Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Green Revolution is stocked at 325 licensed dispensaries across Washington, New York, and California, 232 of them in Washington, with the deepest coverage in Seattle, Tacoma, Spokane, Olympia, and Bellingham. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

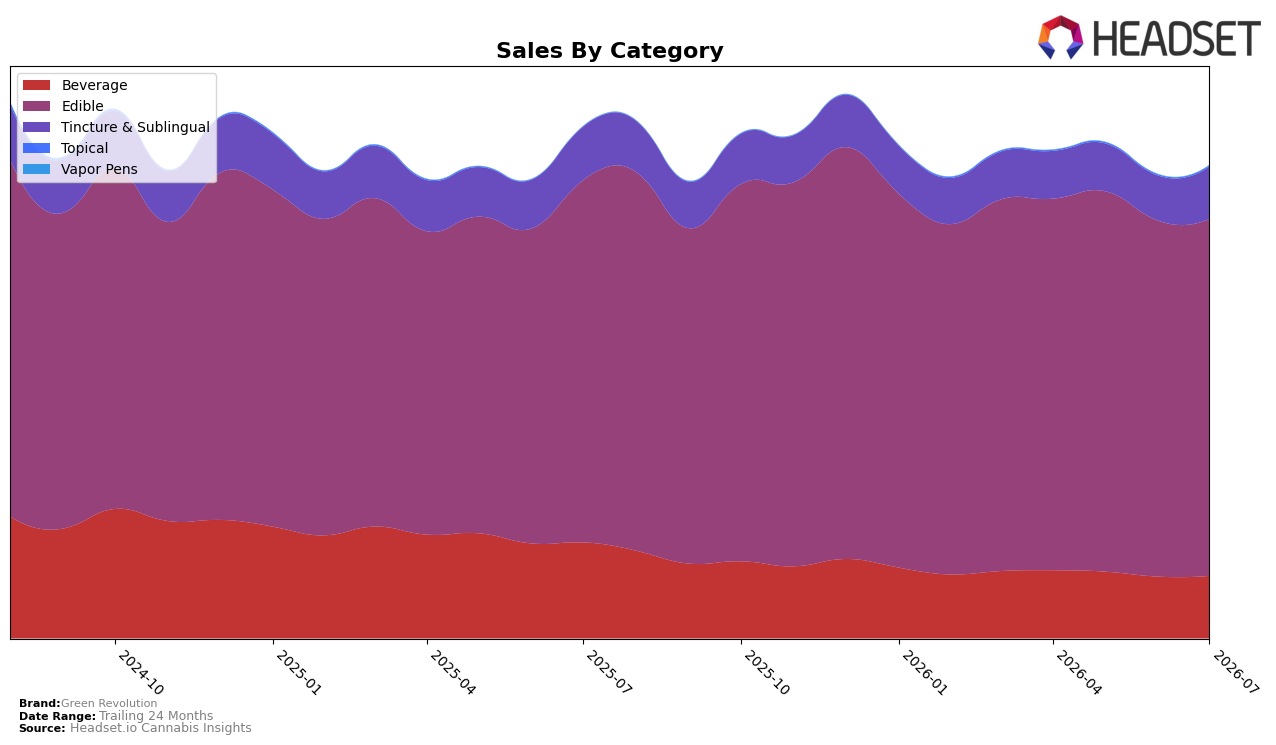

In July 2026, Green Revolution’s category mix concentrated further in Edible at 75.56% share with a modest 0.23% MoM uptick but a 1.47% YoY decline, while Beverage slid YoY by 35.01% despite a 1.13% MoM lift, taking share to 13.18%. Tincture & Sublingual rose 16.76% MoM but fell 1.75% YoY, reaching 11.06% share, and Topical spiked 702.37% YoY and 9.41% MoM yet remained just 0.19% of mix; the brand’s overall sales were down 7.62% YoY as average price rose 7.13%. With Edible ranked 2 in Washington, the mix signals dependence on a single category for rank while subcategory volatility, especially the Beverage contraction, offsets MoM gains and constrains total-brand recovery.

The combination of a 7.13% YoY price increase and a 7.62% YoY sales decline implies demand elasticity pressuring volumes in core Edible even as the brand holds a number 2 rank locally, while a 35.01% YoY Beverage drop reduces cross-category reach. The 16.76% MoM lift in Tincture & Sublingual alongside a 0.23% MoM Edible increase suggests near-term stability hinges on incremental gains in higher-priced formats, but the 0.19% Topical share, despite a 702.37% YoY surge, remains too small to diversify risk; taken together, the pattern implies the brand’s positioning is anchored in Edible with limited buffer from secondary categories, making category breadth the lever to mitigate price-driven volume headwinds.

Competitive Landscape

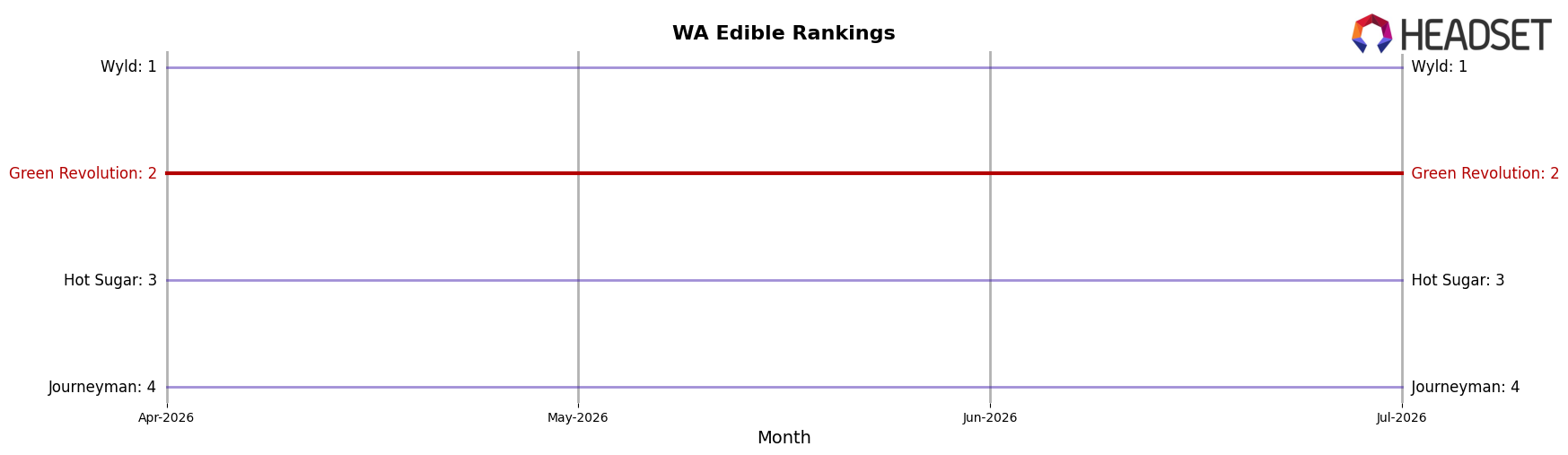

Green Revolution ranks #2 in Washington Edible for July 2026, unchanged from #2 year over year, and flat versus three months ago at #2, while the category leader Wyld held #1 both this year and last as its sales grew 7.99% YoY; meanwhile, Hot Sugar stayed at #3 with a 5.92% YoY decline and Journeyman improved from #5 to #4 on 6.47% YoY growth, indicating that Green Revolution’s steady #2 position amid a rising #1 and a climbing #4 implies a maturing share dynamic where maintaining rank likely requires outpacing mid-tier risers rather than only closing the gap to the leader.

Notable Products

Doozies Fly - Pineapple Gummies 10-Pack (100mg) posted the steepest decline at -12% while holding rank 6, and Nano Doozies - CBD/CBN /THC 1:1:1 Blue Raspberry Nighttime Gummies 10-Pack (50mg CBN, 50mg CBD, 50mg THC) slipped -9% but remained rank 1. In contrast, Doozies - CBD/THC 60:1 Juicy Peach Gummies 10-Pack (600mg CBD, 10mg THC) rose +14% to rank 2 as Doozies Elevate - CBD/THC 1:1 Juicy Peach Gummies 10-Pack (100mg CBD, 100mg THC) gained +7% at rank 8. With all top-10 SKUs in Edible and two new Doozies PLUS entries debuting at ranks 7 and 10 alongside mixed moves from -12% to +14%, the pattern implies the brand is consolidating around functional gummy formats while pruning momentum in classic THC-forward flavors.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.