Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

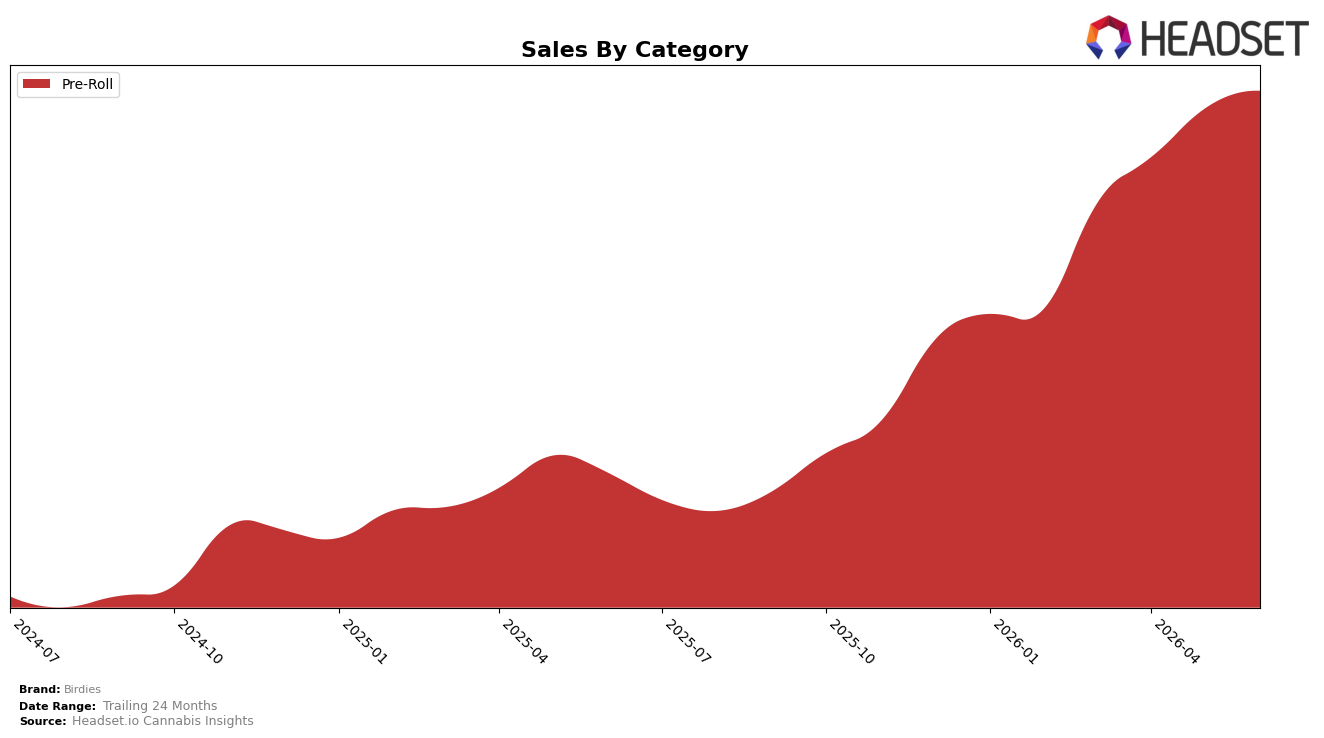

In June 2026, Birdies operated as a single-category brand with Pre-Roll at 100.0% of mix, posting 122.99% year-over-year growth and a 2.65% month-over-month lift, while average price declined 20.07% YoY to $21.56. Within the California Pre-Roll context, Birdies held rank 12 and posted 377.59% sales growth over 24 months, indicating a scale-up that coincided with price compression and steady monthly volume gains; the pattern implies Birdies is trading price for velocity inside a concentrated category footprint.

The combination of a 20.07% YoY price decline alongside 122.99% YoY sales growth and a modest 2.65% MoM uptick suggests Birdies is competing on accessible price points to drive unit throughput, which sustains a rank of 12 in California Pre-Roll despite single-category concentration at 100.0%. The 377.59% 24‑month expansion paired with a flat category mix implies limited diversification risk near term but potential ceiling effects at rank 12; the pattern implies Birdies’s positioning is volume-led within Pre-Roll, relying on continued price efficiency rather than mix expansion to gain share.

Competitive Landscape

Birdies sits at rank #12 in California Pre-Roll for June 2026, a 32-place climb from #44 year over year, with its three-month position steady at #12 while reaching a new peak rank of #12 in June 2026; by contrast, Jeeter held #1 with no YoY rank change and CannaBiotix (CBX) advanced from #7 to #4 alongside a 39% YoY sales increase. With STIIIZY fixed at #2 year over year and Kingpen stable at #3 while Birdies rose 32 ranks but did not move quarter-over-quarter, the pattern implies Birdies has completed a rapid recovery into the tier just outside the top 10 and now needs incremental share gains to convert stabilization into upward mobility.

Notable Products

Ultra Hybrid THCA diamonds Infused Pre-Roll 5-Pack (4.2g) posted the steepest decline at -19.9% month over month, slipping to rank 8 while the Classic Indica Blend Pre-Roll 3-Pack (2.1g) fell -11.2% at rank 6. In contrast, Ultra Indica THCA diamonds Infused Pre-Roll 5-Pack (4.25g) rose +16.2% to rank 7, and the Hybrid Classic Pre-Roll 10-Pack (7g) gained +6.6% at rank 2. The mix signals that infused Hybrid SKUs are losing traction even as Indica-infused options and core Hybrid formats stabilize, implying selective consumer uptake within the infused line.

Sativa Classic Blend Pre-Roll 10-Pack (7g) remains rank 1 despite a -8.9% dip, while the Classic Sativa Blend Pre-Roll 3-Pack (2.1g) advanced +8.0% at rank 4. Nine of the top ten are Pre-Roll SKUs clustered in Classic 10-Packs and 3-Packs alongside a smaller infused segment, indicating concentration in value multi-packs. The pattern implies Birdies is anchored by Classic multi-pack demand with cautious upside in Indica-infused formats rather than a broad infused expansion.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.