Market Insights Snapshot

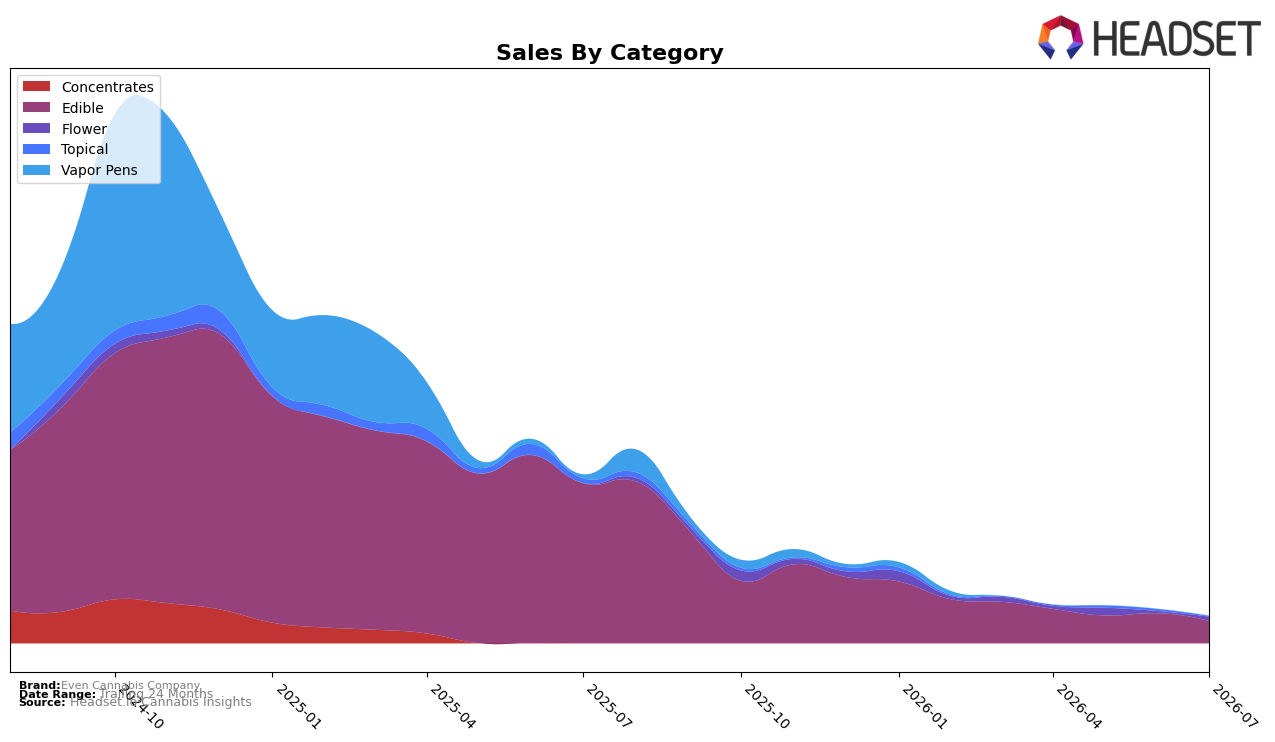

In July 2026, Even Cannabis Company concentrated 82.38% of sales in Edible, with category sales down 86.32% year over year and 26.25% month over month, while Flower expanded to 15.62% share on a 106.92% month-over-month surge from a small base and Topical contracted to 2.00% share with an 88.13% year-over-year decline and a 70.39% month-over-month drop. Against a brand-level sales decline of 84.20% year over year and a 17.51% increase in average price, the category mix implies reliance on Edible is amplifying the contraction, and the abrupt Flower upswing is the only offset but not yet large enough to rebalance risk.

The shift toward a higher-priced, niche-heavy basket—Flower at an average price of $29.92 versus Edible at $15.10 and Topical at $33.92—alongside Edible’s 26.25% month-over-month fall suggests price-led value loss in the primary category while the 106.92% Flower rebound points to traction in fewer, higher-priced SKUs. With Ontario as the top market and no current rank reported in Edible, the pattern implies Even Cannabis Company should accelerate SKU and distribution focus in Flower to lift share while progressively de-risking from Edible, because a 15.62% share carried by rapid month-over-month growth can reposition the mix faster than waiting for an 86.32% year-over-year Edible decline to stabilize.

Competitive Landscape

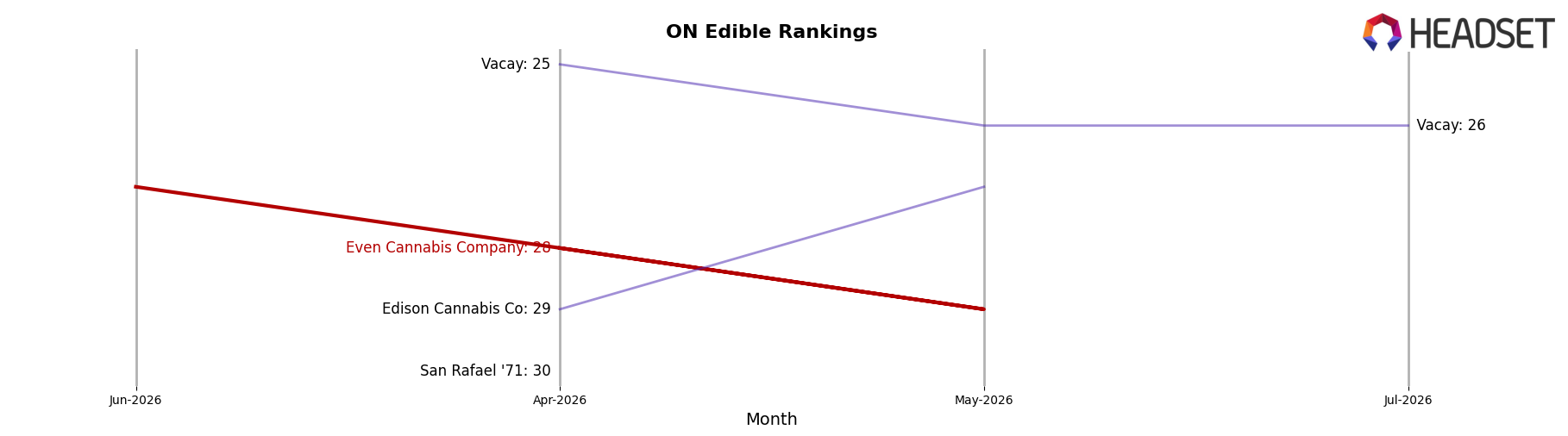

Even Cannabis Company sits at rank #27 in ON Edible for July 2026, slipping 1 position year over year from #26 while improving 1 spot versus three months ago from #28, and it remains 3 ranks below its peak of #24 from August 2025; meanwhile, category leaders moved in the opposite direction, with Spinach holding #1 with a 10.8% YoY sales increase and Wyld climbing from #4 to #3 on 13.0% YoY growth, while Fly North surged from #15 to #5 alongside a 607.3% YoY gain. The combination of a 1-rank YoY decline and only a 1-rank quarter-on-quarter lift, as faster-rising competitors consolidate top-5 positions, implies Even Cannabis Company is drifting toward a lower-mid tier unless it converts incremental rank stability into sharper share capture.

Notable Products

CBD Blue Raspberry Lemonade Fast Acting Gummies 50-Pack (1500mg CBD) posted the standout move in July 2026 with a +343.6% month-over-month surge to rank 4, while Biggies Cherry Cola Live Resin Soft Chews 4-Pack (10mg) fell -64.8% to rank 2, creating a split where growth is concentrated in one Edible SKU as another contracts. Gary Satan (3.5g) climbed +106.9% to rank 3, and with three of the top five ranked products sitting in Edibles, the category now anchors velocity even as the rank-1 CBD Mango Lemonade Gummies 30-Pack (750mg CBD) declined -23.9%.

The mixed signals—one Edible at +343.6% and another at -64.8%, plus a Flower entry at +106.9%—imply a pivot toward higher-variance launches and formats that can spike quickly, suggesting Even Cannabis Company is leaning into fast-acting Edible innovation while allowing legacy gummies to deflate to fund momentum bets.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.