Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

710 Labs is stocked at 855 licensed dispensaries across California, Michigan, and 5 other states, 451 of them in California, with the deepest coverage in Los Angeles, San Francisco, San Diego, San Jose, and Santa Ana. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

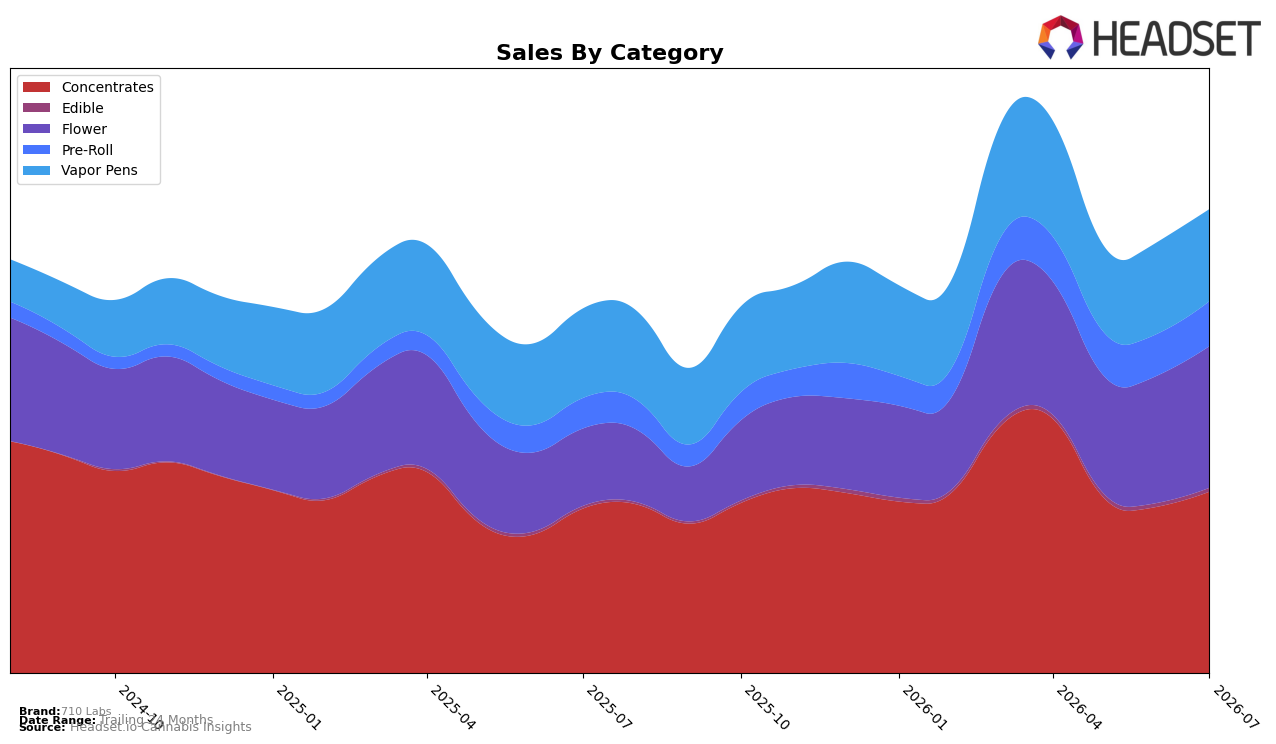

In July 2026, 710 Labs split sales across Concentrates at 38.92% share and Flower at 30.41% share, with Vapor Pens at 19.84% and Pre-Roll at 9.80%; this mix shifted as Flower surged 82.01% year over year while Concentrates rose 10.13%, and month over month Flower advanced 11.04% versus 8.89% in Concentrates. Vapor Pens held nearly flat with 2.73% YoY and 0.27% MoM, while Pre-Roll climbed 46.08% YoY and 7.44% MoM; Edible added 34.01% YoY on 1.09% MoM from a 1.03% share. With average price down 2.80% YoY to $32.65 and Concentrates carrying a $49.23 average versus Flower at $26.20, the pattern implies 710 Labs is trading into higher-volume, lower-price Flower and Pre-Roll without abandoning its Concentrates anchor, tilting revenue mix toward faster-growing inhalables while protecting premium margins in Concentrates.

These shifts imply a dual-track positioning where 710 Labs maintains rank-led credibility in Concentrates (ranked 2 in Concentrates in Colorado) while expanding reach via scaled Flower and Pre-Roll, evidenced by Flower’s 82.01% YoY and 11.04% MoM outpacing Vapor Pens’ 2.73% YoY and 0.27% MoM. The 8.89% MoM in Concentrates alongside a 7.44% MoM in Pre-Roll suggests basket-building around extracts plus ready-to-consume formats, and the 2.80% YoY price decline paired with a 19.84% share in Vapor Pens indicates price-sensitive segments are being addressed without heavy reliance on cartridges. The implication is portfolio smoothing: Concentrates sustains premium identity and rank while Flower and Pre-Roll absorb demand elasticities, positioning 710 Labs to capture incremental volume growth without overexposure to any single category’s slower YoY trajectory.

Competitive Landscape

710 Labs sits at rank #3 in CA Concentrates in July 2026, improving 1 position from #4 year over year while slipping 1 spot from #2 in April 2026 to #3 in July 2026; the brand also peaked at #2 in May 2026, indicating short-term volatility around a generally upward YoY trend. Competitively, Raw Garden holds #1 with no YoY rank change and posted a 14.2% sales lift, and STIIIZY remains #2 with a 1.4% sales increase, while Punch Extracts / Punch Edibles slid from #3 to #4 alongside a 21.1% sales decline; this pattern implies 710 Labs is consolidating a top-three position but must regain momentum from its May 2026 peak to close the gap on the stable #1–#2 tier.

Notable Products

With no month-over-month swings above +50% or below -10%, the steepest move is Donny Burger Pre-Roll (1g) slipping 5.8% to rank 10 while Terp Quest RSO Syringe (1g) gained 6.3% to rank 5, establishing a split where concentrates edged up as a value pre-roll softened. Cherry Ludens (3.5g) leads at rank 1 while Britney's Frozen Lemons #5 (3.5g) sits at rank 8, and six of the top ten are Flower SKUs, indicating a portfolio still concentrated in Flower despite a higher-ranked concentrate. This mix suggests 710 Labs is leaning on flagship Flower to anchor share while selectively scaling a single concentrate SKU, a positioning that tilts toward depth in Flower with tactical experimentation in non-Flower formats.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.