Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

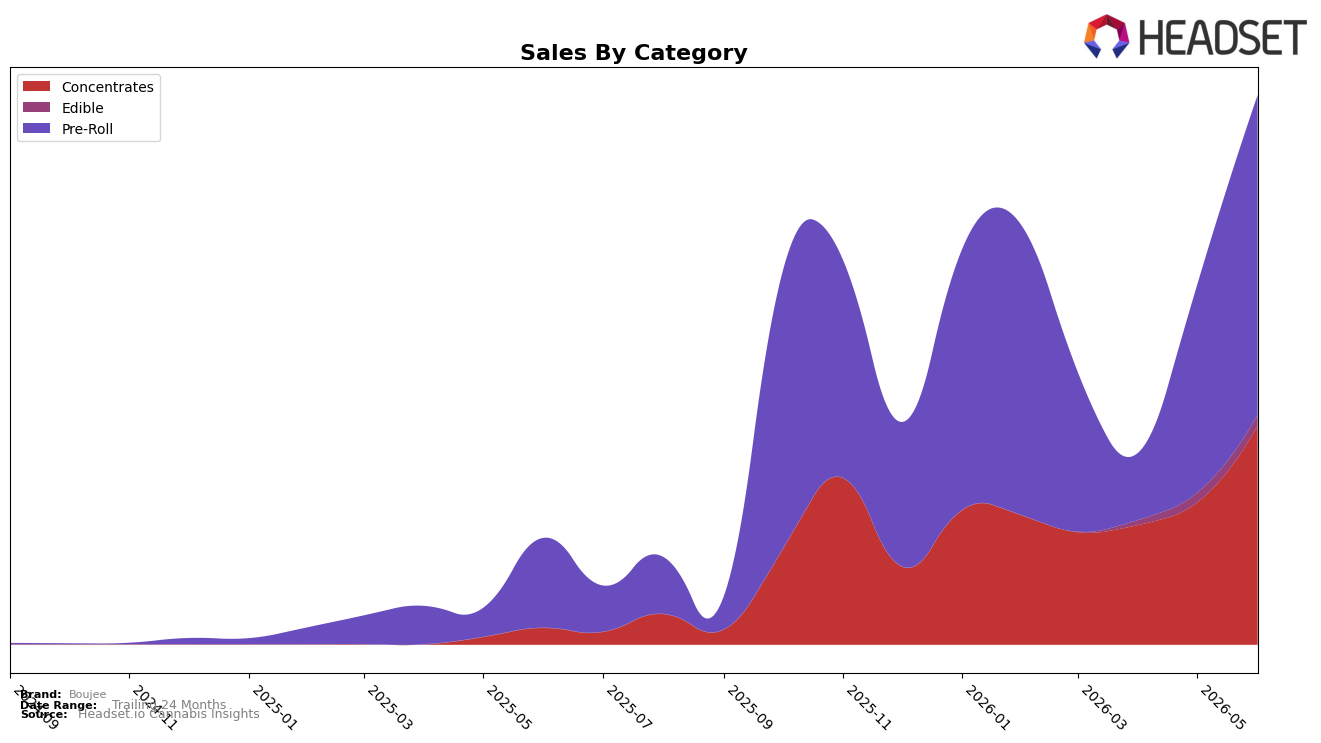

Boujee’s category mix in June 2026 concentrated 58.22% of sales in Pre-Roll with 256.60% year-over-year growth and 54.29% month-over-month growth, while Concentrates held 39.83% share with 1,228.16% year-over-year and 54.07% month-over-month gains; Edible contributed 1.95% share with 13.14% month-over-month growth and no year-over-year baseline. The average price fell 33.44% year-over-year to $15.32 alongside category-level expansion, and Pre-Roll ranked 57 in Michigan, indicating volume-led gains are outpacing price compression and that mix is tilting toward fast-turn formats where the brand can scale despite downpricing.

The simultaneous 54% month-over-month lifts in both Pre-Roll and Concentrates, paired with a 1,228.16% year-over-year surge in Concentrates versus 256.60% in Pre-Roll, implies Boujee is leveraging cross-format adoption to deepen penetration while relying on Pre-Roll’s 58.22% share for baseline throughput. With Concentrates nearing 40% share and Pre-Roll at rank 57 in Michigan, the portfolio suggests a two-engine strategy where Pre-Roll fuels reach and Concentrates accelerates basket trade-up, positioning the brand to convert price elasticity into higher unit velocity rather than defending margin at prior price points.

Competitive Landscape

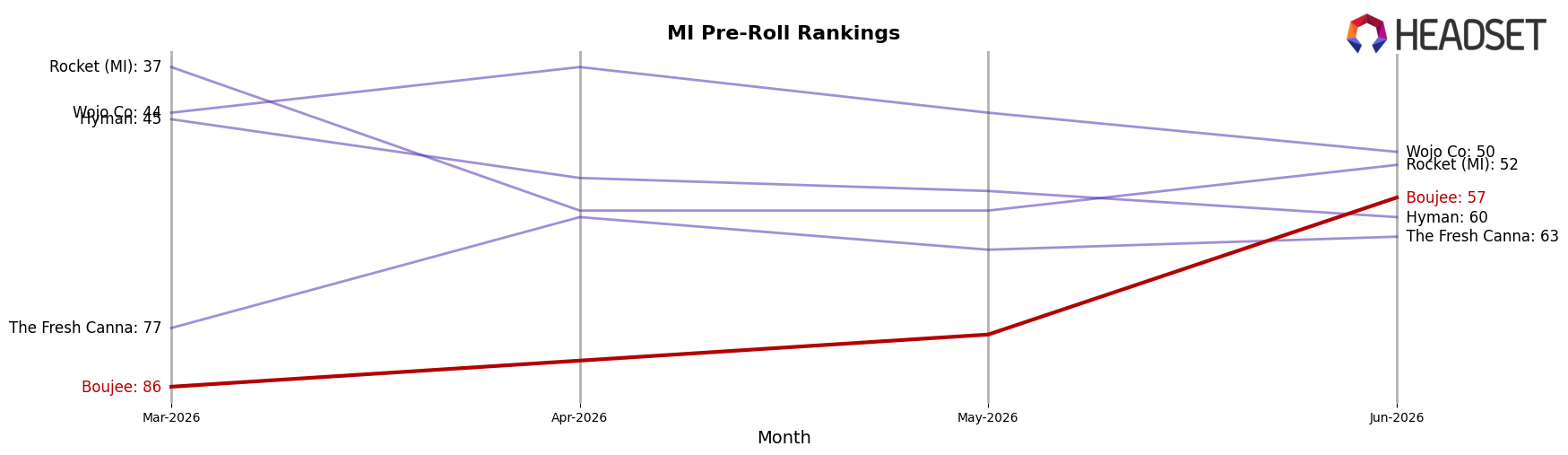

Boujee sits at rank 57 in MI Pre-Roll in June 2026 after climbing 61 positions from rank 118 year over year, and moving up 29 spots from rank 86 in March 2026; despite peaking at rank 50 in January 2026, it has slipped 7 places since that peak. In contrast, Jeeter held at #1 year over year while posting a 7.9% YoY sales decline, and Mitten Extracts advanced from #8 to #4 alongside a 114.4% YoY sales increase; against this backdrop, Boujee’s upward rank mobility outpaces static leaders but lags fast risers in the top five. The pattern implies Boujee is transitioning from lower-tier visibility toward mid-pack relevance, with momentum sufficient for further gains but not yet converting into top-50 persistence.

Notable Products

Cereal Milk Infused Pre-Roll (1.5g) posted the biggest move in June 2026 with a 125% month-over-month surge and a top-3 rank, while Terpaja Blast Infused Pre-Roll (1.5g) also crossed triple digits at +107% to land effectively in the top 3. Berry Gelato Infused Pre-Roll (1.5g) climbed 93% to rank 1 as Unicorn Piss Infused Pre-Roll (1.5g) advanced 60% to rank 2, whereas Strawberry Cough Infused Pre-Roll 6-Pack (2.7g) slipped 1% and held at rank 8. Five of the top ten are Pre-Roll SKUs concentrated in infused formats, and despite Snow Day Live Hash Rosin (5g) generating $42,939 at rank 6 with no prior baseline, the pace of gains clustered at ranks 1–5 implies a product strategy centered on high-potency infused Pre-Rolls driving the leaderboard.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.