Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

CannaBiotix (CBX) is stocked at 662 licensed dispensaries across California, with the deepest coverage in Los Angeles, San Diego, San Francisco, Santa Ana, and Sacramento. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

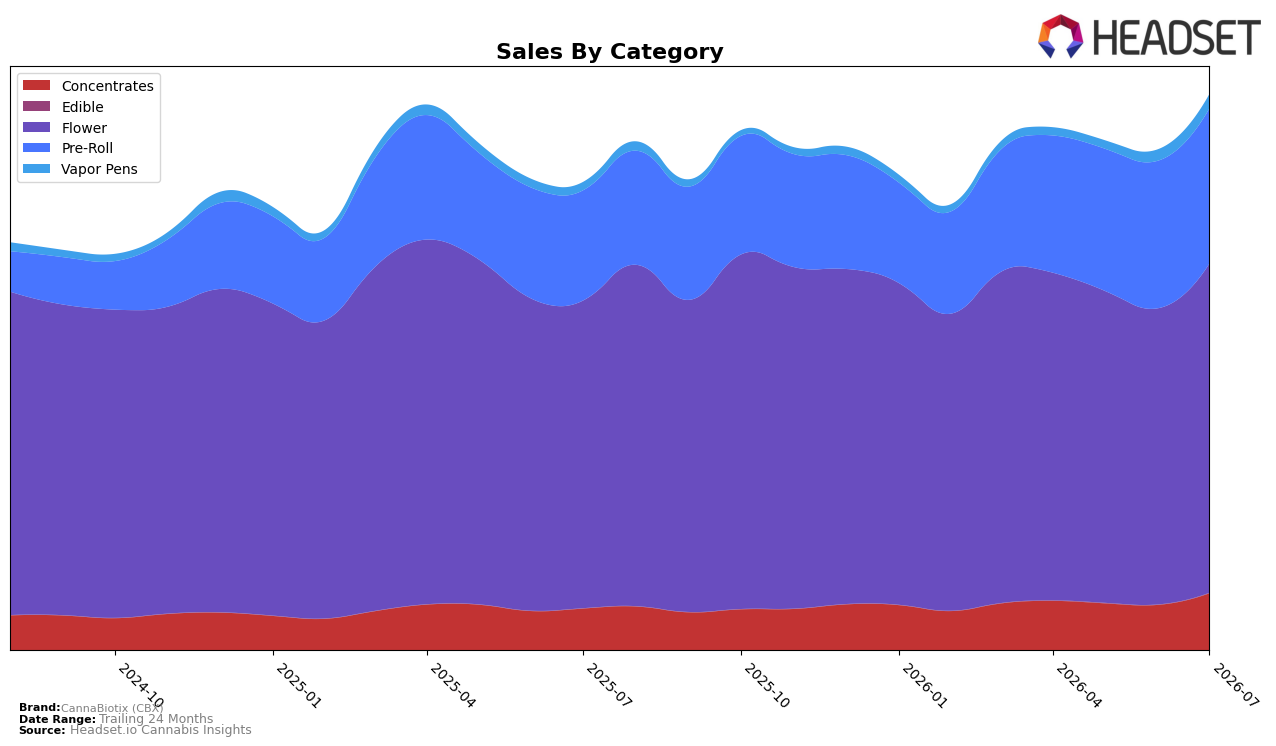

CannaBiotix (CBX) concentrated 59.31% of July 2026 sales in Flower with month-over-month growth of 11.17% and year-over-year growth of 7.01%, while Pre-Roll held 27.91% share with 5.12% MoM and 40.83% YoY expansion. Smaller lines accelerated: Concentrates captured 10.20% share with 25.77% MoM and 36.98% YoY, and Vapor Pens, at 2.54% share, climbed 26.75% MoM and 74.98% YoY; Edible remained marginal at 0.03% share but spiked 149.86% MoM. The mix shifted toward faster-growing inhalables even as the brand’s average price fell 13.59% YoY and total brand sales rose 18.84% YoY, implying CBX is trading volume for share across multiple form factors rather than relying solely on its Flower base.

With Flower still the anchor and ranked 2 in California while Pre-Roll and Concentrates post double-digit MoM gains (5.12% and 25.77%, respectively), CBX’s positioning tilts toward a multi-format portfolio that leverages price elasticity to widen reach. The rapid YoY expansion in Vapor Pens at 74.98% alongside a 27.91% Pre-Roll share suggests cross-category customer capture, and the 18.84% YoY brand growth alongside a 13.59% YoY price reduction indicates a deliberate elasticity play; this combination implies CBX is prioritizing penetration and basket breadth over premium price maintenance to defend rank and diversify beyond Flower.

Competitive Landscape

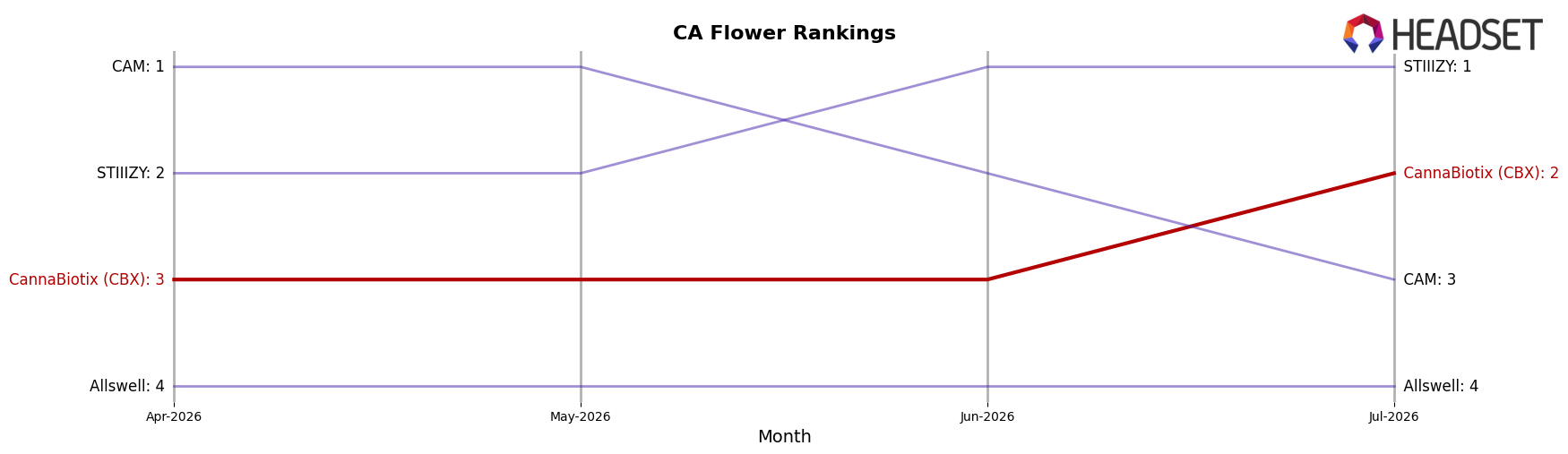

CannaBiotix (CBX) sits at rank #2 in California Flower in July 2026, down 1 position year over year from #1, after improving 1 spot since April 2026 when it was #3; the brand also peaked at #1 in January 2026, indicating a -1 rank change from peak to current. In contrast, STIIIZY holds #1 after rising from #2 year over year while posting a 59.7% sales increase, and CAM is #3, up from #4 with 52.2% year-over-year sales growth, whereas Claybourne Co. fell from #3 to #5 alongside a -1.4% sales decline. The pattern implies CannaBiotix (CBX) is maintaining top-tier share but ceding momentum to faster-rising leaders, signaling a need to arrest slippage from a January 2026 peak to preserve #2 and contest #1.

Notable Products

CannaBiotix (CBX) Super Mango Haze Pre-Roll (0.75g) posted the steepest decline among top SKUs in July 2026 at -17.9% MoM, dropping behind White Walker OG Pre-Roll (0.75g) which rose 17.4% MoM to rank 3 while Super Mango Haze held rank 2. Cereal Milk (3.5g) remained rank 1 with a -1.5% MoM dip, and the single Cereal Milk Pre-Roll (0.75g) fell -26.2% MoM at rank 7 even as the Cereal Milk Pre-Roll 4-Pack (2g) gained 7.9% MoM at rank 4, implying format shift within the same strain family. Eight of the top ten are Pre-Rolls, including double-digit MoM gains for L'Orange Pre-Roll 4-Pack (2g) at +16.2% and GM-uhOh Pre-Roll 4-Pack (2g) at +18.8%, while Casino Kush Pre-Roll (0.75g) slid -26.4% at rank 10, indicating consolidation toward multi-pack and select SKUs. The pattern suggests CannaBiotix (CBX) is tilting assortment and demand toward Pre-Roll multi-packs and a few anchor strains while single-stick variants fragment, guiding pricing and promo toward bundles over individual units.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.