Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

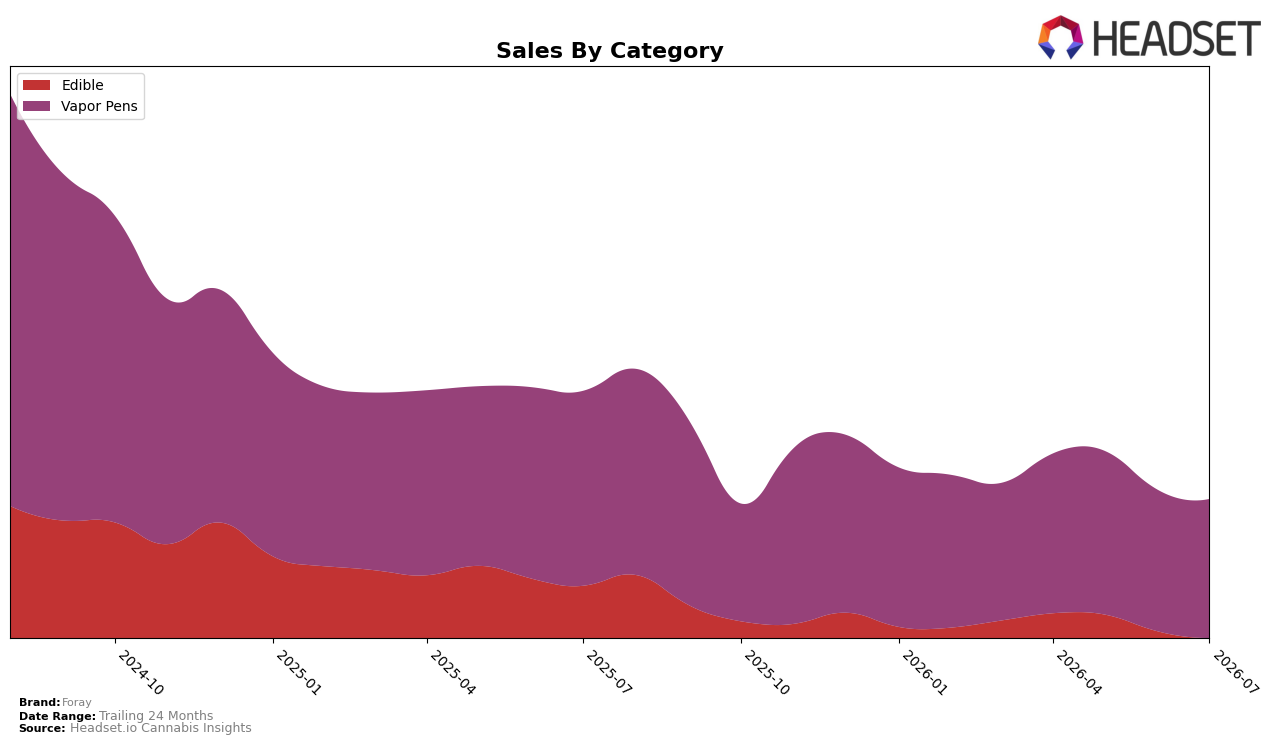

In July 2026, Foray’s mix leaned heavily into Vapor Pens at 71.20% share while Edible held 28.80% share, a concentration that accompanied a -19.36% year-over-year decline in Vapor Pens and a steeper -35.68% year-over-year drop in Edible. Month over month, Vapor Pens slipped -1.03% versus a larger -6.56% decline in Edible, indicating relative stability in the core category. Average price rose 0.50% year over year to $19.04 even as total brand sales fell -24.86% year over year, implying price was not the primary drag. With a Vapor Pens category rank of 21 in British Columbia, the mix suggests share defense in the lead category while Edible acts as a volatility source; the pattern implies Foray’s volume headwinds are concentrated in Edible, not Vapor Pens.

The combination of a -6.56% month-over-month contraction in Edible alongside only -1.03% in Vapor Pens, and a 71.20% sales share in Vapor Pens, points to a positioning anchored in inhalables where losses are comparatively contained. Given a -35.68% year-over-year fall in Edible against -19.36% in Vapor Pens, plus a 21st-place Vapor Pens rank in British Columbia, the brand’s current stance trades broader category diversification for concentration in a segment with smaller sequential decline. The implication is to prioritize Vapor Pens to stabilize rank and share while reframing Edible from core to opportunistic: tightening SKU count or price-pack architectures in Edible could reduce the -35.68% drag without diluting the 71.20% Vapor Pens anchor.

Competitive Landscape

Foray sits at rank #21 in BC Vapor Pens in July 2026, slipping 1 position year over year from #20, while holding flat versus three months ago at #21; this contrasts with Spinach climbing from #3 to #1 on 160.39% YoY sales growth and BoxHot easing from #1 to #2 alongside a -16.68% YoY decline. The category’s ladder also tightened as General Admission rose from #2 to #3 despite a -4.02% YoY sales change, and Back Forty / Back 40 Cannabis advanced from #7 to #5 with 43.10% YoY growth, while Foray’s peak of #13 back in July 2024 is now 8 places higher than its current slot. The pattern implies Foray’s rank trajectory is stagnating amid competitors moving up or consolidating above it, signaling that regaining territory toward its July 2024 peak will likely require share capture rather than passive category lift.

Notable Products

Tangie Crush Distillate Disposable (0.3g) posted the steepest movement in July 2026 with an -18.2% MoM drop at rank 4, while Fast Edi's- CBD/CBN/THC Blackberry Lavender Soft Chews 30-Pack (300mg CBD, 75mg CBN, 10mg THC) fell -12.5% at rank 3, indicating demand is rotating away from specific SKUs rather than the whole portfolio. Blackberry Cream Distillate Disposable (0.3g) held rank 1 with a -1.5% MoM slip as Balanced Mango Haze Distillate Disposable (0.3g) rose +16.5% at rank 6, and four of the top ten are Vapor Pens spanning ranks 1, 4, 6, and 7–9. Within pens, CBD/THC 1:1 Mango Haze Distillate Disposable Pen (0.3g) advanced +15.4% at rank 8 while Indica Distillate Disposable (0.3g) gained +11.5% at rank 7, contrasting with the -18.2% decline for Tangie Crush at rank 4. The mix points to Foray consolidating around inhalable dominance and balanced/cannabinoid-blended formats, with softness concentrated in a few flavored variants rather than a category-wide pullback.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.