Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Gramlin is stocked at 308 licensed dispensaries across California, with the deepest coverage in Los Angeles, San Francisco, Sacramento, San Jose, and Costa Mesa. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

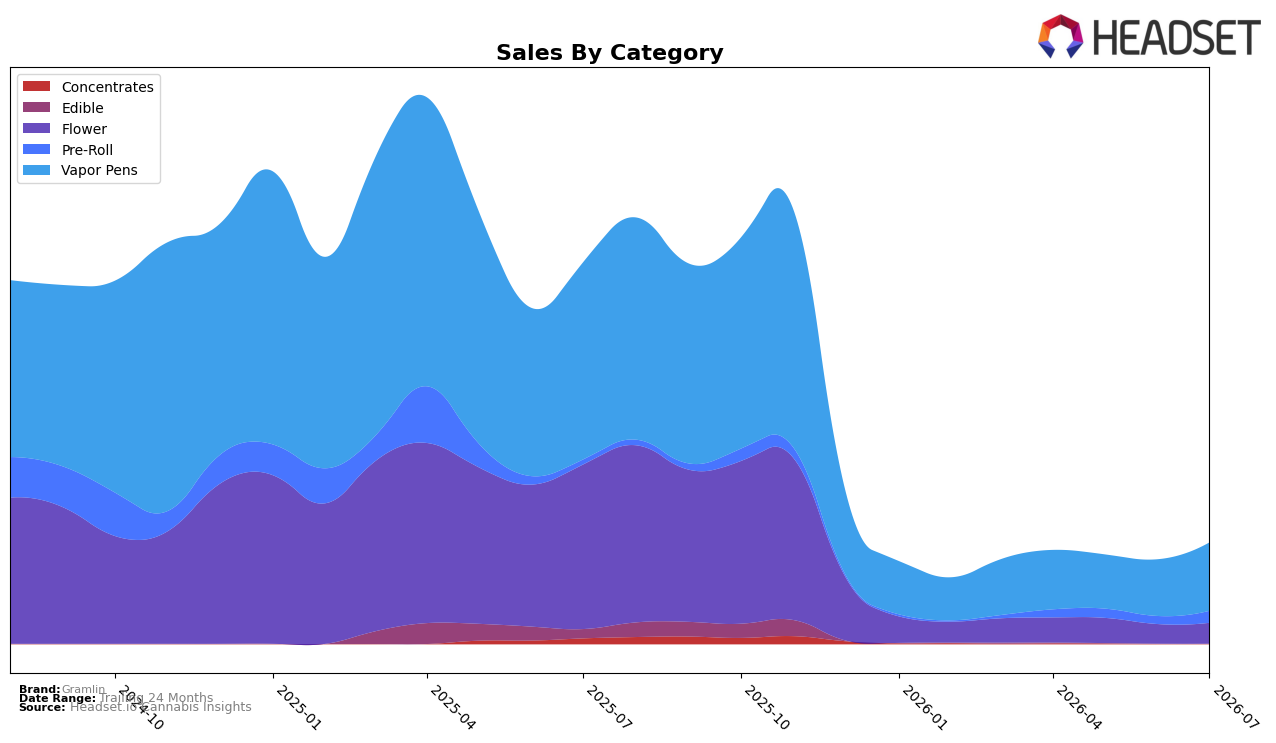

In July 2026, Gramlin concentrated two-thirds of sales in Vapor Pens at 67.74% share, where category sales declined 65.41% year over year but rose 20.57% month over month, while Flower held 20.53% share with a steeper 87.44% YoY drop and a 6.67% MoM lift. Pre-Roll expanded to 11.64% share on a 146.13% YoY surge and a 50.23% MoM jump, as fringe categories like Concentrates and Edible shrank to a combined 0.09% share with YoY declines of 99.08% and 99.58% respectively and MoM moves of -29.04% and -4.01%. With Gramlin ranked 22 in Vapor Pens in California and an average price down 12.63% YoY to $20.61, the pivot signals reliance on a single lead category to offset wider contraction, implying the brand is trading price for velocity to stabilize volume where it still converts.

The simultaneous 20.57% MoM rebound in Vapor Pens and 50.23% MoM acceleration in Pre-Roll, alongside an 87.44% YoY slide in Flower, implies a repositioning toward inhalables that emphasize convenience and price accessibility, with Flower de-prioritized. The 146.13% YoY Pre-Roll expansion, coupled with a 12.63% YoY price decrease and Vapor Pens at a 67.74% mix, indicates a barbell between cartridge-led trips and value-oriented pre-rolls, while near-exit shares in Concentrates (0.05%) and Edibles (0.04%) point to deliberate SKU pruning; the practical takeaway is that Gramlin’s route to restoring rank hinges on deepening Vapor Pens differentiation in California while using Pre-Roll momentum to recover lost Flower occasions.

Competitive Landscape

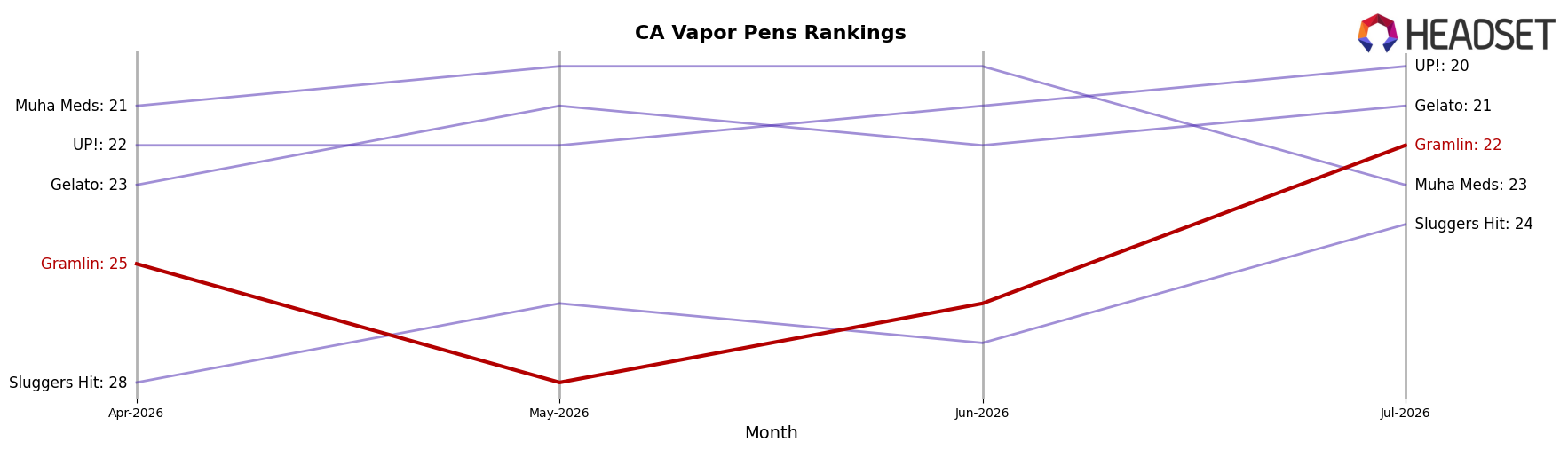

Gramlin sits at rank #22 in CA Vapor Pens in July 2026, down 13 spots year over year from #9, and up 3 positions versus April 2026 when it was #25; against a longer backdrop, the brand is still well below its April 2025 peak at #4, indicating a multi-quarter slide despite a recent quarter-on-quarter lift. In contrast, STIIIZY remains #1 with a year-over-year sales decline of 6.8% yet no rank change from #1, while Jetty Extracts climbed from #4 to #3 on 41.7% year-over-year sales growth; meanwhile, Plug Play slipped from #3 to #4 alongside an 8.5% year-over-year sales contraction. The pattern implies that Gramlin’s drop from #9 to #22 alongside competitors holding or improving top-5 positions points to share being ceded to faster-moving leaders, and the near-term uptick from #25 to #22 will need sustained acceleration to reverse the longer-term downtrend.

Notable Products

Strawberry Cough Distillate Disposable (1g) posted the sharpest movement in July 2026 with a +35.5% MoM surge to rank 4, while Pineapple Express Distillate Disposable (1g) rose +34.9% to hold rank 1. Blue Dream Distillate Disposable (1g) advanced +13.0% at rank 3 versus Raspberry OG Distillate Disposable (1g) at +11.4% in rank 2, and Sour Apple Pie Distillate Disposable (1g) slipped −4.1% at rank 8, indicating gains are concentrated in a handful of faster-rising SKUs. Nine of the top ten are Vapor Pens, concentrating share in a single category while Flower appears only once at rank 10 with Pink Certz x Shady Apples (3.5g) at $21,299. The pattern implies Gramlin is consolidating commercial emphasis around high-velocity vapor pen formats, using double-digit MoM risers at the top ranks to pull category weight while deprioritizing slower non-pen entries.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.