Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

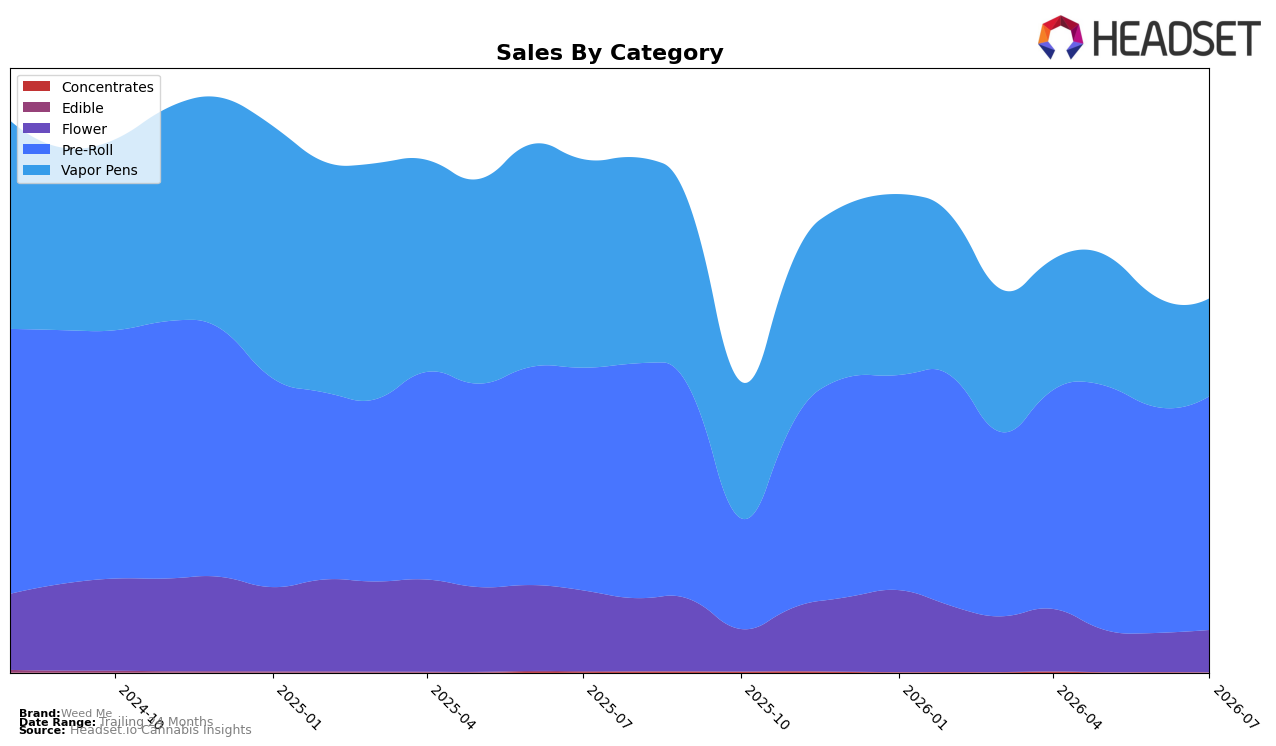

In July 2026, Weed Me’s mix concentrates in Pre-Roll at 62.57% share with Pre-Roll up 4.98% year over year and 3.64% month over month, while Vapor Pens at 26.15% share fell 53.12% YoY and 10.59% MoM. Flower holds 11.28% share with an 8.13% MoM lift despite a 47.75% YoY decline, and Edible is effectively exited at 0.00% share with a 99.25% YoY drop against a 2.36% MoM uptick. With average price down 24.11% YoY to $24.31 alongside Pre-Roll growth, the pattern implies Weed Me is leaning into lower-priced, higher-velocity Pre-Rolls to offset steep Vapor Pens and Flower contractions in British Columbia.

Holding rank 3 in Pre-Roll in British Columbia while Pre-Roll share rises to 62.57% and category sales expand 3.64% MoM suggests a defensible anchor position, but the 53.12% YoY decline in Vapor Pens and 47.75% YoY decline in Flower indicate risk of overexposure to one category. The combination of a 24.11% YoY price decrease and a 4.98% YoY gain in Pre-Roll points to a volume-led strategy that could preserve placement yet compress mix margins; the 8.13% MoM rebound in Flower offers a test bed for rebalancing without diluting the Pre-Roll-led rank 3 stance.

Competitive Landscape

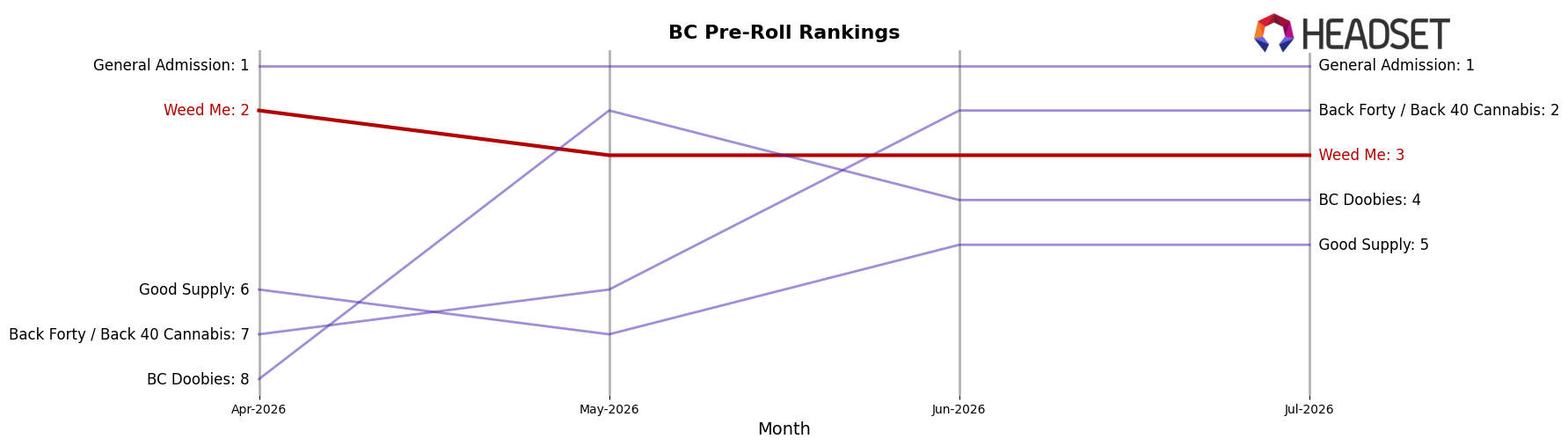

Weed Me is ranked #3 in BC Pre-Roll in July 2026, down 1 position year over year from #2, and off its April 2026 peak of #2 by 1 spot; the brand also slipped from #2 to #3 since April 2026 while the category leader General Admission held #1 despite a 22.34% YoY sales decline and Back Forty / Back 40 Cannabis surged from #17 to #2 with 215.25% YoY growth. Relative to BC Doobies advancing to #4 from #7 and Good Supply climbing to #5 from #8, Weed Me’s shift from #2 to #3 indicates share pressure concentrated at the top end rather than broad-based erosion, implying the trajectory points to a fight to defend a top-3 position against faster risers.

Notable Products

Black Mountain Side Pre-Roll 3-Pack (1.5g) posted a 95.6% month-over-month surge to rank 1, while King Size Sativa 420 Pre-Roll 20-Pack (8g) slid 12.9% to rank 4, flipping the leadership narrative in July 2026 and concentrating momentum in smaller pack sizes. Eight of the top ten SKUs are Pre-Rolls, with Blue Iguana Pre-Roll 3-Pack (1.5g) up 27.3% at rank 2 and Powdered Donuts Pre-Roll 3-Pack (1.5g) up 31.6% at rank 3, versus Vapor Pens where Max- Mango Blueberry Slush Liquid Diamond Cartridge (1g) fell 6.0% at rank 6 and Max - Seedless Grape Liquid Diamond Cartridge (1g) fell 6.4% at rank 10. Despite the $388,072 outcome for the 20-Pack, the contrasting -12.9% decline alongside multiple +27–32% gains among 3-Packs indicates share is rotating toward lower-unit-count formats. The pattern implies Weed Me is shifting demand toward frequent, lower-commitment purchases in Pre-Rolls while Vapor Pens lose relative traction month over month.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.