Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

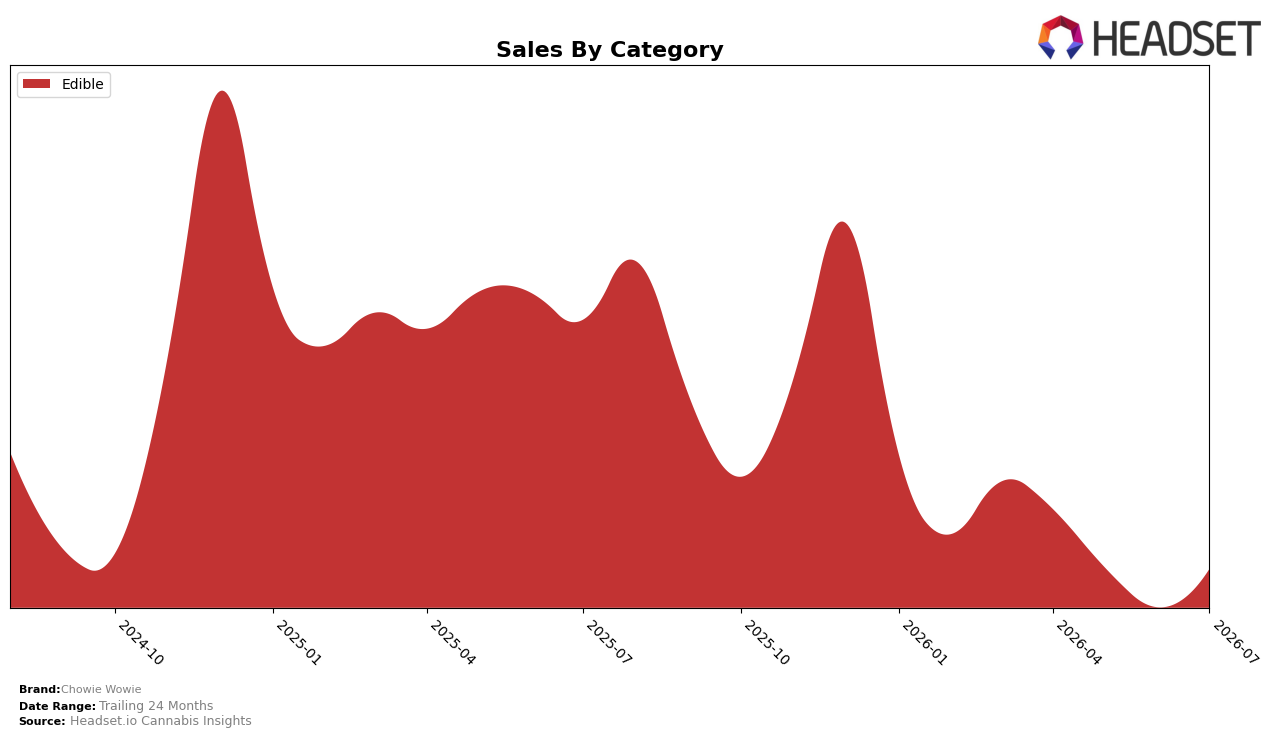

In July 2026, Chowie Wowie’s mix was concentrated entirely in Edible at 100.0% share, with Edible sales up 4.39% month over month but down 21.45% year over year, while average price rose 27.81% year over year and anchored a single-category strategy. Within this single-category footprint, the brand held an Edible rank of 8 in Saskatchewan and posted its top-state volume in ON, implying that mix breadth did not offset the July 2026 year-over-year sales contraction despite a positive monthly uptick. The pattern implies that a price-led, single-category stance is driving short-term MoM lift but not reversing the YoY decline, and that rank position 8 limits upside without incremental mix or subsegment expansion.

The July 2026 tilt toward Edible at 100.0% share, combined with a 27.81% YoY price increase and a 21.45% YoY sales decline, suggests price elasticity is compressing unit volumes even as MoM sales rose 4.39%, and that the state-level footprint anchored by ON needs deeper penetration to improve the rank of 8 in Saskatchewan. Because the category dependence magnifies exposure to Edible-specific demand cycles while raising average price, the implication is that positioning should pivot toward value cues or pack/format optimization within Edible to regain share and climb from rank 8, rather than rely on further price increases that risk widening the 21.45% YoY gap.

Competitive Landscape

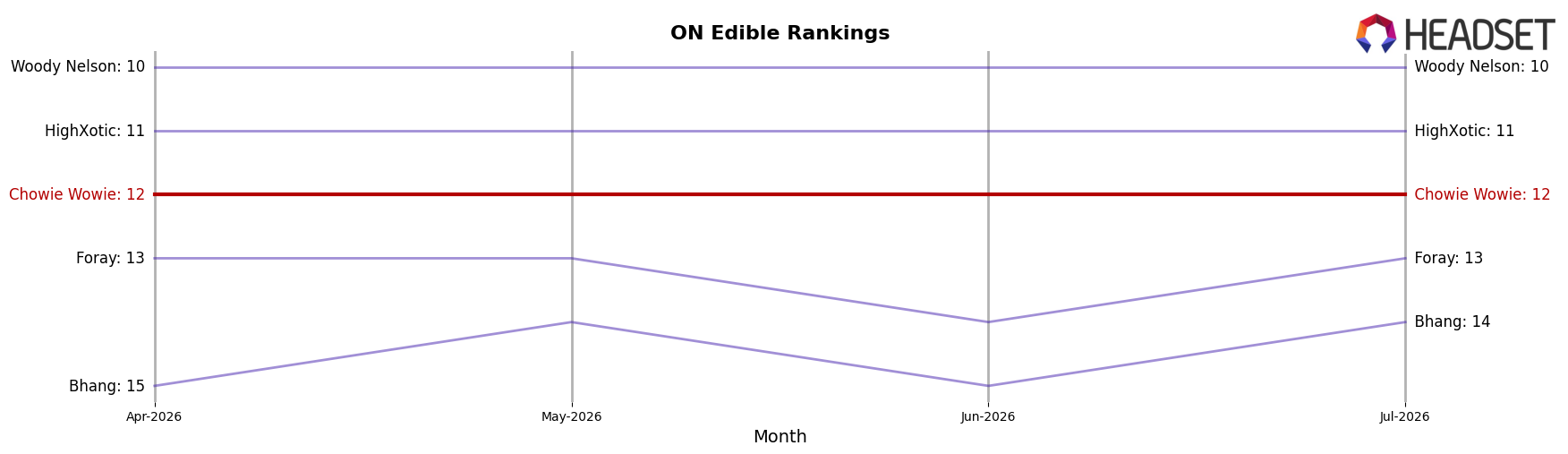

Chowie Wowie sits at rank #12 in ON Edible in July 2026, down 3 positions year over year from #9, while holding flat versus April 2026 at #12, indicating a stall beneath its prior peak of #8 from June 2025; in contrast, Wyld improved its placement from #4 to #3 alongside a 13.7% year-over-year sales increase, and Fly North surged from #15 to #5 with a 611.5% year-over-year lift, signaling that momentum is concentrating among climbers ahead of the middle tier. With category leaders steady as Spinach holding #1 year over year and Gron / Grön maintaining #2 while posting 6.5% sales growth, the combination of a 3-spot YoY slippage to #12 and zero quarter-to-quarter rank improvement implies Chowie Wowie is being outpaced by faster-advancing rivals and must change trajectory to avoid further share erosion.

Notable Products

CBD/THC 1:1 Solid Milk Chocolate Bar 2-Pack (10mg CBD, 10mg THC) dropped 84.7% month over month yet held rank 1, while THC Solid Milk Chocolate Bar (10mg) slid 10.0% and sits at rank 3. In contrast, CBD/THC 1:1 Peanut Butter Balanced Milk Chocolate (10mg CBD, 10mg THC) rose 12.7% at rank 2, and CBD/THC 1:1 Peanut Butter Balanced Chocolate 4-Pack (40mg CBD, 40mg THC) climbed 44.0% at rank 10 on a $27,760 base. With all top-10 SKUs in Edible and multiple 1:1 chocolate formats posting gains of 37.1% to 44.0% alongside the steep 84.7% fall in a leading 2-Pack, the mix signals a pivot from single-serve dominance toward diversified 1:1 chocolate multipacks anchoring future volume.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.