Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

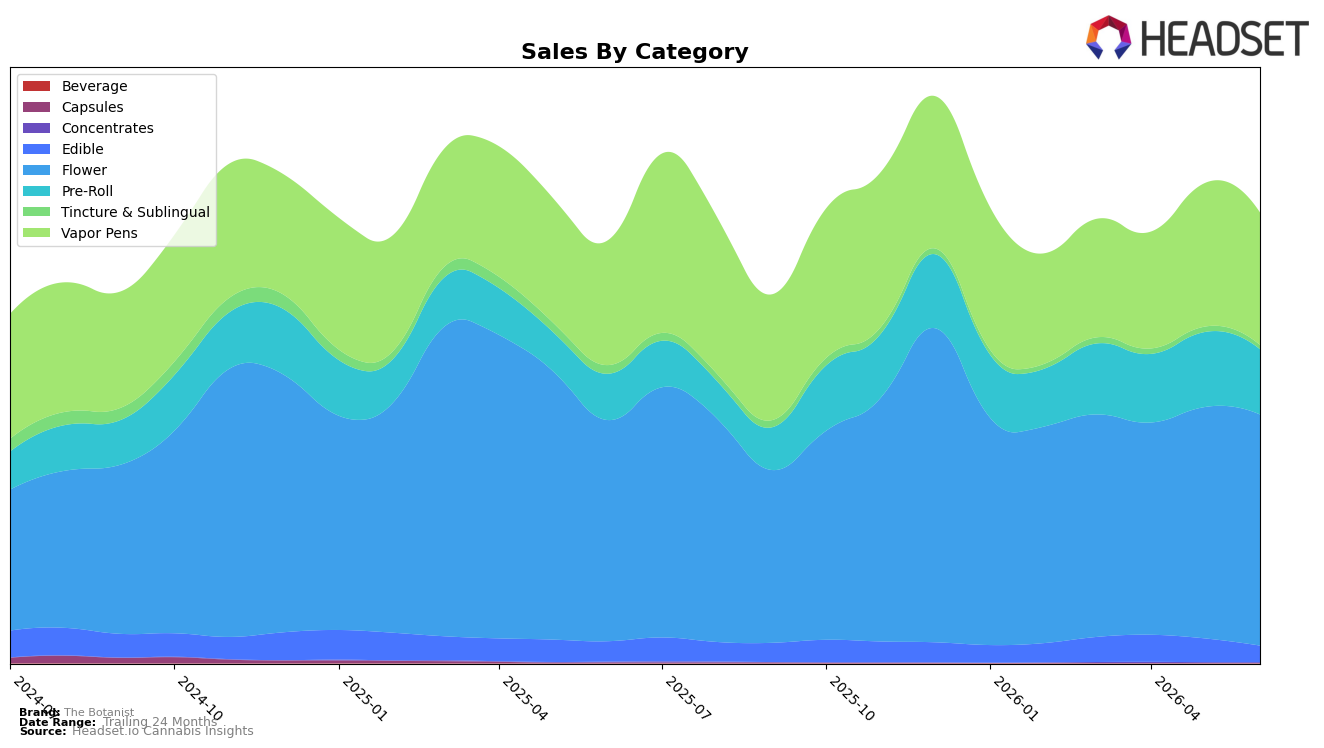

The Botanist’s mix in June 2026 tilted toward Flower at 51.43% share with 4.53% YoY growth but a -0.08% MoM dip, while Vapor Pens held 29.45% share with 5.93% YoY growth and a steeper -7.71% MoM change. Pre-Roll expanded to 14.47% share on 41.07% YoY growth but contracted -13.10% MoM, and Edible fell to 3.63% share with -19.26% YoY and -30.68% MoM declines; Tincture & Sublingual slid to 0.89% share with -52.16% YoY and -21.58% MoM, and Concentrates remained marginal at 0.13% share with 29.54% YoY but -2.76% MoM. With brand sales up 6.54% YoY alongside a -12.92% YoY drop in average price, June 2026 indicates a volume-led profile concentrated in Flower and Pre-Roll, but near-term momentum is constrained by broad MoM pullbacks across all categories.

This mix implies The Botanist is anchoring on value-accessible inhalables, with Flower’s rank at 14 in Illinois setting a mid-pack benchmark while the 41.07% YoY surge in Pre-Roll and 5.93% YoY in Vapor Pens offset Edible’s -19.26% YoY erosion. The brand’s -12.92% YoY pricing and -7.71% MoM pressure in Vapor Pens, combined with a -13.10% MoM reset in Pre-Roll, point to promotional or mix-down tactics that lift unit velocity but cap premium realization; the outcome is a defensible share position in Flower-led baskets, with risk concentrated in non-inhalable formats where -30.68% MoM in Edible and -21.58% MoM in Tincture & Sublingual weaken diversification.

Competitive Landscape

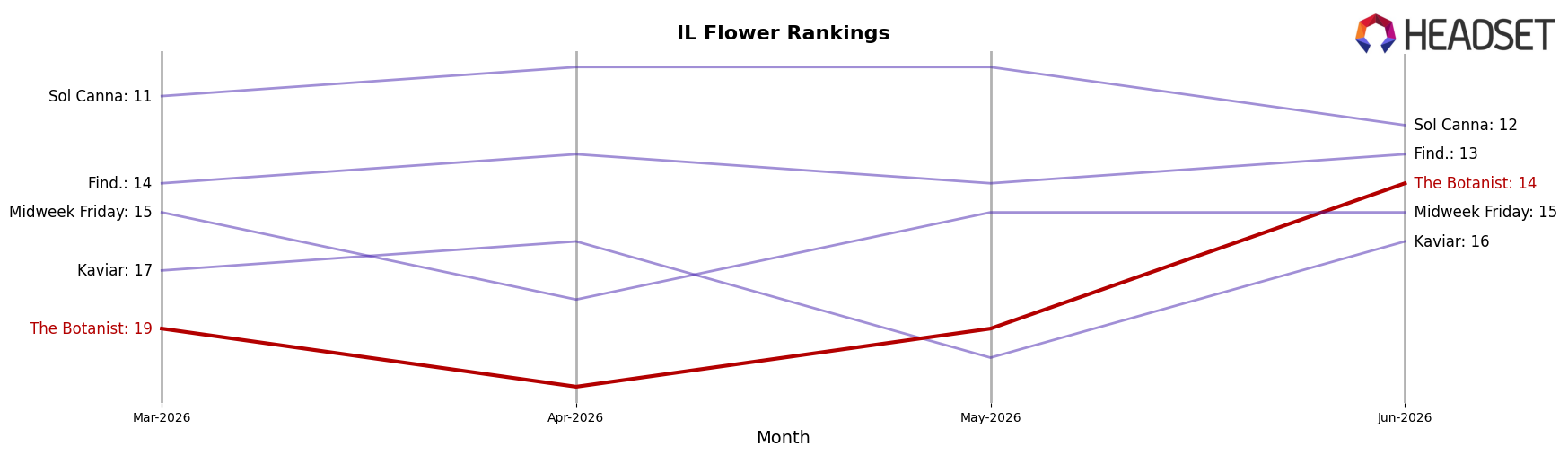

The Botanist sits at rank #14 in Illinois Flower in June 2026, improving 9 positions year over year from #23 and moving up 5 spots since March 2026 from #19, while also hitting its peak rank of #14 this month. Against leaders, High Supply / Supply held #1 both this year and last with sales up 32.1% year over year, and Good Green rose from #4 to #3 with 30.9% sales growth, contrasting with The Botanist’s climb from outside the top 20 into the mid-teens. Meanwhile, Simply Herb slipped from #3 to #4 with a 16.8% sales decline as &Shine advanced from #10 to #5 with 28.5% growth, indicating the competitive middle tier is churning while the top two remain stable. The pattern implies The Botanist’s current upward trajectory is tied to momentum within a reshuffling mid-pack, but breaking into the top 10 will require outpacing rivals posting 28%–32% growth while avoiding declines like the 16.8% seen by a nearby competitor.

Notable Products

Chem Chillz #17 Distillate Infused Pre-Roll 2-Pack (1g) posted the standout move in June 2026 with a +225.8% month-over-month surge to rank 1, while Grapple Pie (3.5g) slid -18.9% to rank 2. LA Kush Cake (3.5g) fell -30.5% and the Grapple Pie Pre-Roll (1g) dropped -34.1% to rank 9, versus Mint Sherbert (3.5g) rising +44.8% at rank 4. Four of the top ten are Pre-Roll SKUs, and that tilt toward Pre-Rolls alongside a vapor pen at rank 6 implies a portfolio shift from bulk Flower reliance toward faster-turn inhalables and form-factor variety that can offset Flower volatility.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.