Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Big Pete's Treats is stocked at 600 licensed dispensaries across California, Missouri, and 5 other states, 407 of them in California, with the deepest coverage in Los Angeles, San Diego, Sacramento, San Francisco, and San Jose. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

In July 2026, Big Pete's Treats operated entirely within Edible, with Edible holding 100.0% category share and a month-over-month change of -5.49% against a year-over-year increase of 15.03%. Average price in Edible declined 4.97% year over year to $13.34 while total brand sales grew 14.88% year over year, indicating unit expansion offsetting price compression. Within California Edible, the brand held rank 17, and the 24-month sales lift of 35.29% paired with a July 2026 month-over-month dip of -5.49% suggests a maturing, price-sensitive base that scales on volume when promotions deepen. The thesis is that a one-category concentration with double-digit year-over-year growth but negative month-over-month momentum positions the brand to trade elasticity for share gains primarily through price and pack architecture.

These shifts imply that Big Pete's Treats is competing on price-driven velocity: a 14.88% year-over-year sales gain alongside a 4.97% price decline and a rank of 17 in California indicates room to climb via mix optimization rather than assortment expansion. The 35.29% 24-month growth, combined with a -5.49% month-over-month contraction in July 2026, points to repeat demand that is sensitive to promotional cadence, meaning the path forward is tighter price-pack alignment and targeted retail depth to convert periodic dips into steadier rank improvement. The thesis is that maintaining a single-category focus while managing elasticity can convert year-over-year unit wins into rank gains without needing cross-category diversification.

Competitive Landscape

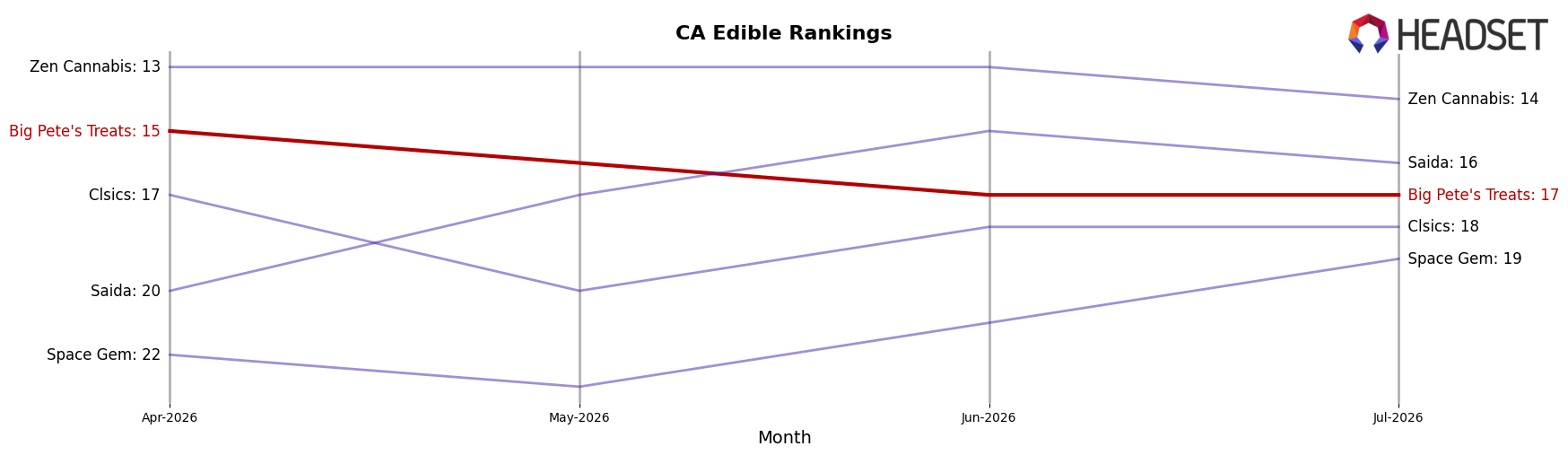

Big Pete's Treats sits at rank #17 in CA Edible for July 2026, improving 2 positions from #19 year over year, but slipping 2 spots from #15 in April 2026 to #17 in July 2026; in contrast, Wyld held #1 with a 2.20% YoY sales lift while Good Tide remained #5 with a 22.07% YoY increase, indicating that Big Pete's Treats is inching up the table YoY but giving back near-term gains as faster-growing leaders widen the gap. The brand’s 3-month rank eased from #15 to #17 while its peak rank matched #15 in April 2026, whereas Camino stayed #2 with 14.77% YoY growth and Kanha / Sunderstorm stayed #3 with 14.64% YoY growth, implying the current trajectory points to stabilization below the top 15 unless momentum accelerates relative to higher-growth incumbents.

Notable Products

Sleepy Time - THC/CBN 2:1 Indica Chocolate Chip Mini Cookies 10-Pack (100mg THC, 50mg CBN) posted the steepest decline at -21.1% and slipped within the top 10 at rank 9, while Strawberry & Watermelon Live Rosin Gummies 10-Pack (100mg) also contracted -10.6% at rank 6. In contrast, Indica Fruity Blast Crispy Marshmallow Treat (100mg) rose +21.9% to hold rank 1 and Chocolate Chip Mini Cookies 10-Pack (100mg) advanced +11.3% at rank 3. With eight of the top ten coming from the Edible category and two Sleepy Time SKUs splitting performance between -21.1% and +9.9% at ranks 9 and 7, the mix points to a pivot away from sleep-positioned line extensions toward faster-moving daytime edibles that can scale.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.