Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

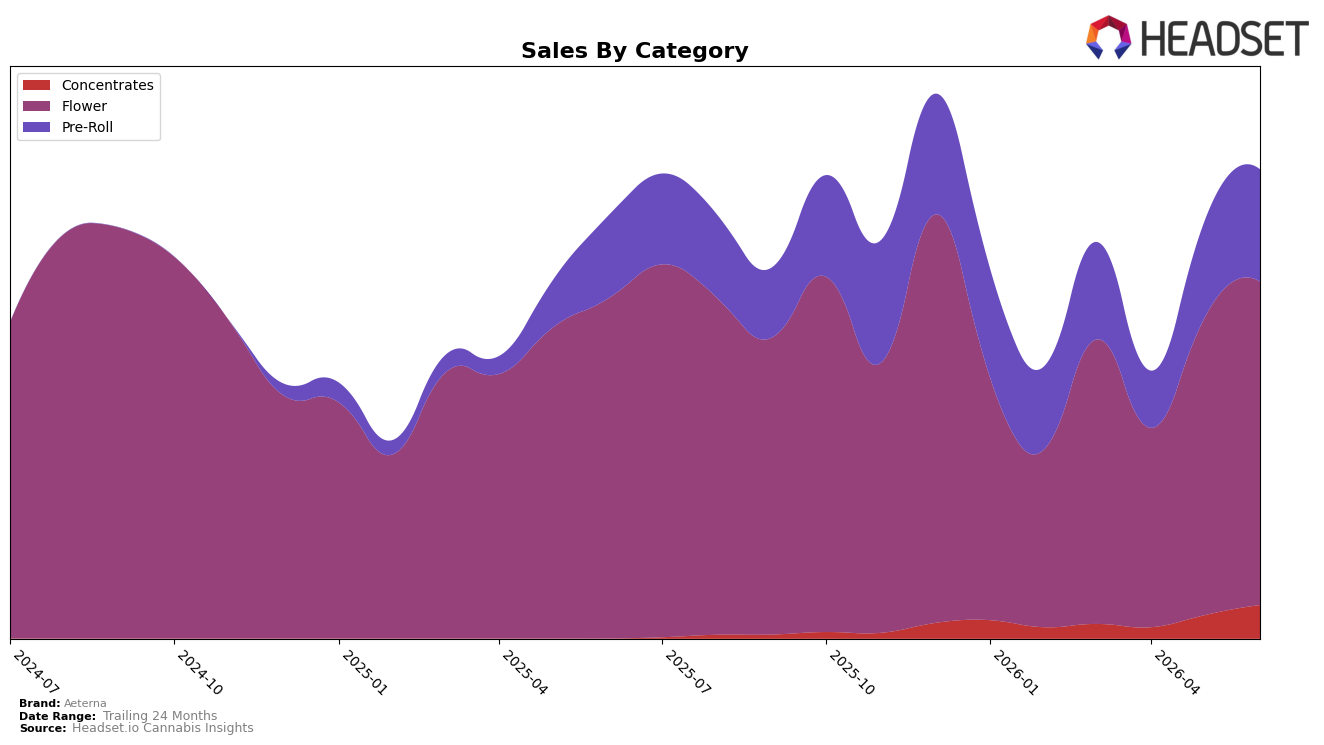

Aeterna’s mix in June 2026 tilted toward Flower at 68.97% share with month-over-month growth of 8.75% but a year-over-year decline of 4.88%, while Pre-Roll expanded to 23.90% share with 15.93% MoM and 35.91% YoY growth; Concentrates, though only 7.13% share, posted a 43.58% MoM surge with no year-over-year comp available. Despite an average price down 19.82% YoY to $26.37 and overall brand sales up 10.99% YoY, the mix shift toward faster-growing Pre-Roll and a rapidly accelerating Concentrates line implies volume-led gains are offsetting Flower softness and price compression.

The pattern suggests Aeterna is repositioning from a Flower-centric profile toward a value-accessible, multi-format portfolio, using Pre-Roll’s 35.91% YoY and Concentrates’ 43.58% MoM expansions to rebalance exposure away from Flower’s 4.88% YoY contraction. With Flower still commanding 68.97% share but ranking 44th in New York, prioritizing continued Pre-Roll momentum and Concentrates trial can reduce reliance on a category with slower YoY traction, implying a push to defend shelf presence via depth in faster-turn formats while Flower serves as a scale anchor rather than the primary growth engine.

Competitive Landscape

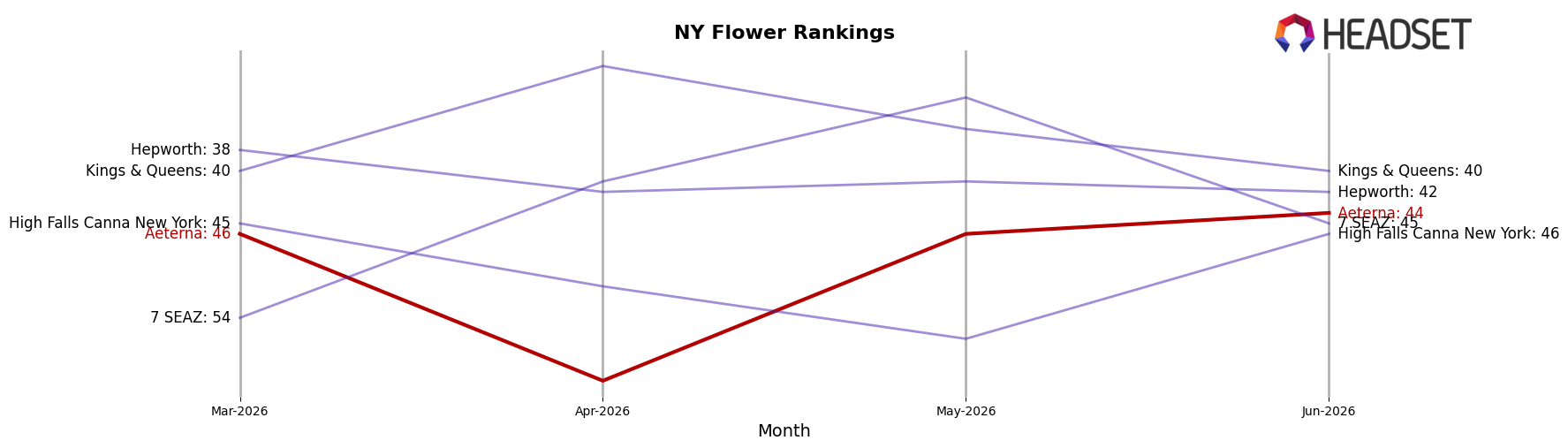

Aeterna ranks #44 in NY Flower in June 2026, falling 10 positions year over year from #34 and slipping 2 spots since March 2026 from #46 to #44, while remaining far below its peak of #14 from June 2024; in contrast, Find. moved up to #1 from #3 alongside a 35.6% YoY sales increase, and RYTHM advanced to #5 from #10 with a 40.6% YoY gain, whereas Dank. By Definition slid to #3 from #1 with a 50.7% YoY sales decline, indicating that Aeterna’s downward rank drift amid both upward and downward competitor shifts implies share is concentrating among faster-moving leaders and that Aeterna must arrest further position loss to reenter the top 20.

Notable Products

Papaya Cake (3.5g) set the sharpest move in June 2026 with a -29.2% MoM drop while holding rank 8, signaling a retreat in one Flower SKU even as Pre-Roll momentum lifted the leaderboard with rank 1 and rank 3 both occupied by Pre-Roll items. Gelato 33 Pre-Roll (1g) rose to rank 1 with +45.8% MoM, outpacing the Flower runner-up at rank 2 by four rank positions and indicating that value and convenience formats are capturing share. Apple Fritter (3.5g) advanced to rank 2 on +41.1% MoM and delivered $58,901, yet four of the top ten are Flower SKUs while three are Pre-Roll, pointing to a split demand curve where Pre-Roll gains are pulling rank faster than Flower. The pattern implies Aeterna is tilting toward faster-turn Pre-Roll variants for growth while maintaining broad coverage in Flower to preserve basket reach.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.