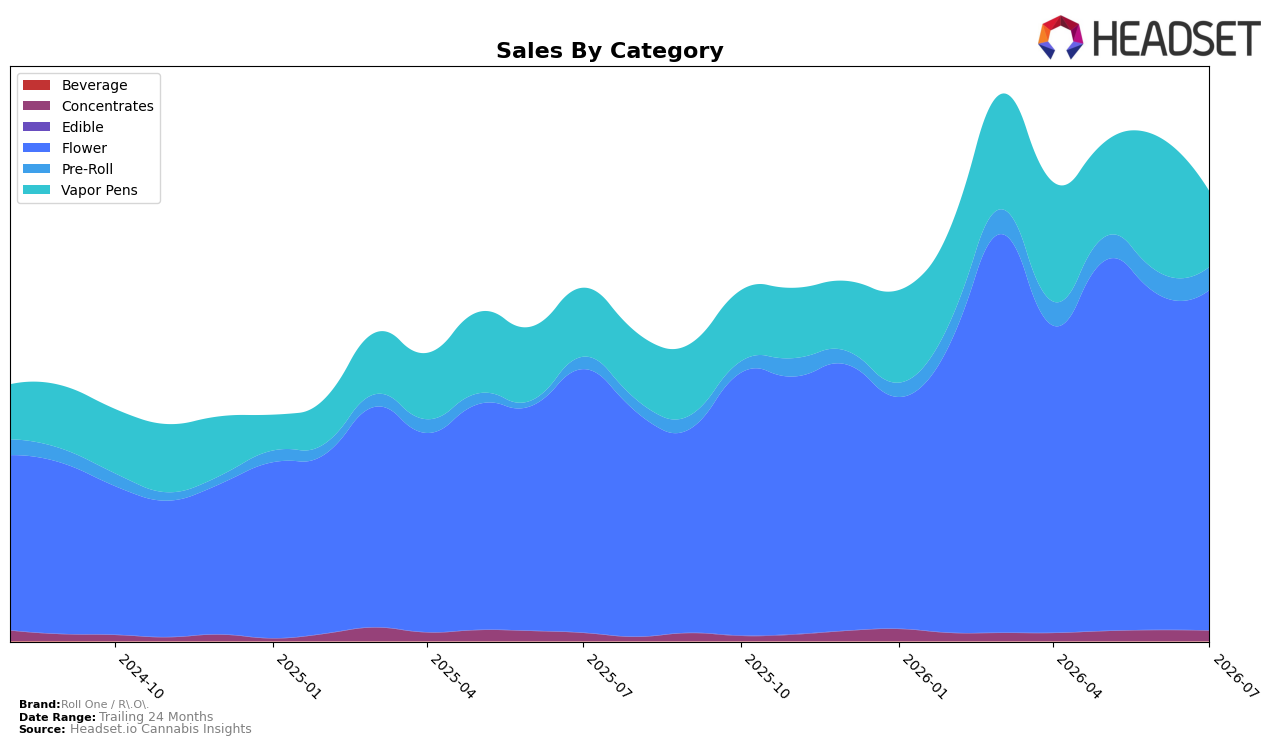

In July 2026, Roll One / R.O.’s mix skewed heavily toward Flower at 75.86% share, with Flower up 29.18% year over year and 1.42% month over month, while Vapor Pens held 16.78% share but fell 44.27% month over month despite a 9.49% year-over-year gain. Pre-Roll’s 5.11% share rode a 90.56% year-over-year increase and a 2.94% month-over-month rise, and Concentrates at 2.25% share grew 29.31% year over year but slipped 4.85% month over month. With the overall brand up 27.44% year over year and average price up 5.45% to $26.66, the pattern points to a consolidation around Flower volume while Pre-Roll becomes the growth outlier and Vapor Pens retracts near term, indicating the brand is leaning into combustion formats as the dependable throughput driver.

The combination of a 75.86% Flower share and a 12th-place Flower rank in Maryland positions Roll One / R.O. as a volume-weighted player competing on breadth within a single anchor category, while the 44.27% month-over-month contraction in Vapor Pens suggests reduced cross-category insulation against format volatility. The 90.56% year-over-year lift in Pre-Roll alongside only a 2.94% month-over-month uptick implies that trial-led gains are transitioning into steadier but smaller monthly increments, whereas Concentrates’ 4.85% month-over-month dip against a 29.31% year-over-year rise signals episodic demand rather than a structural pillar. Taken together, the mix suggests the brand’s near-term positioning hinges on sustaining Flower’s incremental gains while using Pre-Roll as the marginal share lever to offset pen softness, rather than pursuing a balanced portfolio across inhalable formats.

Competitive Landscape

Roll One / R.O. sits at rank #12 in July 2026 in MD Flower, down 3 positions from its July 2025 rank of #9, while its prior three-month position of #16 marks a 4-place climb into the current month; the brand’s peak of #9 in July 2025 contrasts with today’s #12, indicating a net YoY decline of 33% in rank position alongside a quarter-over-quarter improvement of 25% in rank. In the same period, SunMed held steady at #1 year over year and RYTHM advanced from #3 to #2 with a 47.9% YoY sales increase, while Strane moved from #8 to #5; this competitor movement upward as Roll One / R.O. drifted from #9 to #12 points to share consolidation at the top and implies that Roll One / R.O.’s path back to top-10 status will depend on sustaining the recent 4-rank rebound rather than relying on market lift.

Notable Products

Pungent Smile (3.5g) posted the standout movement in July 2026 with a 73.8% month-over-month surge to rank 2, while Chesapeake Crawler (3.5g) fell 61.7% to rank 10. Dosilato Pre-Roll (1g) held rank 1 despite no reported MoM figure, and Maryland Mantis (3.5g) slipped 3.6% at rank 8. With eight of the top ten coming from the Flower category and only one Pre-Roll in the lead, the skew implies Roll One / R.O. is leaning into Flower velocity while using a single flagship Pre-Roll as a traffic anchor.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.