Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

In June 2026, Gelato’s mix concentrated further into Vapor Pens at 49.27% share while the category declined both year over year by 22.99% and month over month by 13.76%, pulling overall brand sales down 18.80% YoY amid a 4.37% YoY increase in average price. Pre-Roll held 23.64% share with sales down 16.34% YoY and 10.10% MoM, while Edible at 18.85% share contracted more sharply at 26.15% YoY and 18.44% MoM; in contrast, Flower rose 117.49% YoY and 17.28% MoM to 6.40% share, and Concentrates slid 24.64% YoY and 31.62% MoM to 1.83% share. The pattern implies overexposure to declining inhalable segments is outweighing gains in Flower, so mix rebalancing rather than pricing is the primary lever to stabilize volume.

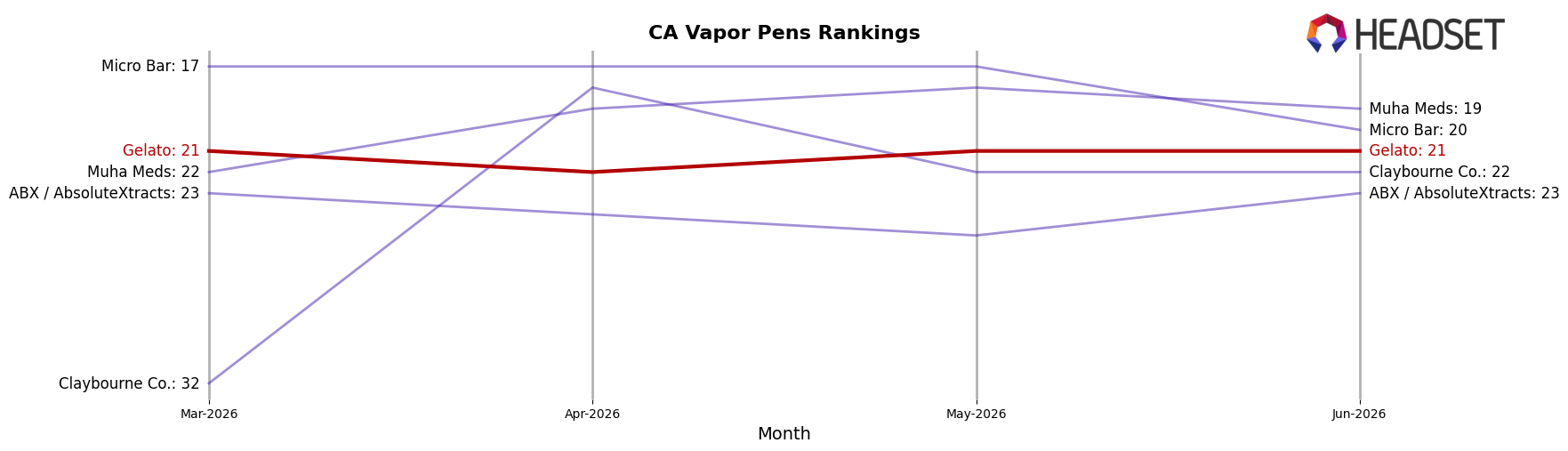

Positioning-wise, a 21 rank in Vapor Pens in California alongside a 13.76% MoM dip signals limited shelf velocity in the core category even as average price held at $11.86 and rose 4.37% YoY, while the 117.49% YoY surge in Flower suggests an emergent foothold that could diversify risk. With Pre-Roll and Edible shrinking 16.34% and 26.15% YoY respectively but still comprising 42.49% combined share, maintaining breadth without deepening declines becomes critical; the mix indicates Gelato can lean into Flower’s 17.28% MoM momentum while containing exposure to categories posting double-digit MoM drops, implying a pivot toward balanced inhalable-flower positioning to protect rank and margin.

Competitive Landscape

Gelato ranks #21 in CA Vapor Pens in June 2026, down 4 positions year over year from #17, and flat versus March 2026 at #21; this contrasts with Jetty Extracts rising from #5 to #3 alongside a 47.3% YoY sales increase and STIIIZY holding #1 while posting a -7.0% YoY sales change. Against a field where Raw Garden stayed at #2 with roughly 11.0% YoY growth and Plug Play slipped from #3 to #4 with a -7.0% YoY sales change, Gelato’s current #21 position is well off its peak of #9 in June 2024, indicating a two-year drift from peak visibility and implying the brand now competes more with mid-pack volatility than with top-10 momentum.

Notable Products

Sour Diesel Pre-Roll (1g) posted the steepest movement in June 2026 with a -50.5% month-over-month decline while holding a shared rank position at 5, indicating a sharp pullback despite staying within the top five. In contrast, Mango Dream Pre-Roll (1g) rose +35.9% MoM to rank 3, and Blue Dream Distillate Cartridge (1g) fell -20.2% to rank 8, marking a split between Pre-Roll momentum and Vapor Pens softness. Eight of the top ten SKUs are Pre-Rolls, and Chem Dawg Pre-Roll (1g) leads at rank 1 with $26,459 in sales, implying Gelato’s mix is consolidating around Pre-Rolls while Vapor Pens retrench, a setup that points to near-term focus on combustion formats over cartridges.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.