Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Alchemy (Ieso) is stocked at 196 licensed dispensaries across Illinois, Massachusetts, and 5 other states, 106 of them in Illinois, with the deepest coverage in Chicago, Springfield, Naperville, Addison, and Arlington Heights. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

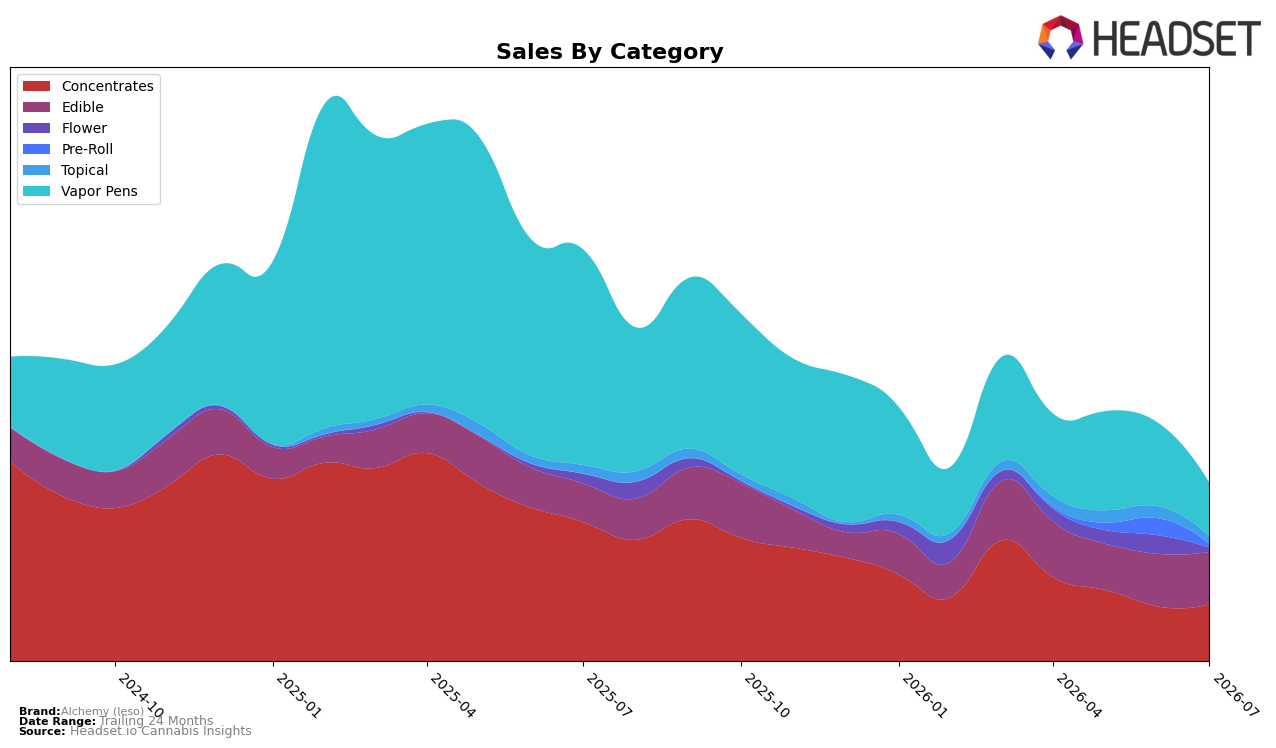

Alchemy (Ieso) concentrated its July 2026 mix around three pillars: Concentrates at 31.97% share (month-over-month up 4.01% but year-over-year down 59.28%), Vapor Pens at 30.48% share (month-over-month down 35.47% and year-over-year down 75.04%), and Edible at 29.55% share (year-over-year up 35.91% with a slight month-over-month dip of 0.32%). Smaller lines compressed sharply: Topical fell 38.89% month-over-month and 12.31% year-over-year to 4.06% share, while Flower contracted 79.40% month-over-month and 60.01% year-over-year to 2.13% share, and Pre-Roll declined 80.93% month-over-month to 1.80% share with no year-over-year read. With overall brand sales down 56.96% year-over-year and average price down 34.32%, this mix implies a deliberate pivot toward Edible resilience while trimming exposure to more volatile inhalables.

In July 2026, the rise of Edible (up 35.91% year-over-year) alongside the month-over-month pullback in Vapor Pens (down 35.47%) and the slight month-over-month lift in Concentrates (up 4.01%) suggests Alchemy (Ieso) is cushioning revenue with steadier, lower-priced formats while maintaining a presence in its lead category. The 15th rank in Concentrates in Illinois combined with a 59.28% year-over-year decline there signals mid-pack positioning that may be sustained by selective depth rather than broad category sprawl; the concurrent 79.40% month-over-month Flower contraction and 38.89% month-over-month Topical drop indicate a pruning strategy that reallocates attention to categories with either near-term momentum or defensible share. Net effect: the brand is trading breadth for defensibility, leaning into Edible growth and stabilizing Concentrates to offset inhalable volatility at lower price points.

Competitive Landscape

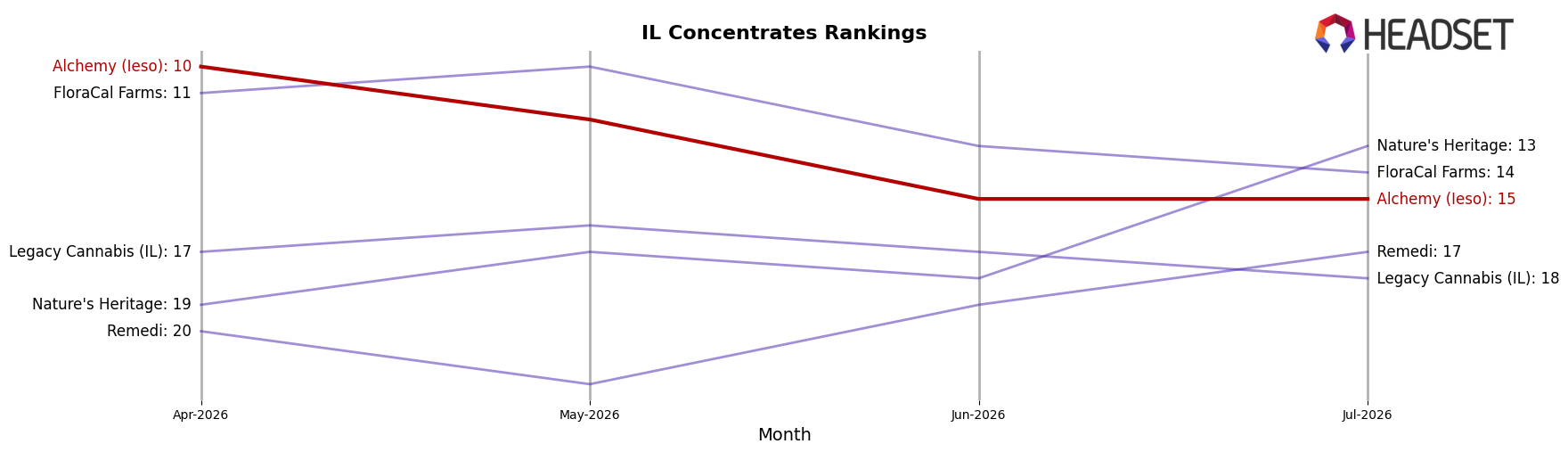

Alchemy (Ieso) sits at rank #15 in IL Concentrates in July 2026, down 10 positions from rank #5 year over year, and 5 spots softer than April 2026 when it held #10; the brand’s peak of #4 in September 2025 underscores a two-step slide from peak-to-current and a ten-spot drop versus July 2025. Meanwhile, Aeriz held #1 year over year and remains #1, and IC Collective jumped from #8 to #3 with 93.1% YoY sales growth, indicating Alchemy (Ieso) lost relative share while faster risers compressed the middle ranks; the trajectory from #4 to #15 implies a repositioning is required to re-enter the top 10 as incumbents gain and climbers overtake.

Notable Products

Sleep Potion - CBN/THC 5:1 Black Raspberry Gummies 20-Pack (500mg CBN, 100mg THC) posted a -17.7% month-over-month change and slipped to rank 2, while Stella Blue Cured Budder (1g) fell -21.8% to rank 7. In parallel, CBD/THC 20:1 Orange Pineapple Healing Gummies 20-pack (2000mg CBD,100mg THC) declined -19.8% at rank 3, contrasting with CBD/CBG/THC 3:2:1 Cranberry Lime Gummies 20-Pack (300mg CBD, 200mg CBG, 100mg THC) rising +21.9% to rank 1. With eight of the top ten rooted in functional Edible formats and Vapor Pens slipping with a -18.2% drop at rank 9, the mix points to Alchemy (Ieso) consolidating around high-CBD and sleep-aid gummies while de-emphasizing inhalables despite a single SKU still clearing $12,000.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.