Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

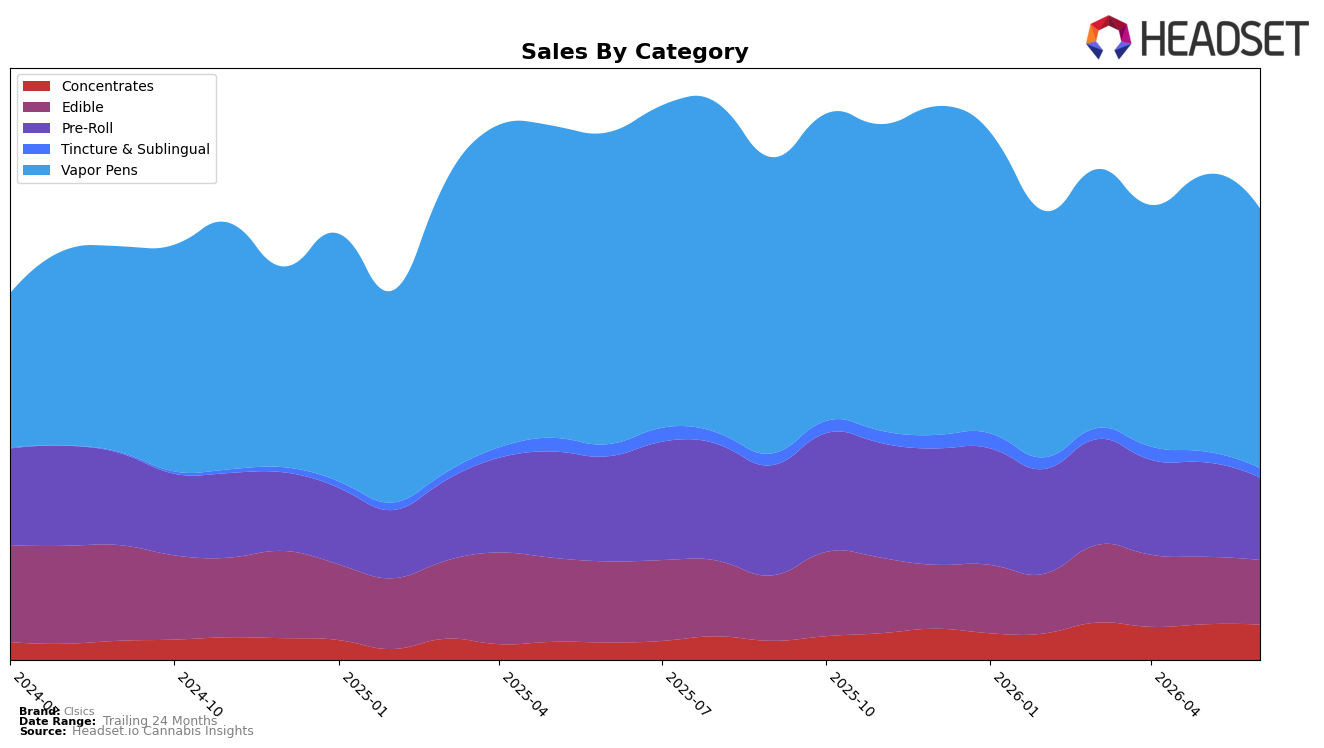

In June 2026, Clsics’ mix tilted further toward Vapor Pens at 56.91% share (ranked 16 in California Vapor Pens), even as Vapor Pens declined -16.68% YoY and -6.15% MoM; Pre-Roll fell faster at -21.42% YoY and -12.70% MoM while holding 18.25% share. Edible contracted -19.83% YoY and -4.06% MoM at 14.41% share, whereas Concentrates surged 93.56% YoY with only a -0.98% MoM dip, reaching 8.04% share. With brand-wide sales down -14.23% YoY and average price down -4.68% YoY, the pattern implies price-led pressure in larger formats while a high-growth Concentrates pocket is offsetting declines in the bigger buckets, leaving overall mix concentration in Vapor Pens a drag on near-term momentum.

The shifts suggest repositioning leverage: Concentrates’ 93.56% YoY growth against a near-flat -0.98% MoM compares favorably to Pre-Roll’s -12.70% MoM slide and Edible’s -4.06% MoM dip, indicating that incremental share gains will come faster from deepening the 8.04% Concentrates slice than defending shrinking Pre-Roll and Edible. Because Vapor Pens still commands 56.91% share yet contracted -6.15% MoM, the implication is that stabilizing rank 16 in California hinges on selective SKU rationalization and price-pack architecture in Vapor Pens, while reallocating promo depth toward Concentrates to convert its YoY outperformance into mix accretion and mitigate the -14.23% YoY brand decline.

Competitive Landscape

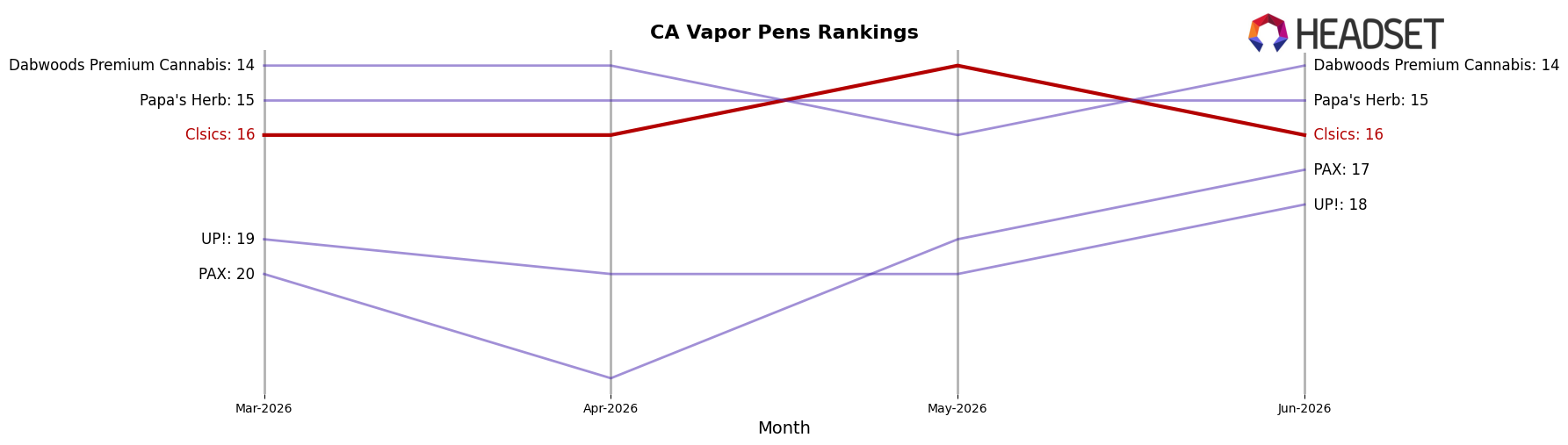

Clsics sits at rank #16 in CA Vapor Pens in June 2026, down 2 positions year over year from #14, and flat versus March 2026 at #16; its historical peak was #13 in May 2025, indicating a 3-spot gap from its best. Competitive momentum is moving away from the middle: Jetty Extracts climbed from #5 to #3 with a 47.3% year-over-year sales lift while Plug Play slipped from #3 to #4 with a 7.0% decline, and category leaders are mixed as STIIIZY holds #1 with a 7.0% sales contraction and Raw Garden remains #2 with an 11.0% increase. The pattern implies Clsics is stuck in a stable-but-drifting tier where upward mobility is getting harder as faster risers consolidate above and underperformers fall but remain ahead, so maintaining #16 after a 2-rank YoY drop signals the need to create a catalyst to re-close the 3-rank gap back to the May 2025 peak.

Notable Products

Cereal Milk Live Rosin Disposable (1g) posted the steepest decline in June 2026 at -13.2% and slid to rank 3, while Pink Lemon Up Live Rosin Disposable (1g) fell -12.9% at rank 6, signaling concentrated pressure within vapor pens despite Blue Crack Live Rosin Disposable (1g) holding rank 2 at -3.8%. Edibles were steadier: CBD/CBN/THC 1:1:1 Blueberry Milk Live Rosin Gummies 10-Pack (100mg CBD, 100mg CBN, 100mg THC) eased -6.7% yet led at rank 1, and Mountain Berry Live Rosin Gummies 10-Pack (100mg) grew 4.6% at rank 8 as five of the top ten were Edible SKUs. The balance of a $95,729 vapor pen leader against a rank-1 edible anchor implies a pivot where gummies carry baseline velocity while select pens face volatility.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.