Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

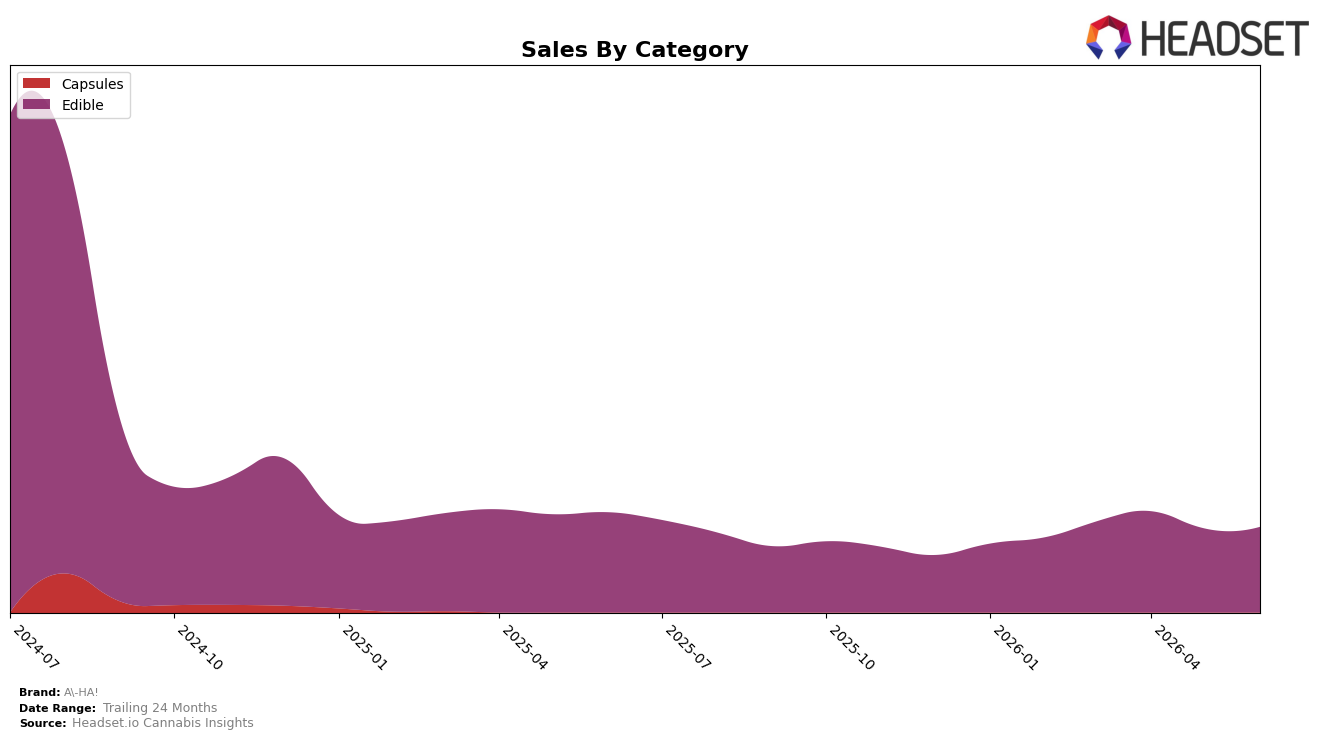

In June 2026, A-HA! was fully concentrated in Edible with a 100.0% category share, pairing a year-over-year sales change of -14.6% with a month-over-month uptick of 1.9%. Average price rose 38.2% year over year, while overall brand sales declined 14.6% in the same window, indicating mix-price tension inside a single-category footprint rather than cross-category cannibalization. With a 24-month sales change of -79.9% alongside a current Edible rank of 22 in Alberta, the pattern implies that price-led gains are not offsetting sustained volume erosion within the sole category focus.

These shifts imply A-HA!’s positioning is narrowing toward a price-elevated Edible strategy where incremental month-over-month stabilization (+1.9%) is insufficient against long-horizon contraction (-79.9% over 24 months) and a mid-pack rank position (22) in Alberta. Concentration at 100.0% in Edible limits diversification levers, so maintaining a 38.2% higher average price amid a -14.6% year-over-year sales decline signals the brand is trading on fewer, potentially higher-priced units rather than expanding buyer reach; the implication is that future share defense will hinge on either reducing the price-to-volume gap or reintroducing category breadth.

Competitive Landscape

A-HA! ranks #23 in ON Edible in June 2026, improving 2 positions year over year from #25 and slipping 1 spot since March 2026 from #24, while still 7 places below its peak at #16 in July 2024; this contrasts with Wyld, which climbed from #4 to #3 with 21.9% YoY sales growth, and Olli, which advanced from #7 to #4 alongside 120.7% YoY sales growth, indicating that competitors are converting sales momentum into rank gains faster than A-HA!; the pattern implies A-HA!’s modest rank gains are being outpaced, so without share-accretive moves its trajectory points to further mid-20s positioning rather than a return toward the #16 peak.

Notable Products

Raspberry Lemonade Hash Rosin Duos Gummies 2-Pack (10mg) posted the sharpest movement in June 2026 with a +210.4% month-over-month surge while sitting at rank 9, contrasted by Double Chocolate Cookie 10-Pack (300mg) plunging -80.2% at rank 8. The top rank is held by Milk Chocolate Live Rosin Waffle Cones 2-Pack (10mg) with +27.0% MoM, and five of the top ten are Cookie SKUs despite two cookie multipacks dropping -68.8% and -80.2%. The contrast between a single-serve gummy’s triple-digit jump and multi-pack cookie declines implies a pivot toward smaller-dose novelty formats over bulk baked goods.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.