Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

Olli is entirely concentrated in Edible, with a 100.0% category mix in July 2026 and a rank of 3 in Edible within Alberta. Within this single-category footprint, year-over-year sales grew 109.1% while month-over-month sales rose 9.7%, and average price climbed 118.2% YoY to $8.75. The combination of 100.0% category share and a top-state anchor in ON implies that Olli is doubling down on Edible rather than hedging with adjacent formats, signaling a specialization strategy rather than portfolio diversification.

These shifts suggest Olli is monetizing demand elasticity in Edible: a 118.2% YoY average price increase alongside 109.1% YoY sales growth indicates mix trading up or successful premiumization, while a 9.7% MoM lift paired with a rank of 3 in Alberta points to ongoing velocity at higher price points. The 100.0% category concentration, coupled with triple-digit 24-month brand expansion of 669.8%, implies that continued gains will depend on sustaining Edible innovation and distribution depth rather than cross-category expansion.

Competitive Landscape

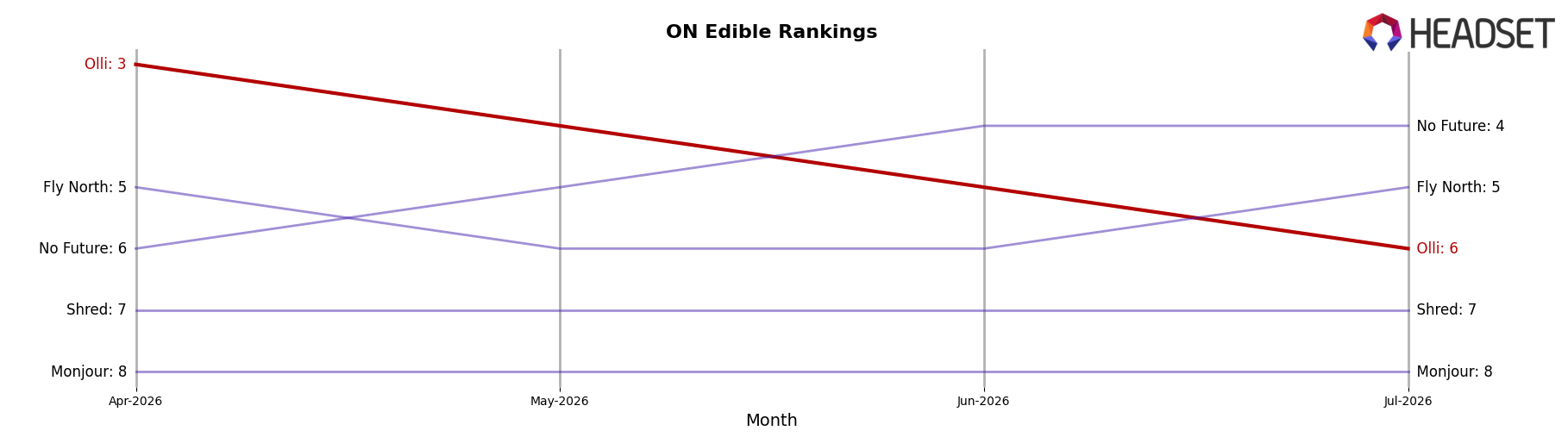

Olli ranks #6 in ON Edible in July 2026, a 1-place improvement from #7 year over year but a 3-place slide from #3 in April 2026; this contrasts with Wyld climbing from #4 to #3 alongside 13.7% YoY sales growth and Fly North jumping from #15 to #5 with 611.5% YoY growth, while category leader Spinach held #1 with 11.3% YoY growth. The gap is directional: Olli’s YoY rank gain of 1 contrasts with No Future moving from #5 to #4 on 58.3% YoY growth, and Olli’s drop from #3 in April 2026 to #6 in July 2026 signals share pressure from faster-rising competitors; the pattern implies mid-year rank erosion after a spring peak will continue unless Olli counters the accelerating momentum of peers now consolidating positions above it.

Notable Products

StikiStix - Sour Mango Haze Chews 10-Pack (100mg) posted the sharpest movement with a 44.1% month-over-month gain while sitting at rank 6, whereas Stikistix - CBG/THC 3:1 Razzy Pink Lemonade Soft Chew 4-Pack (30mg CBG, 10mg THC) rose 24.5% to hold rank 1. The lack of any top-10 declines over -10% alongside a flat -0.16% for CBD/CBG/CBN/THC 1:1:1:1 Fizzy Peach Lemonade Soft Chew (10mg CBG, 10mg CBN, 10mg THC, 10mg CBD) at rank 3 suggests upside is concentrated in mid-pack momentum rather than driven by a broad surge. With eight of the top ten being multi-count Chews or Gummies in the Edible category and only one mentionable raw dollar anchor at $282,276 for Stikistix - Very Berry Chews 15-Pack (150mg) at rank 4 against a 8.3% lift, the mix tilts toward scalable edible formats where incremental velocity can move share faster than price. The pattern implies Olli is leaning into flavor-led Chew variants that can climb ranks on moderate lifts, using a few breakout SKUs to pull the portfolio while flagship items stabilize mix and margin.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.