Where to Buy

Sofa King Tasty is stocked at 22 licensed dispensaries across Arizona, with the deepest coverage in Phoenix, Mesa, Tucson, Buckeye, and Chandler. Search by ZIP code or city below to find the closest one.

Market Insights Snapshot

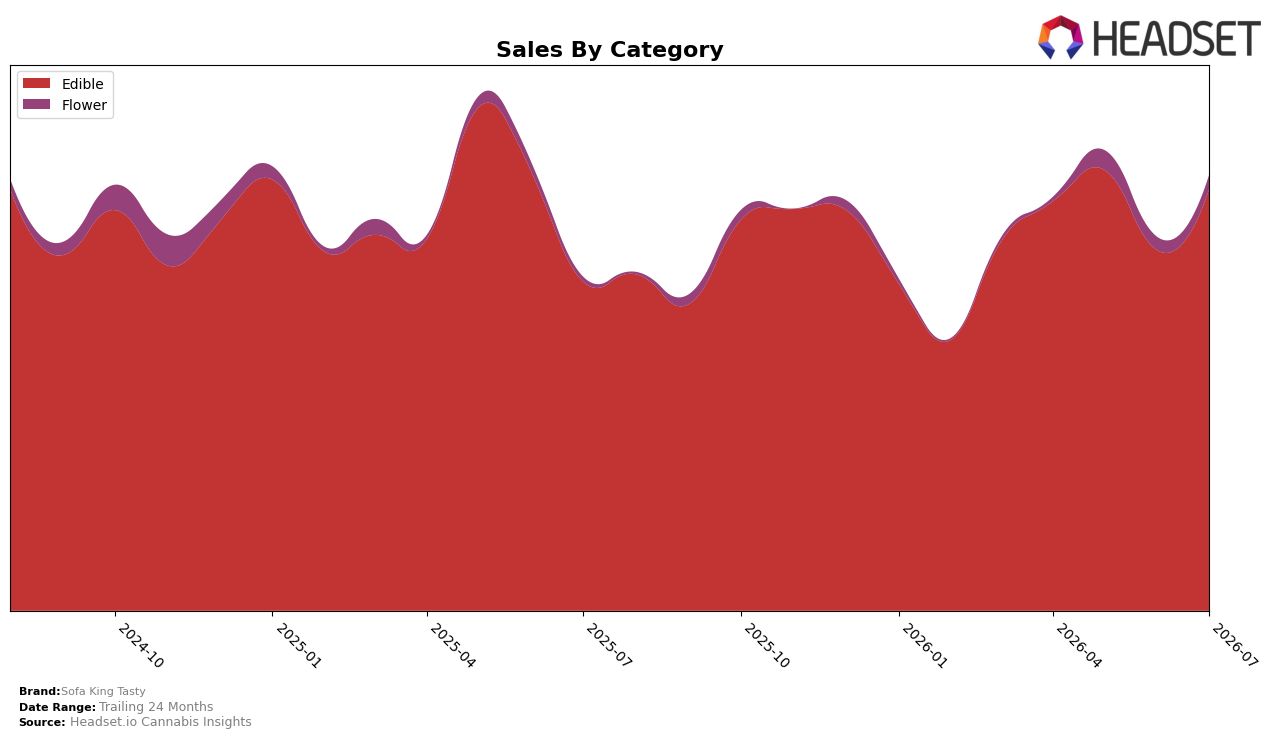

Sofa King Tasty’s July 2026 category mix remained concentrated in Edible at 93.51% share, with Flower at 6.49%, and both categories expanded simultaneously: Edible sales were up 26.68% year over year and 16.24% month over month, while Flower climbed 44.43% year over year and 3.52% month over month. Despite total brand sales rising 27.70% year over year, the average price fell 13.71%, indicating unit growth outpacing price declines; within that, Edible carried an average price of $8.09 and Flower averaged $7.21. In Arizona Edible, the brand ranked 13, and the combination of double‑digit Edible growth and a faster percentage gain in Flower signals a portfolio widening beneath a dominant Edible base, implying the brand is trading volume for share through price pressure while keeping category breadth intact.

The tilt toward Edible at 93.51% alongside a 44.43% year‑over‑year rise in Flower and a 16.24% month‑over‑month surge in Edible suggests a two‑speed positioning: defend scale in Edible while incrementally testing Flower to diversify risk. With the 13 rank in Arizona Edible and a 27.70% brand‑level year‑over‑year lift against a 13.71% price decline, the mix implies an emphasis on velocity and shelf throughput rather than price realization; the faster relative Flower growth and lower average price point indicate an entry‑tier or impulse stance designed to convert trial, which could support rank gains if maintained but may cap per‑unit margin unless trading up mechanisms are introduced.

Competitive Landscape

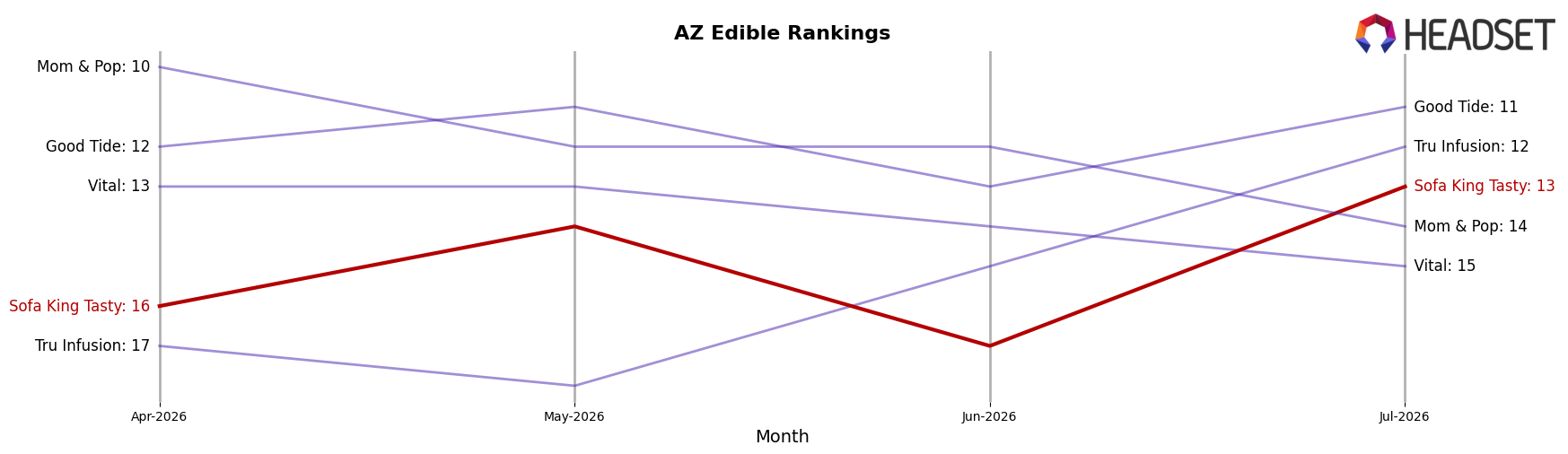

Sofa King Tasty sits at #13 in AZ Edible in July 2026, improving 1 rank position year over year from #14 while rising 3 spots from #16 over the last three months; that contrasts with Wyld holding #1 despite a -9.98% YoY sales decline and Baked Bros climbing from #4 to #3 on +27.68% YoY sales, indicating the middle tier is compressing as leaders either contract or surge. Sofa King Tasty’s current #13 remains below its #10 peak from July 2024, while OGEEZ stays fixed at #2 with +10.74% YoY growth and Gron / Grön slips from #3 to #4 with -1.76% YoY sales, implying Sofa King Tasty’s gradual rank lift reflects incremental share recapture but requires outpacing faster-rising peers to break back into the top 10.

Notable Products

Fruity Pebbles Bar (100mg) posted the largest month-over-month gain at 52.9% and climbed into rank 8, while Rainbow Crunch Gummies 10-Pack (100mg) fell 12.1% to rank 4, indicating a reshuffle within the edible lineup. Sativa Watermelon Gummies (100mg) advanced 27.7% to rank 2, narrowing the gap with Sativa Cherry Gummies (100mg) at rank 1 with 4.1% growth and a single-month revenue of $39,654. Eight of the top ten are Edible SKUs, and the only Flower item, Skunkee (1g), surged 43.3% into rank 7, but edible gains of 37.4% and 19.4% among mid-tier bars signal the gravity is still toward confections. The pattern implies Sofa King Tasty is consolidating around a candy-led portfolio where fast-rising novelty bars pull share even as flagship gummies maintain category leadership.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.