Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

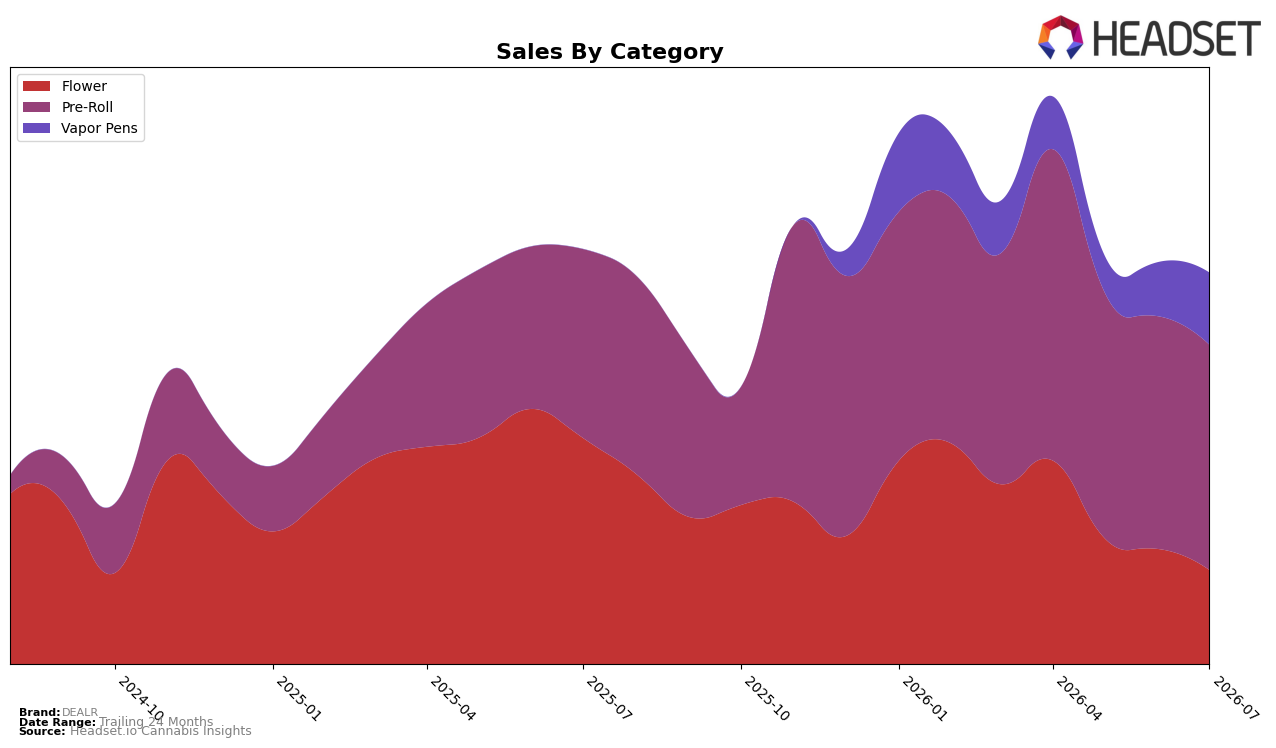

DEALR concentrated 57.55% of July 2026 sales in Pre-Roll with year-over-year growth of 19.23% and a month-over-month dip of 3.23%, while Flower fell to 24.03% share with a -58.42% year-over-year decline and a -18.31% month-over-month slide; Vapor Pens expanded to 18.42% share on a 33.67% month-over-month gain despite no year-over-year baseline. Average price dropped 21.23% year over year to $27.22 as Pre-Roll averaged $20.36 and Flower averaged $83.23, indicating mix-down effects tied to the 24-month sales expansion of 154.71% alongside a July 2026 year-over-year sales contraction of 5.72%. The pattern implies DEALR is pivoting toward lower-priced, velocity-oriented Pre-Roll and accelerating Vapor Pens, while retreat in Flower compresses premium price points and heightens reliance on repeat purchase categories.

With Pre-Roll now the anchor at rank 12 in British Columbia and a 57.55% mix, the -3.23% month-over-month dip suggests ceiling pressure at current shelf depth, whereas Vapor Pens’ 33.67% month-over-month rise indicates whitespace that can rebalance the -5.72% brand-level year-over-year decline. The -58.42% year-over-year and -18.31% month-over-month erosion in Flower, paired with a 21.23% year-over-year average price decline, signals a deliberate trade-down that boosts unit throughput but risks margin dilution; the implication is to lean into value-tier Pre-Roll and build Vapor Pens distribution while selectively pruning Flower to stabilize price architecture.

Competitive Landscape

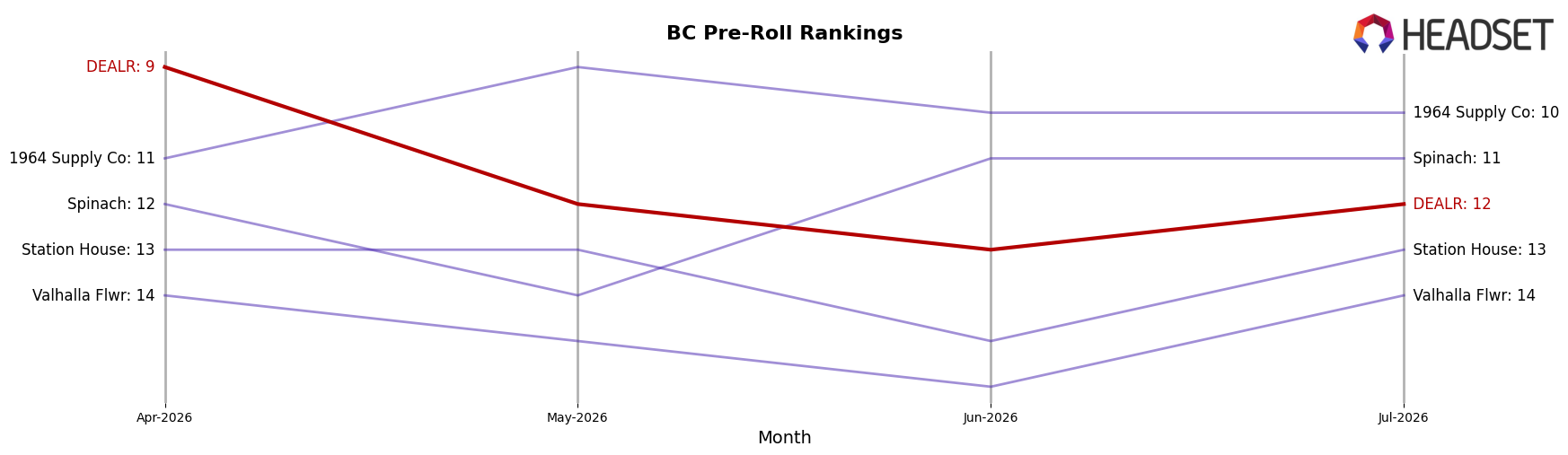

DEALR sits at rank #12 in BC Pre-Roll in July 2026, improving 9 positions year over year from #21 and slipping 3 positions since April 2026 when it peaked at #9; meanwhile, Back Forty / Back 40 Cannabis advanced from #17 to #2 alongside a 215.25% YoY sales change, and General Admission held #1 while posting a -22.34% YoY sales change. The combination of DEALR’s YoY rank gain of 9 spots and quarter-over-quarter decline of 3 spots, contrasted with Weed Me holding #3 despite a -6.83% YoY sales change and Good Supply rising to #5 with a 39.24% YoY sales change, implies a mid-pack position vulnerable to faster movers and dependent on recapturing its April 2026 peak momentum.

Notable Products

Love Potion #9 Pre-Roll 5-Pack (2.5g) posted the steepest move in July 2026 with a -39.3% month-over-month drop while sliding to rank 4, contrasting with Pink Bubblegum Infused Pre-Roll 3-Pack (1.5g) up 32.3% and holding rank 3. Category concentration remains high with seven of the top ten as Pre-Roll SKUs, led by Sweet Jesus Pre-Roll 5-Pack (2.5g) at rank 1 with +8.2% MoM and $172,504 in sales, while Vapor Pens split directionally with Cherry Bottles Diamonds Cured Resin Disposable (1g) down -11.5% at rank 9 and Bubble Burst Liquid Diamonds Cured Resin Disposable (1g) up +1.6% at rank 6. The mix indicates DEALR is skewing toward infused and value multi-pack Pre-Rolls for volume while Vapor Pens act as complementary but more volatile slots, implying near-term merchandising should prioritize Pre-Roll depth over breadth.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.