Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Bhang is stocked at 76 licensed dispensaries across New Mexico and California, 75 of them in New Mexico, with the deepest coverage in Albuquerque, Santa Fe, Hobbs, Rio Rancho, and Farmington. Search by ZIP code or city below to find the closest one.

Market Insights Snapshot

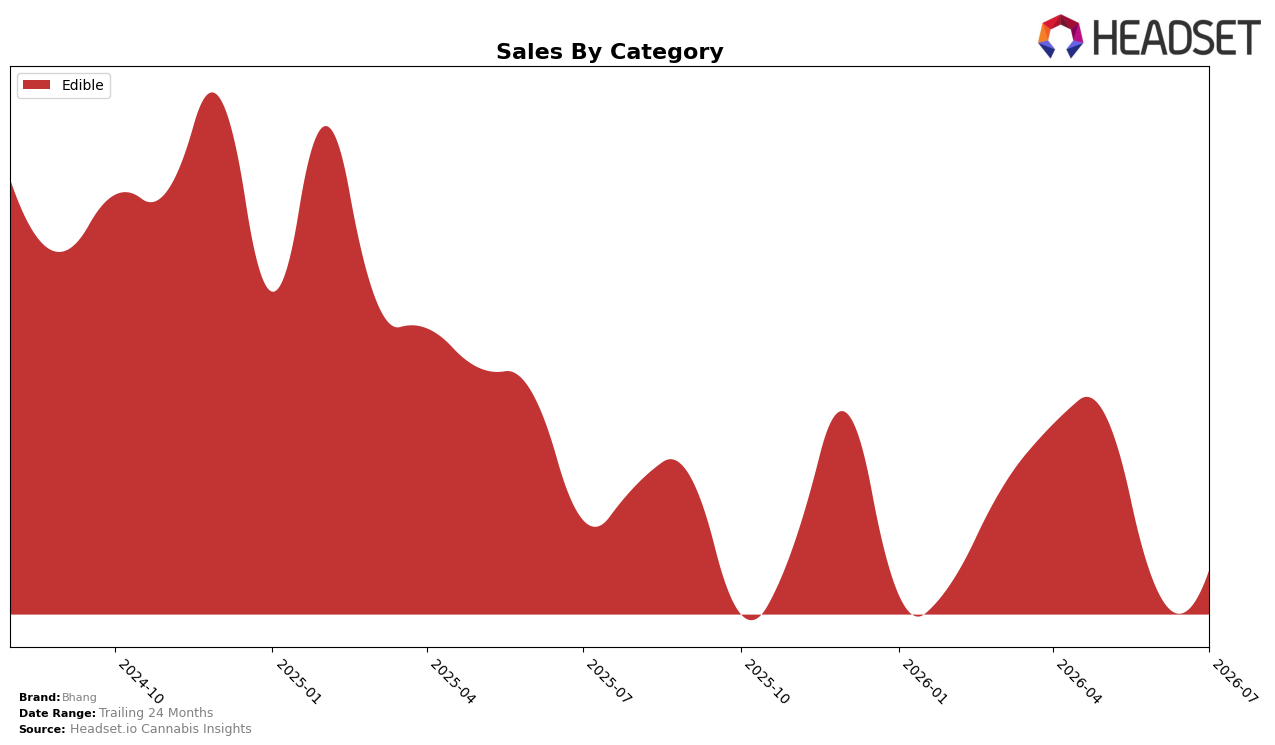

In July 2026, Bhang operated as a single-category brand with Edible accounting for 100.0% of sales, while category sales moved -5.19% year over year and +2.30% month over month. Average price sat at $4.63 with a -0.47% YoY shift, indicating modest price compression alongside a slight MoM volume or mix lift. With Edible concentrated in ON and a category rank of 14 in Edible within British Columbia, the pattern implies Bhang is trading short-term MoM momentum for longer-term YoY softness within a fully concentrated Edible strategy.

The 100.0% Edible mix, coupled with a -5.19% YoY decline against a +2.30% MoM uptick, suggests Bhang’s positioning hinges on rapid execution within Edible rather than portfolio diversification. The -0.47% YoY price change at a $4.63 average implies reliance on entry-priced or value-leaning SKUs to defend share rank 14 in British Columbia while leaning on ON as the volume anchor; this pattern implies Bhang’s path to regain YoY growth is through mix optimization and selective premiumization inside Edible rather than cross-category expansion.

Competitive Landscape

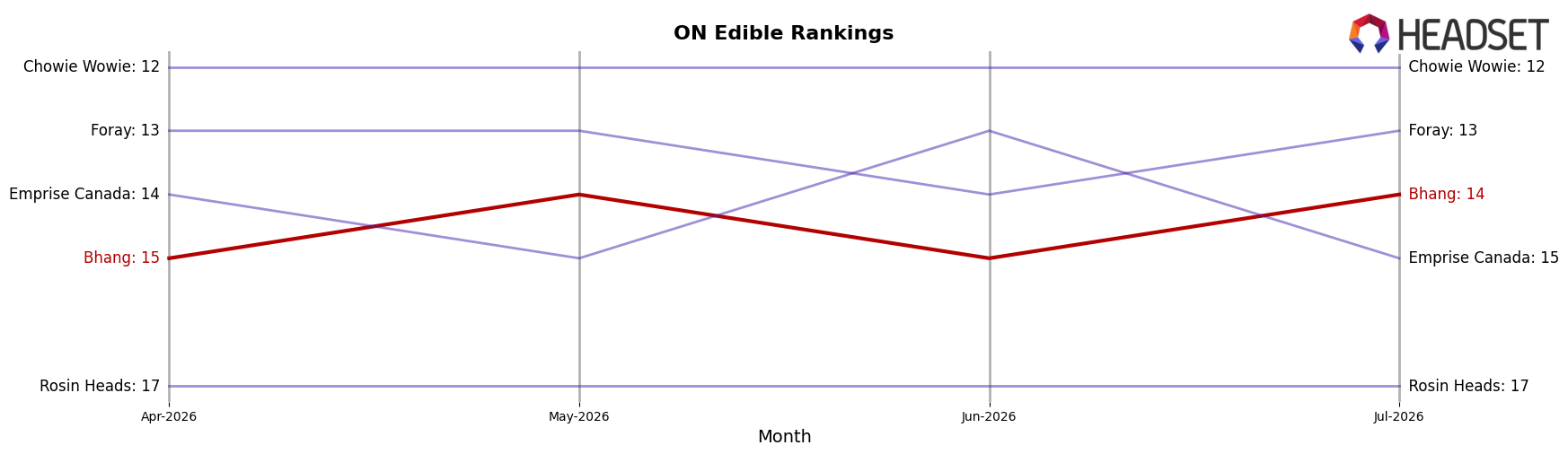

Bhang ranks #14 in ON Edible in July 2026, down 4 positions year over year from #10, and it slipped 1 rank versus April 2026 when it was #15 improving briefly before settling back, while its historical peak was #10 in July 2025. In contrast, Spinach held #1 with a 11.26% year-over-year sales gain and Wyld advanced from #4 to #3 alongside a 13.69% sales increase, whereas Fly North vaulted from #15 to #5 on 611.52% growth, indicating that Bhang’s rank erosion amid double-digit competitor gains points to a share redistribution rather than a category contraction.

Notable Products

CBD/THC 1:1 Mochaccino Milk Chocolate (10mg CBD, 10mg THC) posted the steepest decline in July 2026 at -84.8% MoM, dropping into rank 10, while Ice Milk Chocolate Bar (10mg) fell -59.7% MoM to rank 8. Offsetting that weakness at the top, THC Milk Chocolate Bar 4-Pack (10mg) surged +271.3% MoM to rank 2 and THC Dark Chocolate Bar 4-Pack (10mg) rose +78.6% MoM to rank 1. The pattern implies a pivot toward multipack THC chocolate bars as growth engines while niche flavors retreat.

CBD/THC 1:1 Caramel Dark Chocolate Bar (10mg CBD, 10mg THC) advanced +409.9% MoM to rank 3 even as the single-serve THC Milk Chocolate (10mg) slipped -9.5% MoM to rank 5. Four of the top ten are multipacks or 1:1 functional variants, and Cookies and Cream White Chocolate Bar (10mg) added +1,036.9% MoM at rank 4 with under $31,000 in sales, indicating demand is concentrating in formats that either bundle servings or pair THC with CBD.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.