Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

In July 2026, BC OZ operated as a single-category brand with Flower at 100.0% of sales share, while Flower sales were down 32.16% year over year and 20.31% month over month; at the brand level, sales declined 32.24% year over year alongside a 1.03% year-over-year increase in average price. Within British Columbia Flower, BC OZ held rank 17, a position that, paired with a full reliance on a category experiencing double-digit month-over-month contraction, implies exposure to category cyclicality without portfolio offsets.

The mix staying at 100.0% Flower while average price rose 1.03% year over year and sales fell 32.24% year over year suggests BC OZ traded minimal pricing gains for volume losses, and the 20.31% month-over-month decline indicates price was not used to stabilize share in a weakening month. Holding rank 17 in British Columbia Flower during a 32.16% category-year-over-year decline and a 20.31% month-over-month drop signals the brand’s positioning is tied to Flower demand swings rather than cross-category customer capture, implying that portfolio breadth or targeted price tiers may be required to defend rank if category pressure persists.

Competitive Landscape

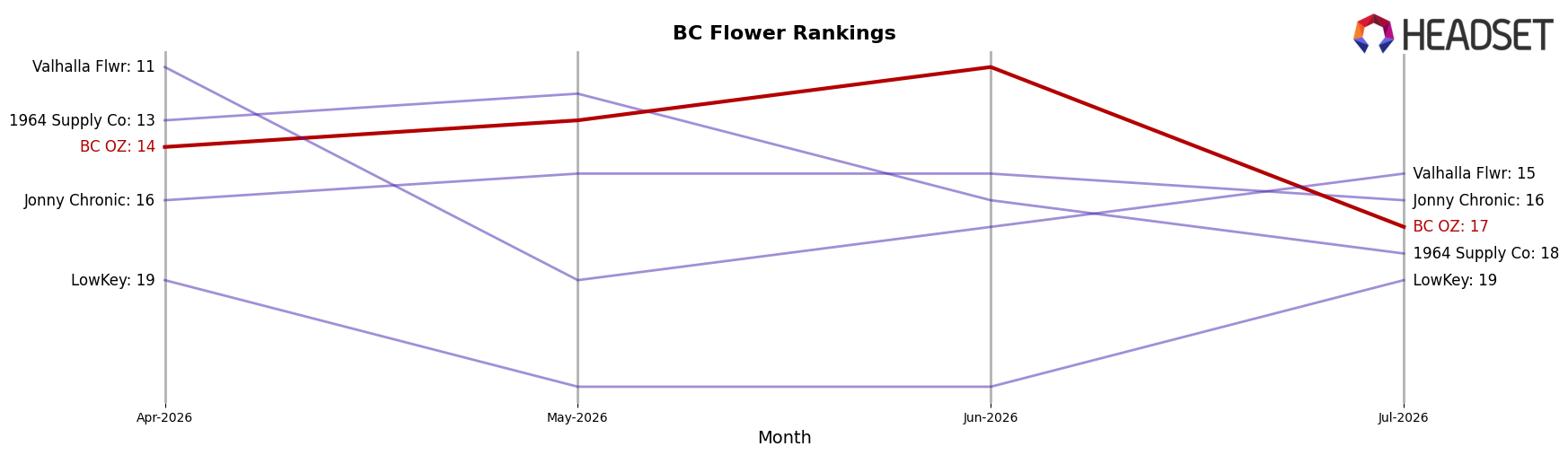

BC OZ sits at rank #17 in BC Flower in July 2026, down 4 positions year over year from #13, and 3 positions lower than April 2026 when it was #14; the drop contrasts with Good Supply rising from #6 to #2 while expanding sales by 42.9%, and diverges from Big Bag O' Buds moving from #2 to #1 with a 6.4% sales gain; compared with its peak at #1 in October 2025 and a current placement outside the top 15, the three-month slide of 3 ranks and a year-over-year decline of 4 ranks indicate BC OZ is losing relative share to faster-advancing incumbents, implying that without near-term product or pricing repositioning the brand’s trajectory points to further mid-tier displacement.

Notable Products

Jade Noir (28g) posted the standout move in July 2026 with +143% MoM, rising to rank 1, while Comfortably Numb (28g) collapsed −85% MoM to rank 9; the spread between a triple-digit gain at the top and a bottom-tier plunge implies a volatile reallocation of demand within the catalog. Lemon Heads (28g) slid −34% MoM to rank 2, and 9 lb Hammer (28g) fell −17% to rank 3, yet Silver Orchard (28g) climbed +59% MoM to rank 4, indicating that momentum clustered around select Flower SKUs even as adjacent peers retrenched. With all top-10 positions occupied by Flower and two SKUs experiencing >50% MoM swings, the mix points to a deliberate tilt toward fewer, scale-ready ounces that can win share quickly while underperformers are deprioritized.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.