Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

CAM is stocked at 642 licensed dispensaries across California, New York, and Illinois, 564 of them in California, with the deepest coverage in Los Angeles, Sacramento, San Diego, Santa Ana, and Costa Mesa. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

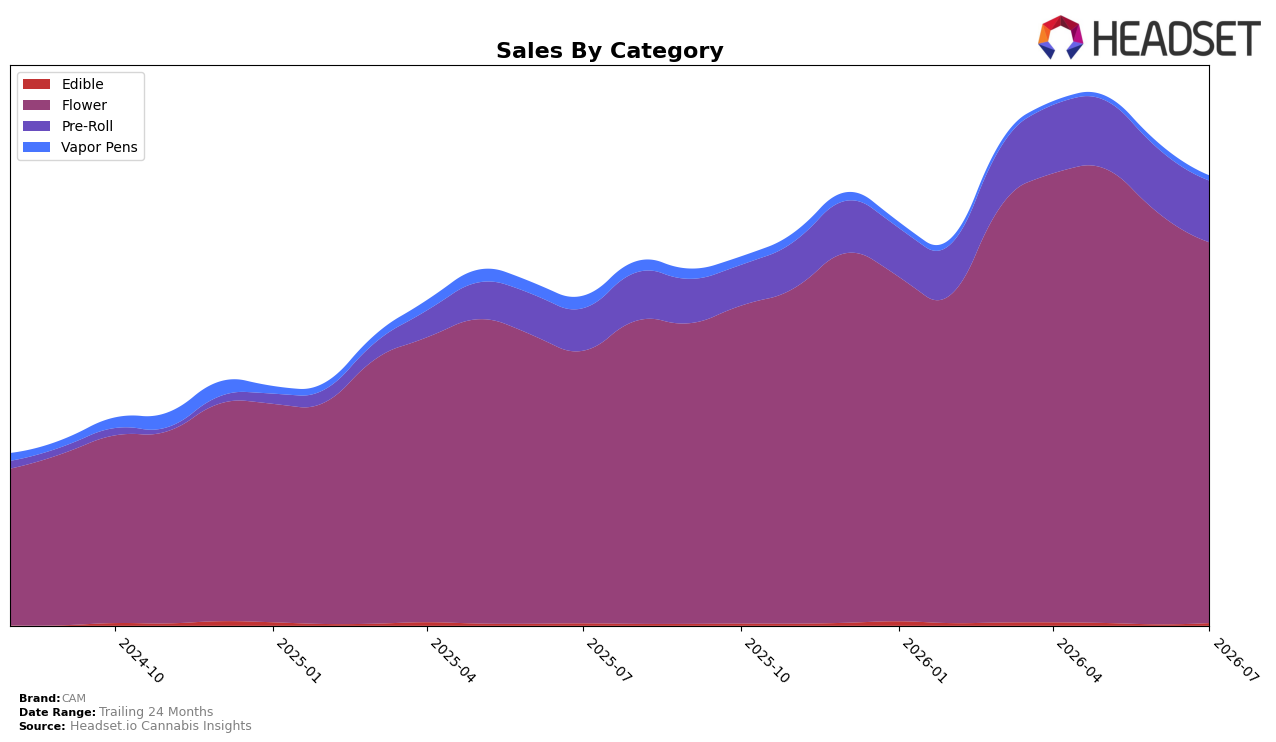

In July 2026, CAM’s mix concentrated further in Flower at 82.58% share with 39.10% year-over-year growth despite a 7.43% month-over-month dip, while Pre-Roll held 14.07% share with 41.32% year-over-year growth and a 3.72% month-over-month decline. Vapor Pens contracted to 1.94% share with a 44.64% year-over-year drop and an 8.10% month-over-month decline, whereas Edible, at 1.41% share, grew 4.49% year-over-year and jumped 23.09% month-over-month. The pattern implies CAM is doubling down on inhalables led by Flower and Pre-Roll for annual growth, while a small but accelerating Edible uptick is offsetting near-term softness in inhalables on a monthly basis.

With Flower ranked 3 in California and accounting for 82.58% of sales, the category weight elevates CAM’s exposure to rank volatility when Flower pulls back month-over-month by 7.43%, even as year-over-year gains of 39.10% support the brand’s broader 34.81% annual growth. Pre-Roll’s 41.32% year-over-year rise alongside a 3.72% month-over-month decline suggests cross-category reliance on inhalable demand cycles, while the 23.09% month-over-month surge in Edible, though only 1.41% share, provides a counter-cyclical buffer as Vapor Pens retreat 44.64% year-over-year. The implication is a positioning anchored in premium inhalables in California where rank 3 in Flower can sustain brand-scale momentum, but portfolio risk is concentrated unless the early Edible momentum is cultivated to diversify monthly swings.

Competitive Landscape

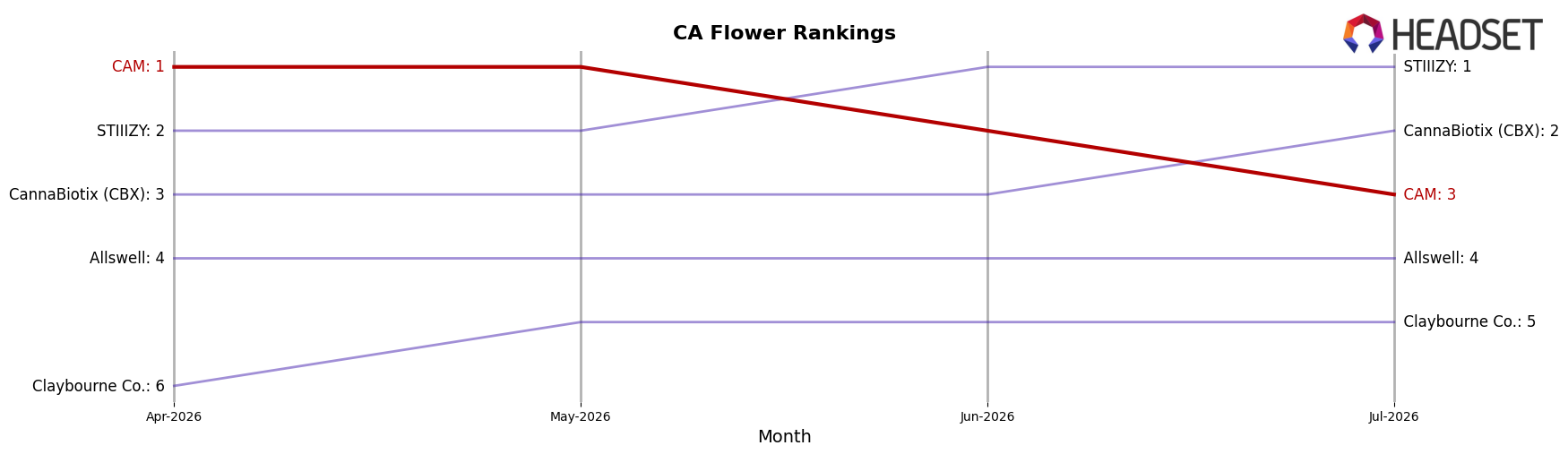

CAM is ranked #3 in CA Flower in July 2026, improving 1 place year over year from #4, but dropping 2 places from its peak at #1 in May 2026; meanwhile, STIIIZY sits at #1 after rising from #2 with 59.7% year-over-year sales growth, and CannaBiotix (CBX) holds #2 after sliding from #1 with 7.0% growth. Against the broader set, Allswell moved from #5 to #4 with 17.3% growth while Claybourne Co. fell from #3 to #5 with a 1.4% decline, framing CAM’s shift from #1 three months ago to #3 now as a share redistribution rather than a demand collapse; the thesis is that CAM’s rank trajectory—up 1 place YoY but down 2 places since May 2026—implies short-cycle volatility driven by competitor surges rather than structural erosion.

Notable Products

Private Reserve - Pop (3.5g) posted the steepest decline in July 2026 at -36.7% MoM while sliding to rank 10, and Jack Herer (3.5g) fell -35.7% MoM at rank 2, indicating demand compression at both the premium tail and core top tier. Private Reserve - Bubba's Girl (3.5g) remained rank 1 despite a -28.3% MoM drop, and Bubba's Girl (7g) declined -11.3% at rank 3, concentrating risk as at least seven of the top ten SKUs are Flower. Bubba's Girl Smalls (28g) also contracted -10.7% MoM at rank 6, and Bubba's Girl Pre-Roll (1g) slid -33.9% at rank 5, while new entries like Private Reserve - Coconut Milk (3.5g) at rank 4 arrived without a reported MoM history amid a $271,360 anchor for the top SKU. The pattern implies CAM is over-weighted to Flower with synchronized declines across sizes and formats, signaling a need to rebalance mix toward products with steadier repeat rates and less price elasticity.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.