Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

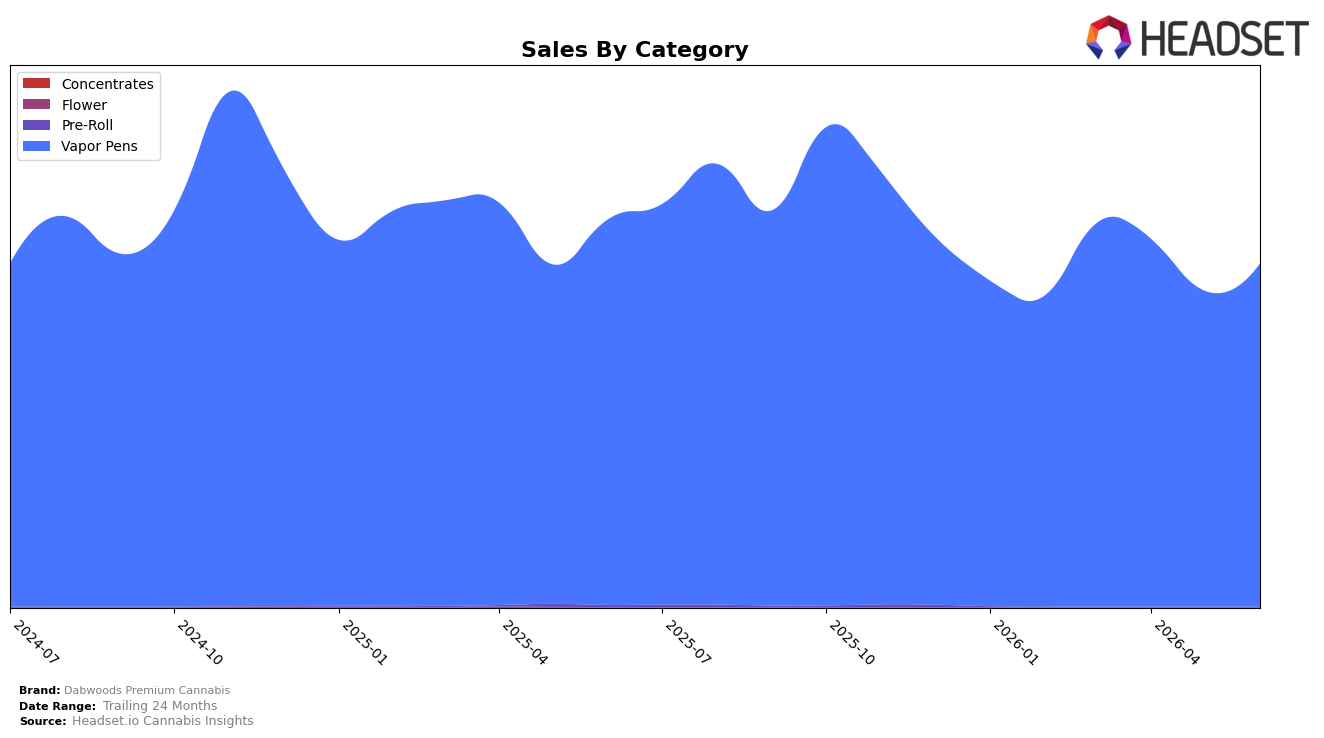

In June 2026, Dabwoods Premium Cannabis remained fully concentrated in Vapor Pens with a 100.0% category share, posting an 8.7% month-over-month lift while year-over-year sales declined 11.0%; the brand’s overall sales were down 11.4% YoY alongside a 10.1% YoY drop in average price, and it held rank 14 in Vapor Pens in California. The combination of a single-category mix at 100.0% and a MoM uptick of 8.7% against a YoY contraction of 11.0% implies a short-term rebound within Vapor Pens but continued pressure on annual velocity, suggesting that pricing and assortment within this category are the primary levers driving current performance.

The 10.1% YoY decline in average price alongside an 11.0% YoY sales contraction, despite an 8.7% MoM sales increase, indicates that recent gains are more volume- than price-led; holding rank 14 in California Vapor Pens while maintaining a 100.0% mix implies limited insulation from category headwinds and minimal cross-category hedge. This pattern implies the brand’s positioning is tightly tied to Vapor Pens price bands and promotional cadence, where defending or improving the rank 14 position will likely depend on managing discount depth relative to the 10.1% price decline while preserving the MoM momentum that delivered an 8.7% lift.

Competitive Landscape

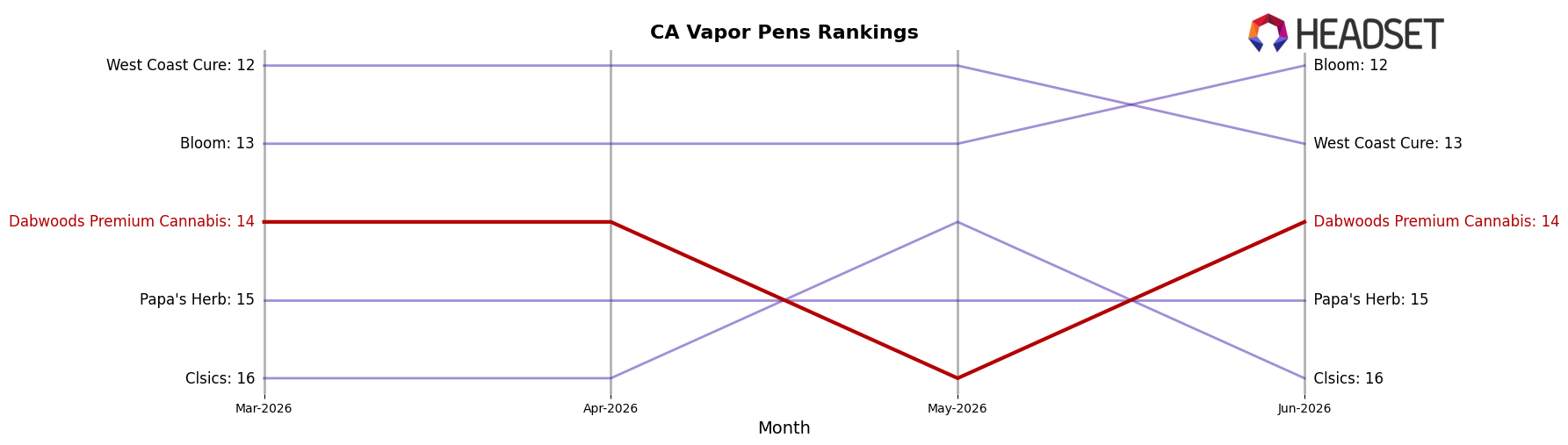

Dabwoods Premium Cannabis sits at rank #14 in CA Vapor Pens in June 2026, down 1 position from #13 year over year, and flat versus March 2026 at #14; this follows a prior peak of #11 in December 2024, indicating a three-rank slide since that peak and a stable but lower plateau. In the same period, Jetty Extracts climbed from #5 to #3 with a 47.32% YoY sales increase, while Plug Play moved from #3 to #4 alongside a -6.98% YoY sales change, and category leader STIIIZY held #1 despite a -6.95% YoY shift; these directional moves show competitors gaining or holding share through mix shifts while Dabwoods Premium Cannabis is ceding rank momentum. The pattern—minor YoY rank erosion of 1 position coupled with no quarter-over-quarter recovery and a three-rank drop from the December 2024 peak—implies a stall-out phase where maintaining share now depends on countering competitor mix gains rather than riding overall category tides.

Notable Products

Blue Melonade Liquid Live Diamond Dab Bar Disposable (1g) led June 2026 with a 49% month-over-month rise to rank 1, while Classic- Georgia Peach Distillate DabBar Disposable (1g) slipped 6% at rank 5. Marshmallow Dream Liquid Live Diamond Disposable (1g) climbed 29% to rank 2, and Classic Pineapple Kush Liquid Live Diamonds DabBar X Disposable (1g) advanced 32% to rank 4. With all top-10 items in Vapor Pens and four Liquid Live Diamond SKUs occupying ranks 1–2 and 4–6 with gains between 22% and 49%, the mix indicates a pivot toward live-resin-derived formats that concentrate velocity at the top of the lineup.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.