Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

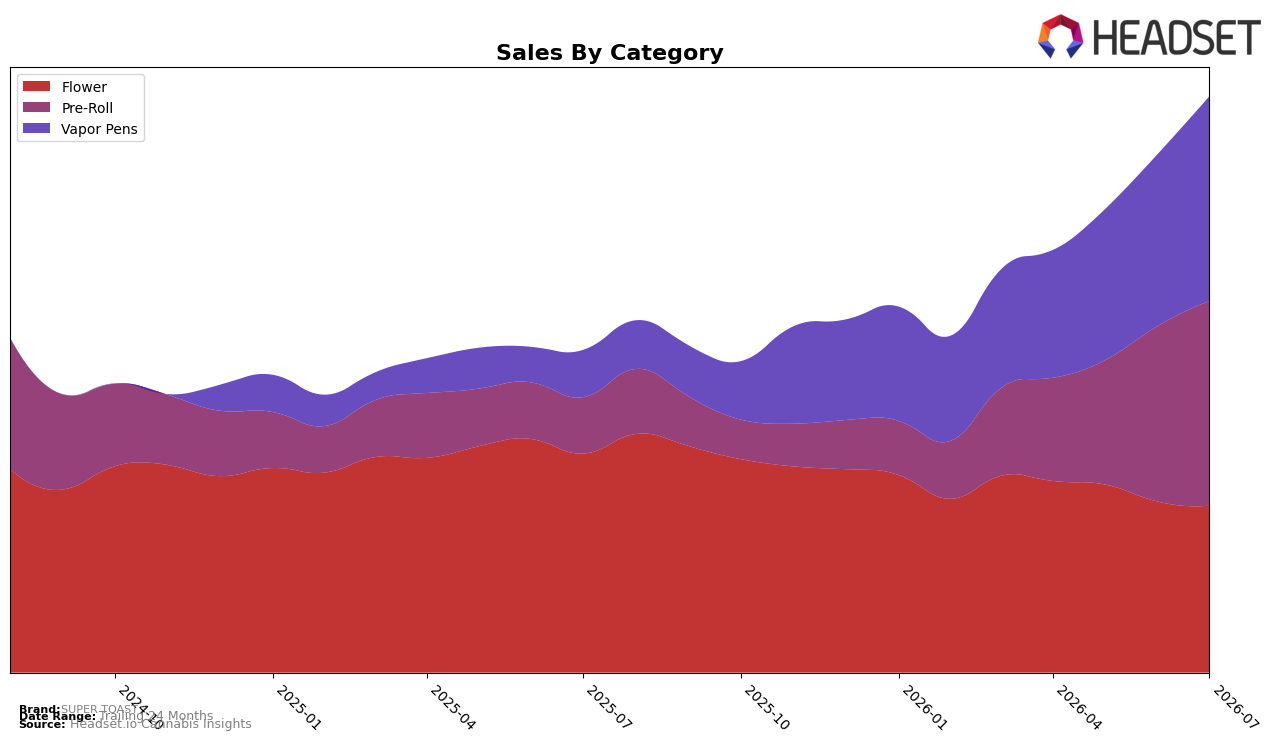

In July 2026, SUPER TOAST split its mix nearly evenly between Vapor Pens at 35.57% share and Pre-Roll at 35.48% share, with Flower down to 28.95% share. Vapor Pens grew 335.28% year over year and 19.08% month over month, while Pre-Roll rose 263.50% YoY and 16.40% MoM; in contrast, Flower declined 23.83% YoY and 2.39% MoM. With overall brand sales up 78.76% YoY and average price up 0.42% YoY to $23.66, the outsized growth in Vapor Pens and Pre-Roll versus contraction in Flower implies a structural pivot toward inhalables with faster velocity, concentrating demand away from legacy Flower.

These shifts reposition SUPER TOAST toward higher-growth inhalable formats, as evidenced by Vapor Pens and Pre-Roll jointly accounting for 71.05% share alongside double-digit MoM gains of 19.08% and 16.40%, respectively, while Flower softness of -23.83% YoY and a -2.39% MoM slide indicates reduced reliance on bulk Flower price elasticity. Holding the number 9 rank in Flower in Ontario against a shrinking Flower contribution suggests the brand is trading rank stability for mix-led growth, meaning near-term momentum is more sensitive to sustained pen and pre-roll velocities than to Flower positioning.

Competitive Landscape

SUPER TOAST ranks #9 in ON Flower for July 2026, unchanged year over year at #9 but down from #8 three months ago, while its peak at #6 in June 2025 marks a three-position slide from that high; in contrast, Shred moved from #2 to #1 with a 17.2% YoY sales increase and Spinach improved from #4 to #2 alongside 31.1% YoY growth, whereas Back Forty / Back 40 Cannabis fell from #1 to #4 with a 5.4% YoY decline and The Original Fraser Valley Weed Co. rose from #6 to #5 with essentially flat (+0.1%) sales, implying SUPER TOAST’s static #9 and drift from its June 2025 peak signal share leakage to faster-advancing leaders rather than a short-term fluctuation.

Notable Products

SUPER TOAST’s Animal Mintz Slims Pre-Roll 10-Pack (4g) posted the steepest shift in July 2026 with a -40.8% month-over-month drop at rank 10, while Liquid Demons - Mix Pack Infused Pre-Roll 5-Pack (2.5g) climbed 41.8% to rank 3. Hoagies Pre-Roll 2-Pack (2g) also advanced 23.6% to hold rank 1, and Passionfruit Salute Liquid Diamond Cartridge (1g) slipped -8.6% at rank 8. With three Pre-Roll SKUs in the top ten anchoring ranks 1, 3, and 10, the mix points to a strategy anchored in Pre-Rolls where flagship formats gain share even as legacy bundles retreat.

Watermelon Felon Liquid Diamond Cartridge (1g) in Vapor Pens grew 5.1% at rank 2, whereas Mango Ice Liquid Diamonds Cartridge (1g) entered at rank 9 with $326,515 and no prior month comparator. Flower held steady with Sgt. Pineapple Milled (7g) up 2.8% at rank 4 and Pop n' Pour Blue Raspberry Milled (3.5g) down -4.0% at rank 7. The dispersion—modest Vapor Pens growth, mixed Flower shifts, and divergent Pre-Roll trajectories—implies SUPER TOAST is consolidating around a two-pillar portfolio where Pre-Rolls drive velocity and select Vapor Pens maintain premium placement.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.