Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

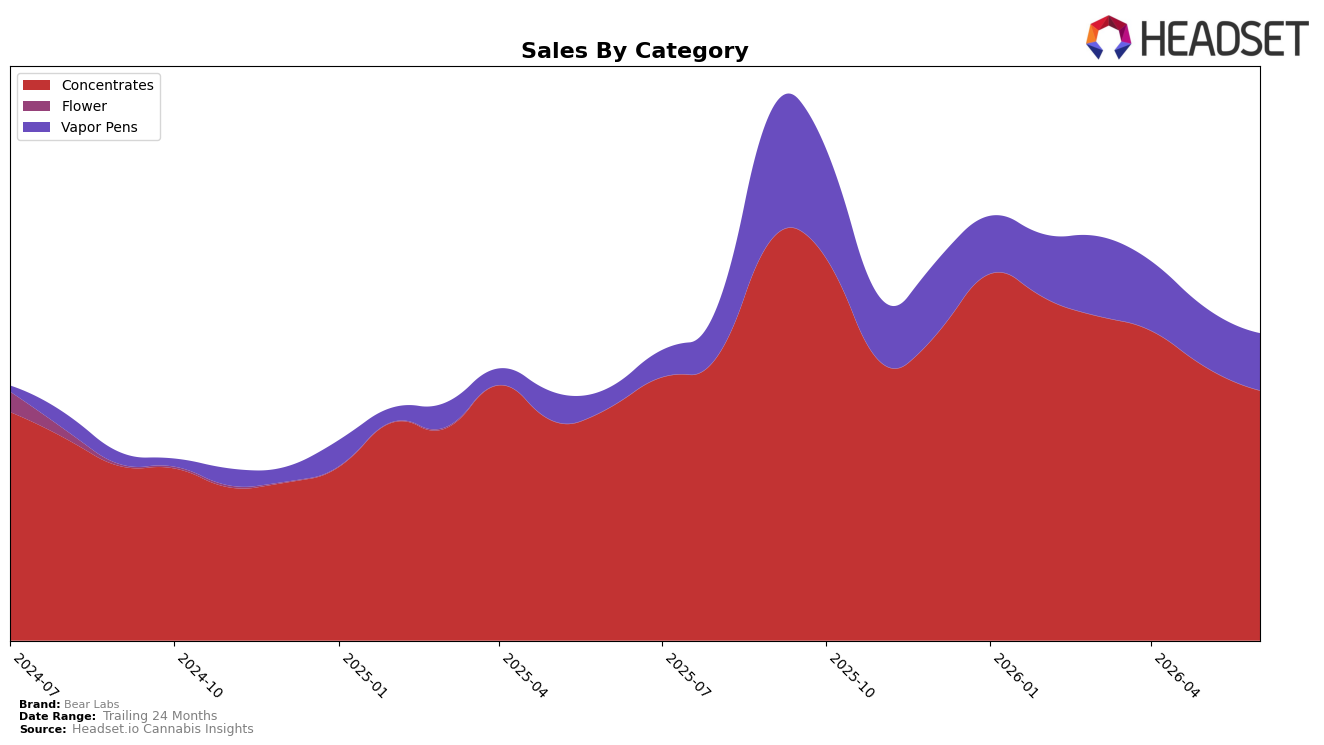

Bear Labs concentrated its June 2026 mix in Concentrates at 81.44% share (rank 9 in Concentrates in California) with year-over-year growth of 7.74% but a month-over-month decline of 8.77%, while Vapor Pens expanded to 18.56% share with a 185.51% year-over-year surge but a 3.49% month-over-month dip. The brand’s overall sales rose 21.82% year over year as average price fell 13.10% to $23.45, indicating that unit velocity rather than pricing drove the uplift; this combination implies the portfolio is leaning into lower-priced Concentrates to anchor volume while Vapor Pens contribute incremental mix despite short-term monthly softness.

The shift toward an 18.56% Vapor Pens share alongside an 81.44% Concentrates core suggests Bear Labs is using Vapor Pens as a secondary entry point without displacing its Concentrates base, given the 7.74% Concentrates YoY growth versus the 185.51% Vapor Pens YoY expansion. Holding rank 9 in Concentrates in California while posting month-over-month declines in both categories (-8.77% and -3.49%) indicates a pullback tied more to monthly demand or promo cadence than to structural share loss, implying the brand’s positioning remains anchored in Concentrates with selective Vapor Pen scaling that can buffer seasonality if price architecture stays disciplined.

Competitive Landscape

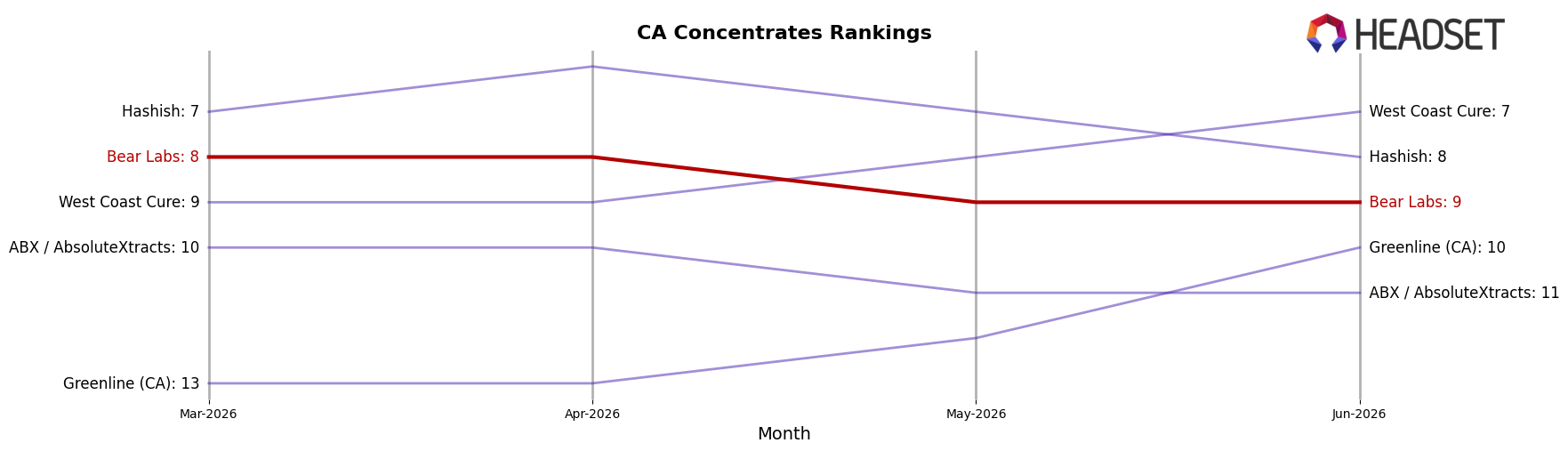

Bear Labs is ranked #9 in CA Concentrates in June 2026, slipping 1 position year over year from #8 while holding flat versus March 2026 at #8, indicating a modest downward drift against a steady near-term baseline. In contrast, 710 Labs climbed from #4 to #3 on 24.7% YoY sales growth, while Punch Extracts / Punch Edibles fell from #3 to #4 with a 29.1% YoY sales decline, underscoring that movement around the top five is active even as Raw Garden held #1 with 7.0% YoY growth. With its peak at #5 in October 2025 and a current position four spots lower, the trajectory implies Bear Labs is ceding relative share to faster risers and must reverse rank slippage to reenter the top-five tier.

Notable Products

Black Cherry Dream Budder (1g) posted the steepest movement in June 2026 with a -33.7% month-over-month change while holding rank 3, contrasting with Chem Diesel BHO Budder (1g) at rank 2 growing +17.7% month over month. White Runtz BHO Badder (1g) led the board at rank 1 with no reported month-over-month figure, and Hash Burger Live Rosin (1g) dropped -22.2% at rank 7. With eight of the top ten slots in Concentrates and only one Vapor Pens SKU at rank 8, the mix indicates Bear Labs is consolidating around hydrocarbon and rosin formats rather than expanding inhalable variety.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.