Market Insights Snapshot

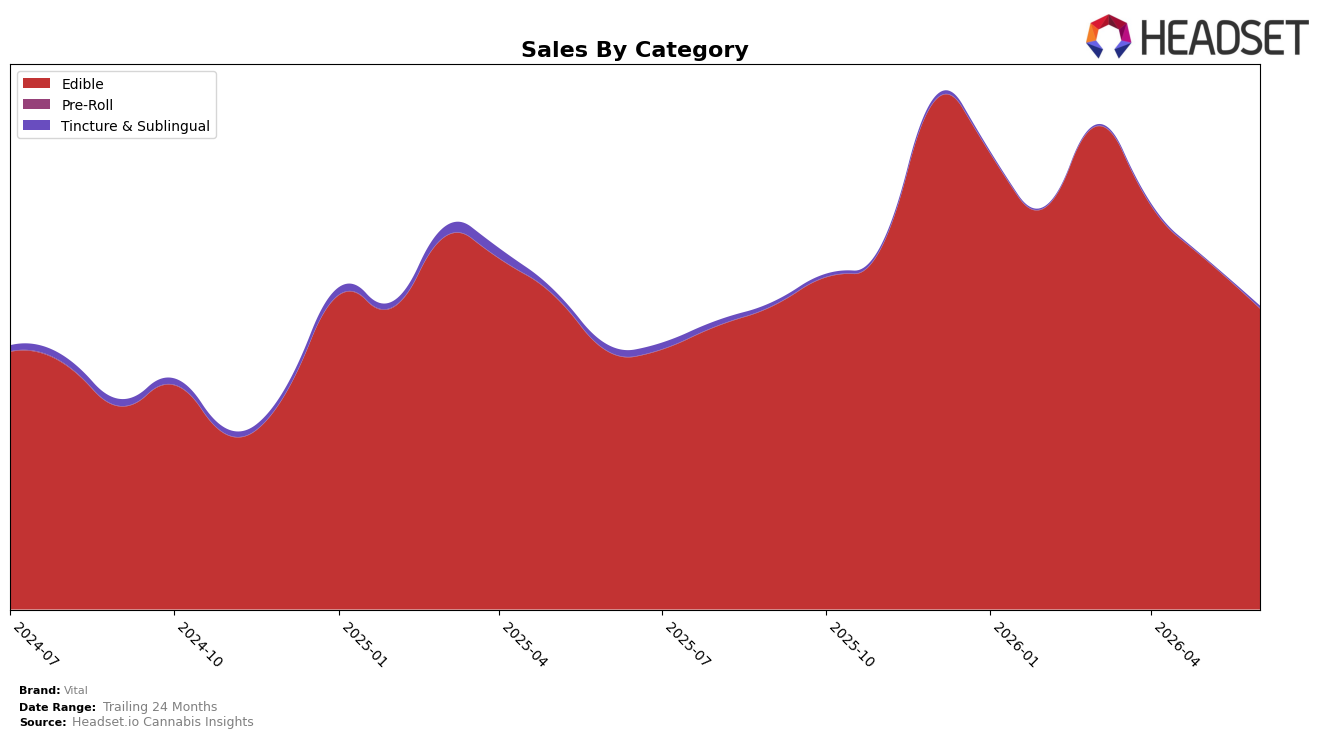

Vital concentrated 99.30% of June 2026 sales in Edible, up 16.79% year over year but down 14.19% month over month, while the much smaller Tincture & Sublingual segment held 0.70% share with a 64.64% year-over-year decline but a 193.63% month-over-month surge. The brand’s overall year-over-year sales rose 14.95% alongside a 7.14% year-over-year drop in average price, indicating volume expansion within Edible despite a June pullback, and positioning Vital’s Edible-led mix to benefit from lower price points even as category breadth remains narrow.

With Edible at 99.30% share and Tincture & Sublingual rebounding month over month by 193.63% off a small base, Vital’s risk concentrates in one category, but the price elasticity implied by a 7.14% year-over-year price decrease and 14.95% sales growth suggests defensibility if Edible demand softens further by another 14.19% month over month. In Arizona Edible, Vital’s rank at 14 indicates mid-tier visibility, so the immediate implication is to use the Edible scale to selectively seed Tincture & Sublingual where early gains can compound share from 0.70% without materially compromising the Edible-driven position.

Competitive Landscape

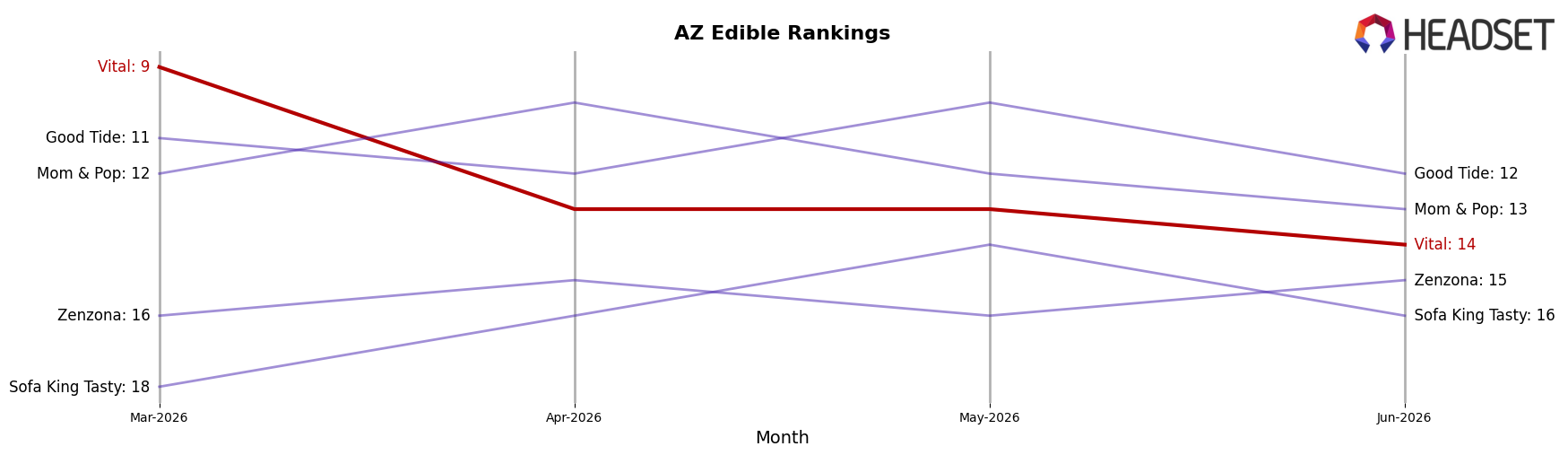

Vital sits at rank #14 in Arizona Edible for June 2026, down 1 position year over year from #13 and 5 positions below its March 2026 rank of #9, despite having peaked at #8 in December 2025; meanwhile, Wyld holds #1 but with a -15.3% year-over-year sales change and Baked Bros moved up from #4 to #3 with +30.9% year-over-year sales, indicating Vital’s mid-year slide is less about category contraction and more about share being ceded to upwardly mobile rivals; the implication is that without a catalyst, the trajectory from #9 in March 2026 to #14 in June 2026 points to continued rank erosion as competitors consolidate gains.

Notable Products

Indica Watermelon Gummies 10-Pack (100mg) posted the steepest decline in June 2026 at -85.9% MoM, falling to rank 10, while Peach Fast Acting Gummies 10-Pack (100mg) also collapsed -71.7% MoM at rank 8; this sharp deterioration in two fast-acting or flavor-variant SKUs implies volatility at the tail of the lineup. At the top, Tropical Mango RSO Gummies 10-Pack (100mg) held rank 1 despite a -9.0% MoM dip and Grape Fast Acting Gummies 10-Pack (100mg) stayed at rank 2 with a -5.1% MoM change, indicating that leadership is coming from entrenched flavors rather than growth from innovation. Six of the top ten are Edible gummies featuring functional or pectin formulations, and Indica Sour Blue Raspberry Pectin Gummies 10-Pack (100mg) was the only notable riser at +12.3% MoM to rank 6, suggesting shopper preference is consolidating toward pectin and functional blends over fast-acting variants. The mix points to a commercial direction prioritizing core, steady Edible formats while pruning underperforming fast-acting and watermelon/peach extensions to stabilize velocity.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.