Market Insights Snapshot

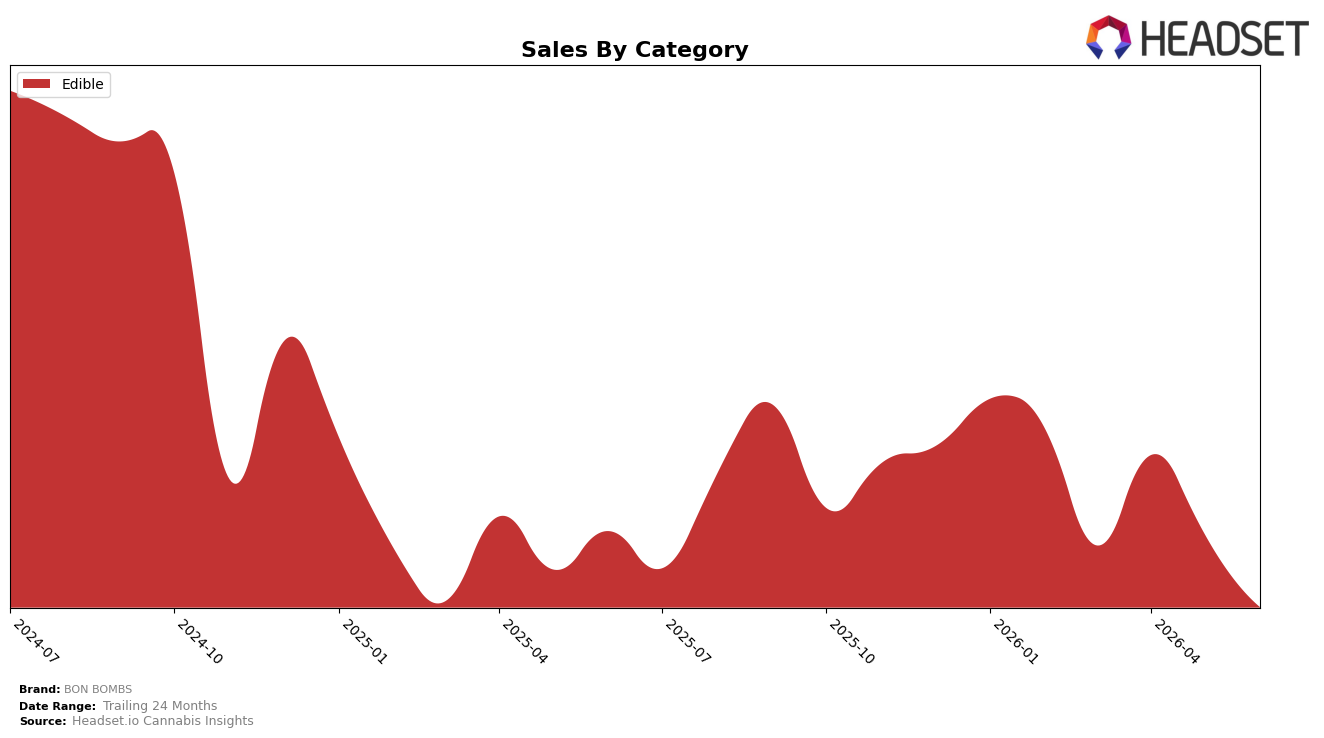

In June 2026, BON BOMBS operated as a single-category brand with Edible accounting for 100.0% of sales, down 6.50% year over year and down 6.26% month over month; average price rose 5.46% YoY to $18.33 while category share remained concentrated at 100%. Within Washington Edibles, the brand held rank 29, indicating a position that did not diversify into other categories and absorbed both a YoY contraction of 6.50% and a MoM dip of 6.26%; the implication is that a price-led strategy amid a one-category footprint is compressing volumes faster than price can offset, anchoring the brand at mid-pack rank 29.

The combination of 100.0% category concentration and a 5.46% YoY price increase alongside a 6.50% YoY sales decline suggests elasticity pressure within Edibles, where the current rank 29 leaves limited buffer against further MoM declines of 6.26%. This pattern implies BON BOMBS’s positioning is skewed toward defending margin in Edibles rather than gaining share, and without cross-category ballast the brand’s exposure to single-category volatility is elevating risk to both rank 29 stability and longer-horizon performance after a 29.22% decline over 24 months.

Competitive Landscape

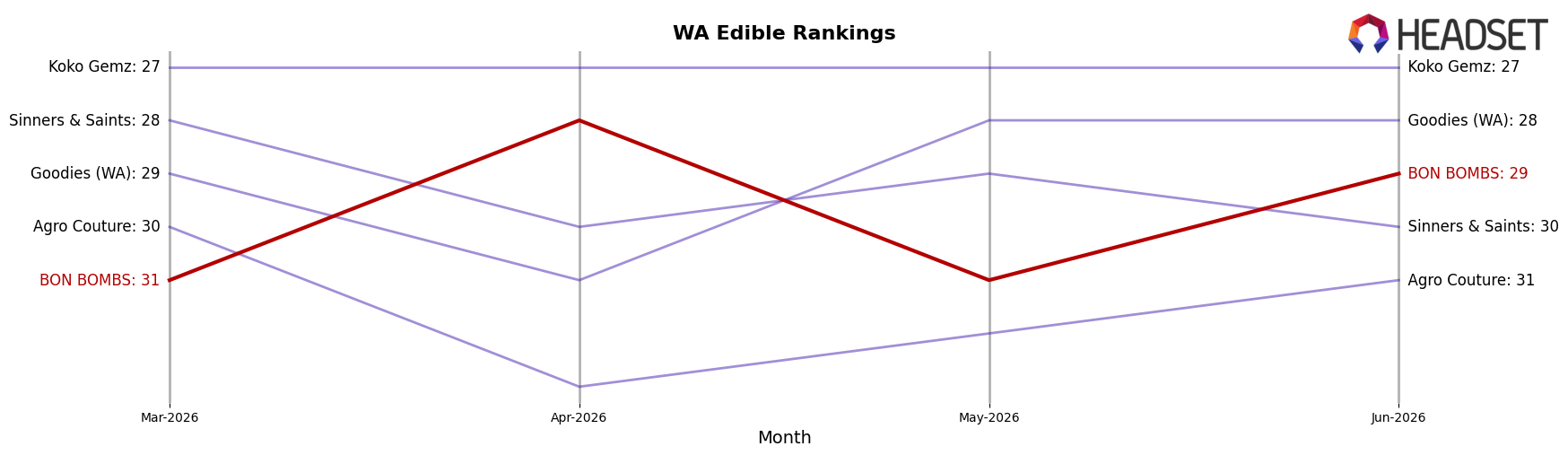

In June 2026, BON BOMBS sits at rank #29 in WA Edible, slipping 1 position year over year from #28 and improving 2 spots versus March 2026’s #31, while remaining 4 places below its peak of #25 from September 2024; by contrast, Wyld held #1 with a 7.3% YoY sales gain and Hot Sugar stayed #3 despite a 1.8% YoY sales decline, indicating the category’s upper tier is more stable than the lower ranks where BON BOMBS operates. With Green Revolution anchored at #2 and up 17.5% YoY while BON BOMBS posts a 1-rank YoY decline and only a 2-rank three-month lift, the directional gap suggests BON BOMBS’s current trajectory points to continued mid-pack churn unless it converts recent short-term rank gains into sustained movement toward the low-20s.

Notable Products

CBD/THC 1:1 Orange Dark Chocolate 10-Pack (100mg CBD, 100mg THC) posted the standout movement with a 49.6% month-over-month increase and a tied rank position at 3, while Sugar Free Raspberry Dark Chocolate 10-Pack (100mg) fell 13.2% and held rank 2. CBD/THC 1:1 Classic Milk Chocolate 10-Pack (100mg CBD, 100mg THC) rose 16.2% to rank 1, signaling that two 1:1 SKUs now bookend the leaderboard as sugar-free variants at ranks 2, 4, 5, 8, and 9 logged declines between 8.9% and 33.6%. The combined pattern implies a pivot toward cannabinoid-ratio chocolate leading growth as the sugar-free cluster sheds rank momentum, concentrating mix toward functional formats over dietary positioning.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.