Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

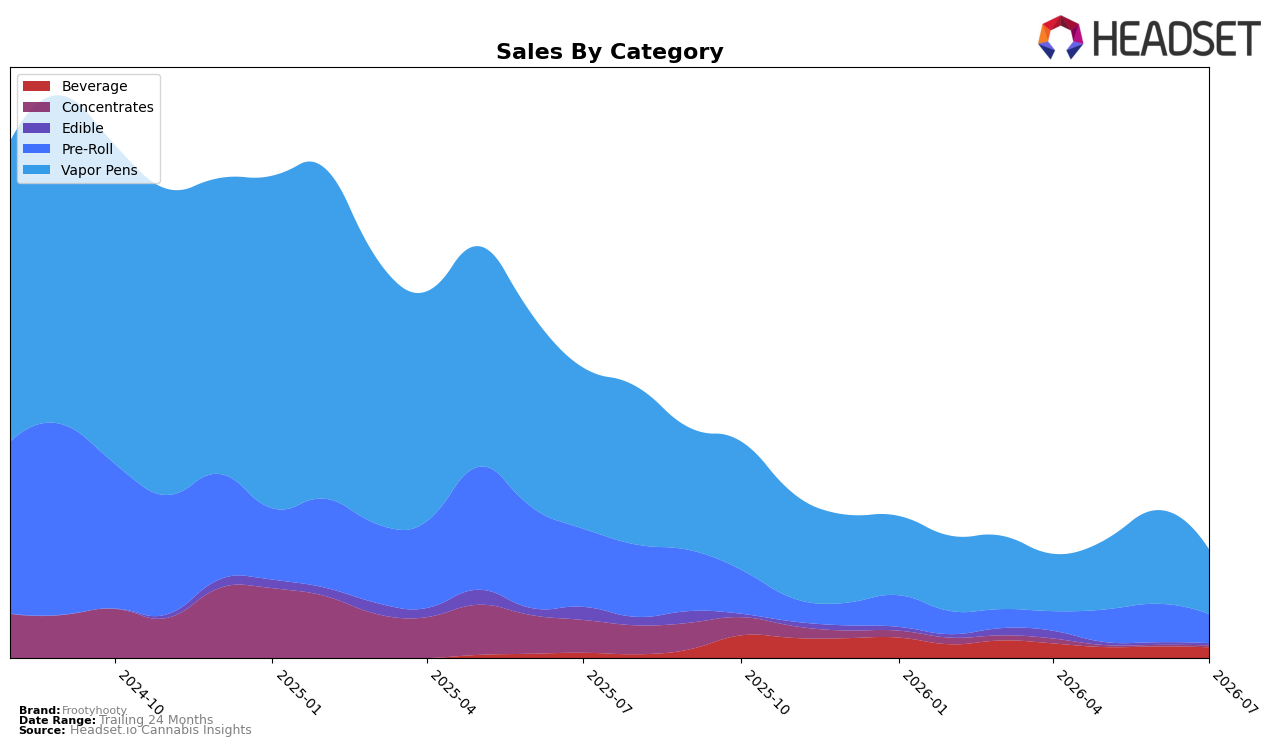

In July 2026, Frootyhooty concentrated 59.87% of sales in Vapor Pens with year-over-year down 59.99% and month-over-month down 31.06%, while Pre-Roll held 26.81% share with year-over-year down 62.99% and month-over-month down 24.36%. Beverage expanded year-over-year by 101.17% but slipped month-over-month by 7.37%, reaching 10.06% share, whereas Edible fell year-over-year by 85.19% and month-over-month by 19.00% to just 1.76% share. Concentrates remained small at 1.49% share but grew month-over-month by 28.01% despite a year-over-year decline of 95.06%. The mix indicates a pivot from collapsing Edible and Pre-Roll volumes toward Beverage and selective Concentrates recovery, implying category diversification as Vapor Pens pressure persists and average price contraction of 27.44% year-over-year sets a value-led footing.

With a 59.87% reliance on Vapor Pens alongside a rank of 29 in Vapor Pens in Saskatchewan, the brand is positioned mid-pack while Pre-Roll at 26.81% share compounds exposure to combustibles that fell 62.99% year-over-year. Beverage’s 101.17% year-over-year growth at a $5.02 price point and Concentrates’ 28.01% month-over-month lift suggest trading down on price and selective premium experimentation, respectively. The pattern implies Frootyhooty can mitigate a 62.85% brand sales decline year-over-year by reallocating toward Beverage to capture lower-price demand while using targeted SKUs in Concentrates to test higher-margin niches, reducing dependence on categories with 24.36% to 31.06% month-over-month declines.

Competitive Landscape

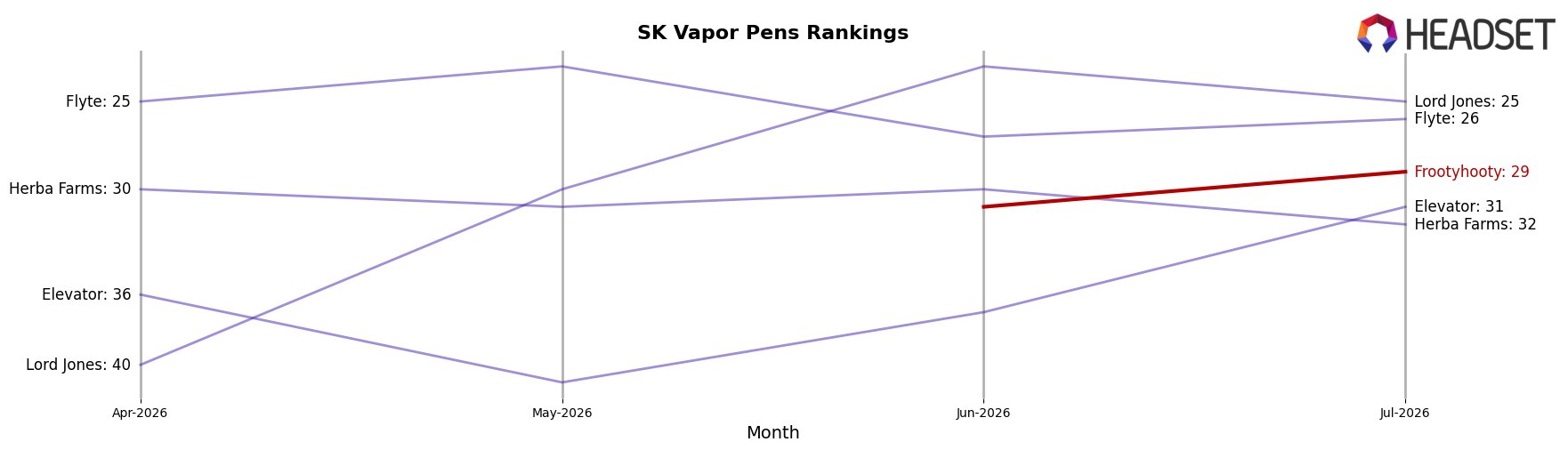

Frootyhooty sits at rank #29 in SK Vapor Pens in July 2026, improving 17 positions year over year from #46 and jumping 32 spots versus April 2026 when it was #61; meanwhile, Spinach held #1 both year over year at #1 and currently at #1, and JC Green Cannabis Company rose from #17 to #5 with 116.25% YoY sales growth while Frootyhooty reached a new peak rank of #29 in July 2026, indicating the brand’s trajectory is upward but still trailing leaders whose stability or rapid ascent signal escalating competitive pressure on mid-tier share.

Notable Products

Poppin Peach Splash Zero Soda (10mg THC, 12oz, 355ml) set the tone with a rank of 1 despite a -91.6% month-over-month slide, while Wild Watermelon Coconut Live Rosin + Disty Cartridge (1g) fell to rank 3 with a -14.7% decline, indicating a pullback concentrated at the top. Splash Zero Pink Lemonade Sparkling Beverage (10mg THC, 12oz, 355ml) at rank 2 dropped -13.5%, and Poppin Peach Full Spectrum Live Rosin Cartridge (1g) at rank 4 contracted -39.3%, with four of the top five positions occupied by Beverage and Vapor Pens SKUs together. The Pre-Roll tier was mixed, with Froot Basket Infused Pre-Roll 5-Pack (2.5g) at rank 6 growing 8.3% while Cherry Lipgloss Infused Pre-Roll 3-Pack (1.5g) at rank 7 declined -16.9%, signaling a selective shift within formats rather than a uniform category trend. The pattern implies Frootyhooty is overexposed to volatile Beverage and Vapor Pens leaders and may need to lean into steadier Pre-Roll momentum to stabilize the mix.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.