Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Turn is stocked at 573 licensed dispensaries across California, New York, and Arizona, 430 of them in California, with the deepest coverage in Los Angeles, Long Beach, San Diego, Santa Ana, and Sacramento. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

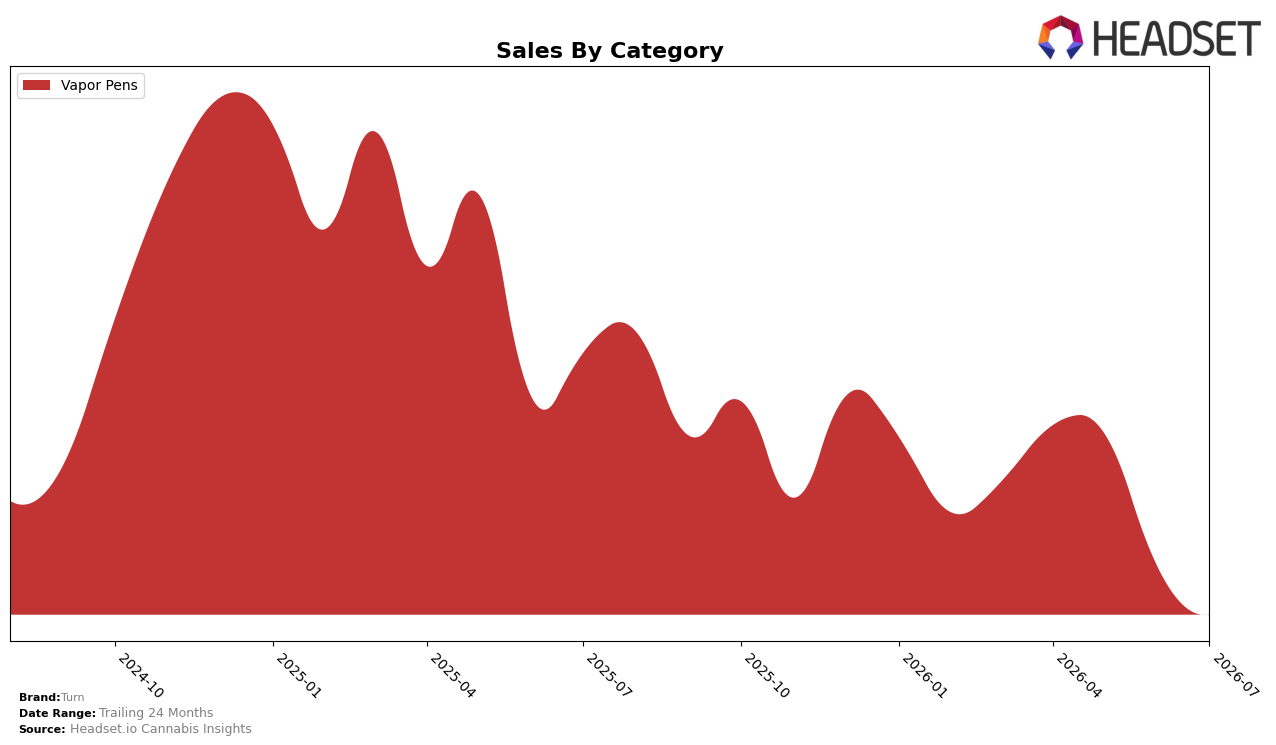

Turn’s July 2026 mix is fully concentrated in Vapor Pens at 100.0% share, with category sales down 25.2% year over year and 5.6% month over month, while average price fell 4.5% YoY to $25.78. Within California Vapor Pens, Turn held rank 11, indicating mid-pack positioning as both volume and price contracted simultaneously; the pattern implies the brand’s single-category exposure amplified the 25.2% YoY decline because no other categories offset the 5.6% MoM dip.

The combination of a 100.0% Vapor Pens reliance and an 11th-place rank in California suggests Turn is competing primarily on accessible pricing rather than premium laddering, given the 4.5% YoY price reduction paired with a sharper 25.2% sales decline. The implication is that July 2026 share defense likely hinges on stabilizing repeat volume within Vapor Pens rather than price-led gains, because the 5.6% MoM slide in a single category indicates sensitivity to short-term demand shifts that a diversified mix could have cushioned.

Competitive Landscape

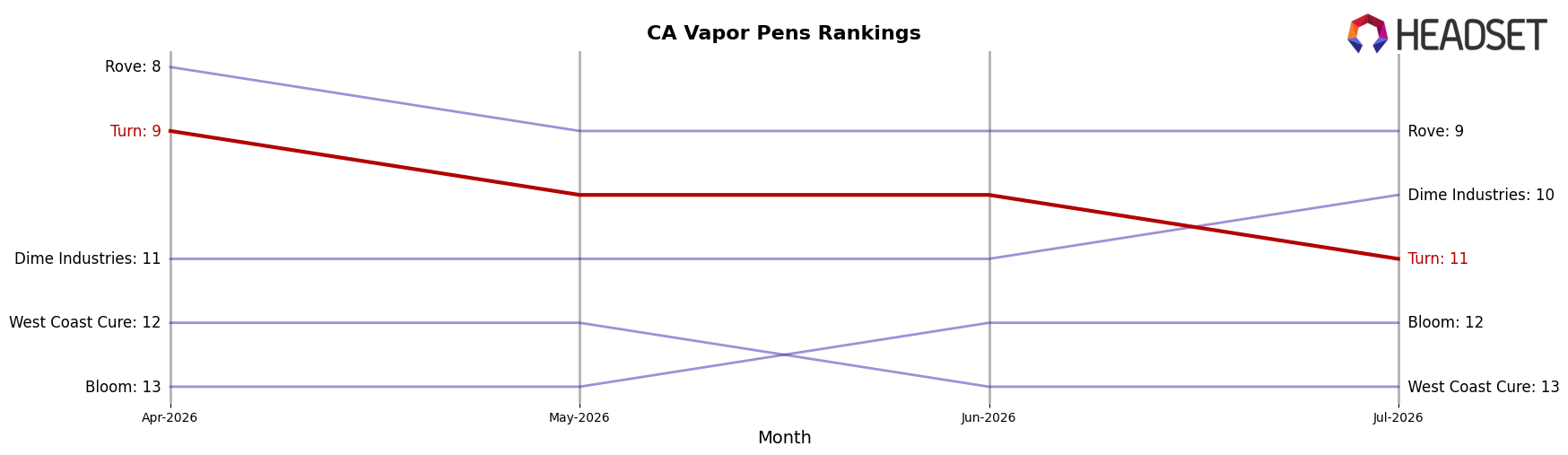

Turn sits at rank #11 in California Vapor Pens in July 2026, down 3 positions year over year from #8 and slipping 2 spots from #9 in April 2026, while its historical peak was #5 in December 2024. In contrast, STIIIZY held at #1 year over year despite a 6.8% YoY sales decline, and Jetty Extracts climbed from #4 to #3 with a 41.7% YoY sales increase; meanwhile, Plug Play fell from #3 to #4 with an 8.5% YoY sales decline. With rank erosion both year over year (-3 ranks) and quarter over quarter (-2 ranks), the trajectory implies Turn is losing relative velocity in a tier increasingly defined by rising share for faster-growing incumbents and challengers.

Notable Products

Turn Down - Granddaddy Purple Live Resin Disposable Pod (1g) posted the steepest slide in July 2026, down 20.6% MoM to rank 3 while Turn Down - Watermelon Sugar High Live Resin Disposable Pod (1g) rose 11.9% to hold rank 1. Turn Down - Dragon Fruit Acai Botanica Blend Live Resin Disposable Pod (1g) surged 38.1% MoM to rank 5, and Turn Up - Blue Dream Live Resin Disposable Pod (1g) gained 10.7% at rank 2, indicating momentum clustered near the top despite one sharp retreat. Eight of the top ten SKUs are Vapor Pens under the Turn Up/Turn Down families, and the category concentration alongside a $166,883 leader suggests Turn is consolidating demand into a few flagship terpene profiles rather than broadly expanding the assortment.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.