Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

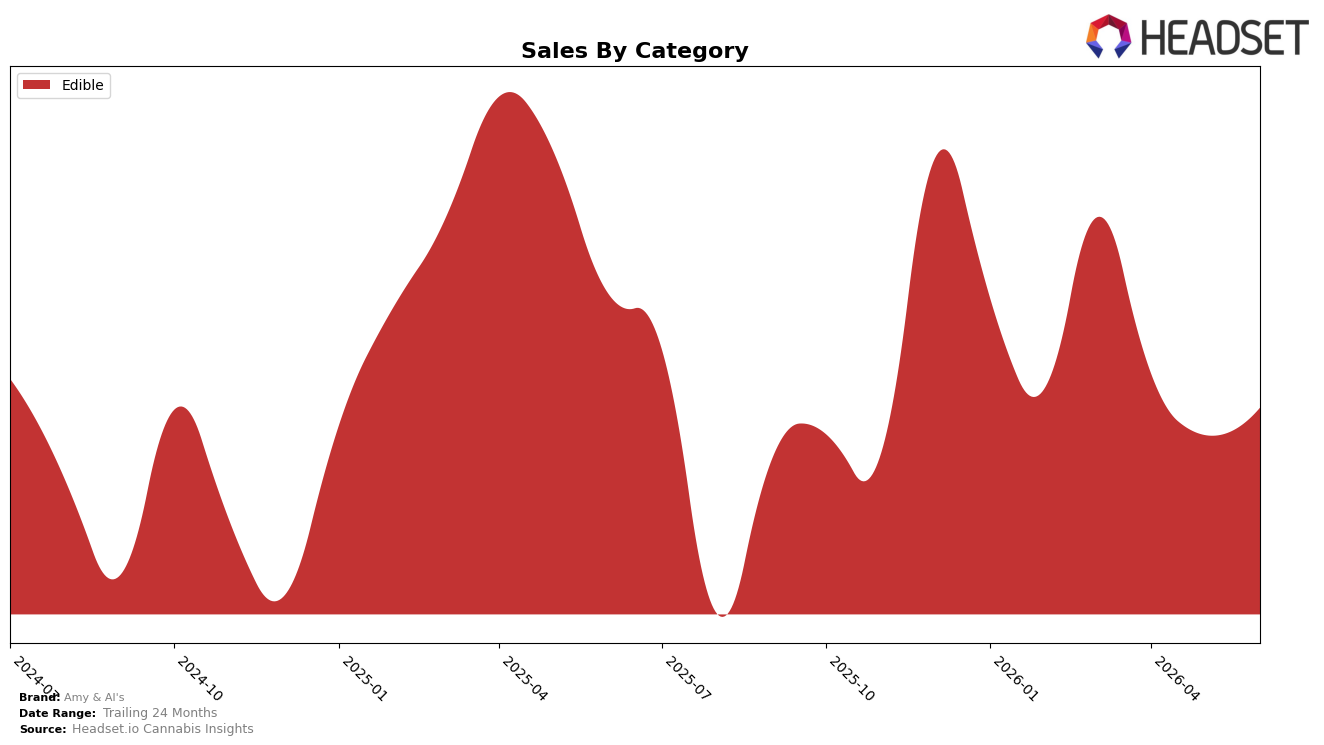

In June 2026, Amy & Al's operated as a single-category brand with Edible at 100.0% mix, posting a year-over-year sales change of -10.9% alongside a month-over-month uptick of 3.0%. Average price rose 32.3% year over year to $11.10, while the brand’s 24‑month sales change of -6.0% trails the shorter-term -10.9% decline, indicating a steeper recent contraction even as June’s MoM gain of 3.0% signals some intra-quarter stabilization. With Edible concentrated entirely in Arizona and a category rank of 22, the pattern implies price-led compression has not fully offset volume pressure, and a one-category footprint amplifies exposure to Edible-specific headwinds.

The mix concentration at 100.0% Edible combined with a 32.3% YoY price increase and a -10.9% YoY sales shift suggests the brand is trading up within Edibles rather than expanding breadth, and the 3.0% MoM lift indicates tactical gains that may be sensitive to promotional cadence rather than structural share growth at rank 22. Given the 24‑month sales change of -6.0% versus the sharper -10.9% in the last year, positioning skews toward maintaining price architecture while ceding some volume, implying the path to improve rank in Arizona Edibles likely depends on targeted pack-size and form-factor moves within Edibles rather than cross-category diversification in the near term.

Competitive Landscape

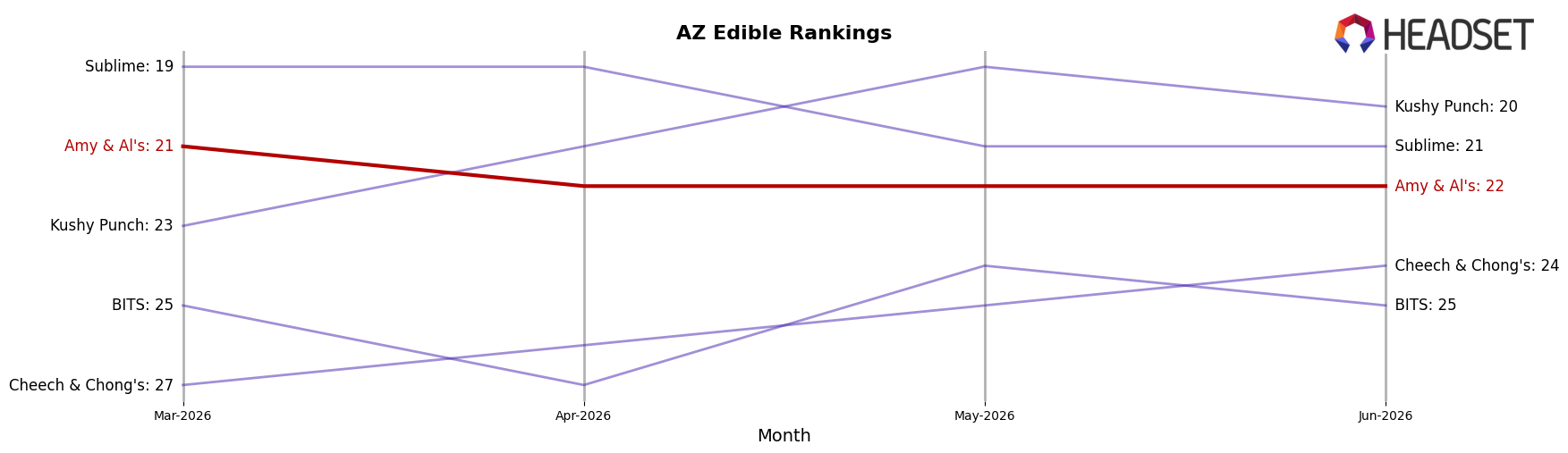

Amy & Al's sits at rank #22 in AZ Edible for June 2026, a 5-place YoY slide from #17, and down 1 spot from March 2026’s #21, while also sitting 6 places below its peak at #16 in May 2025; by contrast, Wyld held #1 YoY to #1 despite a 15.3% sales decline and Baked Bros climbed from #4 to #3 on 30.9% YoY growth, indicating competitors are either consolidating top ranks or gaining ground even with mixed sales trends. With OGEEZ steady at #2 alongside 15.1% YoY growth and Wana improving from #6 to #5 on 10.8% growth, Amy & Al's relative drift from #21 to #22 over the last three months and from #17 YoY implies share is leaking to brands improving velocity or defending distribution at higher tiers, and the current trajectory suggests further rank pressure unless mix or placement shifts counter the gradual slippage.

Notable Products

Hybrid Brownie Bites (1000mg) delivered the standout move in June 2026 with a 94.3% month-over-month jump, vaulting into rank 9, while Hybrid Brownie 10-Pack (100mg) fell 21.2% but held rank 1. Dark Chocolate Brownie (400mg) climbed 43.4% to rank 5, contrasting with the modest 0.6% uptick for Hybrid Chocolate Chip Cookie 10-Pack (100mg) at rank 3. Eight of the top ten SKUs are Edibles from cookie or brownie families, and the $32,409 posted by Hybrid Brownie 10-Pack (100mg) concentrates value at the top despite divergent growth rates. The pattern implies a pivot toward higher-dosage novelty within core baked-goods, with flagship volume anchoring revenue while potency-led variants expand the opportunity set.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.