Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

BoxHot is stocked at 20 licensed dispensaries across California, with the deepest coverage in Fresno, Los Angeles, San Jacinto, Vallejo, and Adelanto. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

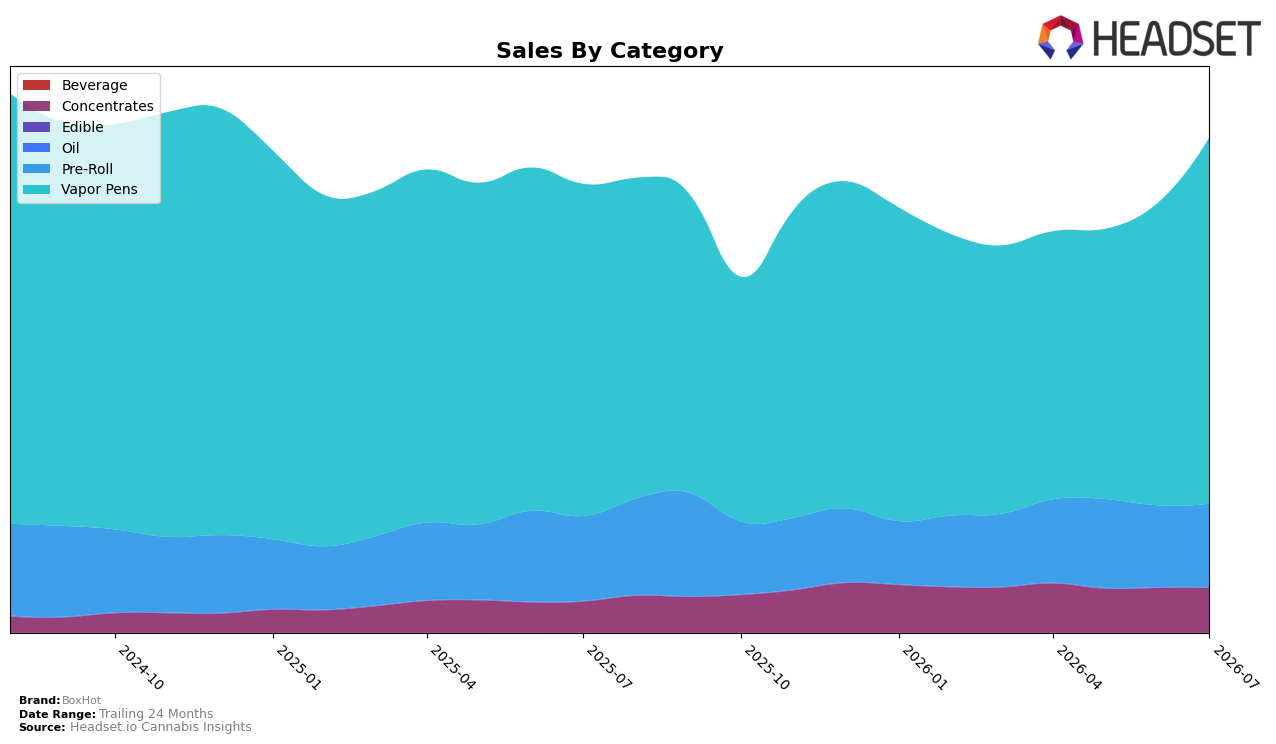

In July 2026, BoxHot concentrated 74.19% of sales in Vapor Pens with a 10.35% year-over-year increase and a 21.15% month-over-month jump, while Pre-Roll held 16.82% share with a -1.61% YoY dip but a 2.00% MoM uptick; Concentrates accounted for 8.99% share with a 44.03% YoY surge and a -0.22% MoM slip. The brand’s average price in July 2026 rose 0.50% YoY to $33.50, and overall brand sales advanced 10.41% YoY as the Vapor Pens-led mix outweighed Pre-Roll softness; the pattern implies BoxHot is leaning into a pen-led volume pulse while cultivating a higher-growth but smaller Concentrates niche that could rebalance mix if sustained.

With Vapor Pens at rank 2 in Alberta and carrying 74.19% of July 2026 sales, BoxHot’s positioning hinges on defending pen share as the primary growth engine while using the 44.03% YoY rise in Concentrates to diversify risk from category cyclicality; the -2.20% 24‑month sales change signals that mix concentration has a ceiling if pen momentum normalizes. The 2.00% MoM lift in Pre-Roll alongside a -0.22% MoM movement in Concentrates suggests near-term trial is broadening beyond pens without margin dilution, given Vapor Pens’ $36.25 average price versus $25.13 in Pre-Roll; the implication is that incremental share gains are most efficiently captured by premium-leaning pens while Pre-Roll acts as an entry ramp that supports, rather than displaces, the core.

Competitive Landscape

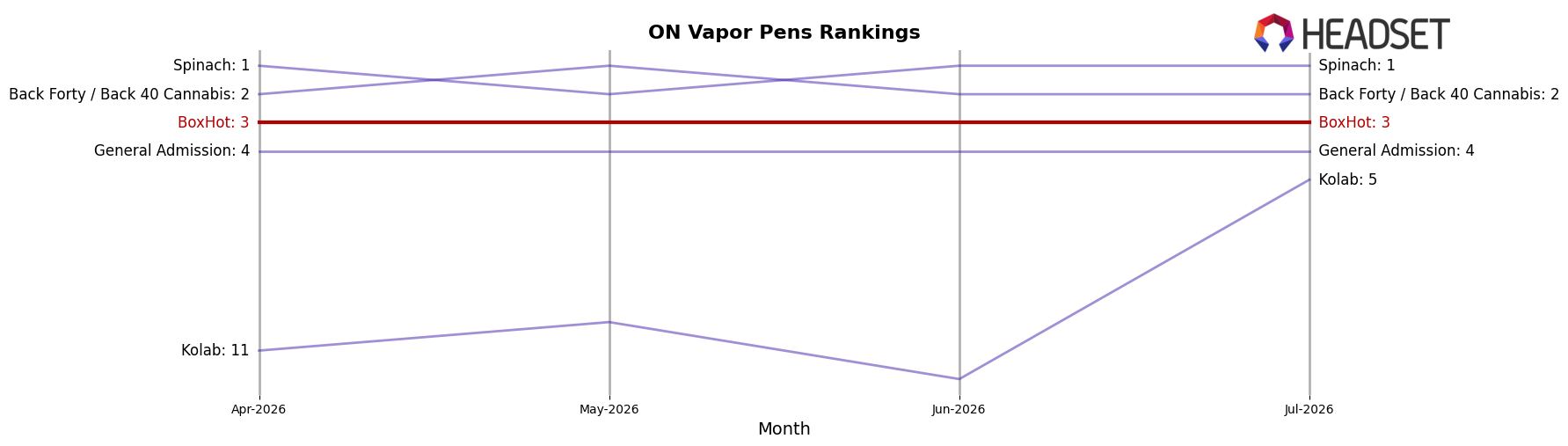

BoxHot sits at rank #3 in ON Vapor Pens in July 2026, down one spot from rank #2 year over year, and flat versus April 2026 at #3; the brand’s peak of #1 in June 2025 contrasts with today’s position, indicating a two-place slide from that high. Meanwhile, Spinach climbed from #4 to #1 with 144.7% year-over-year sales growth, and Back Forty / Back 40 Cannabis moved from #1 to #2 with 9.3% growth, while General Admission fell from #3 to #4 alongside an 19.0% decline; against this backdrop, BoxHot’s shift from #2 to #3 implies it is getting outpaced at the top end and must either recapture share from the current #1–#2 tier or risk settling into a mid-top position.

Notable Products

Peach OG Distillate Cartridge (1g) posted the steepest decline in July 2026 at -11.5% MoM while holding rank 2, and Retro - Code Blue Distillate Cartridge (1.2g) also slid -11.2% at rank 9, signaling elasticity pressure within legacy distillate SKUs even as category traffic stayed high. Pink Kush Liquid Diamond Charged Disposable (1g) rose +48.4% MoM to rank 4, and combined with three other Liquid Diamond entries in the top five, Vapor Pens accounted for eight of the top ten placements, indicating a tilt toward higher-spec resin formats over traditional distillate. Maui Madness Liquid Diamond Charged Cartridge (1g) led at rank 1 with $555,294, while Alien OG Distillate Cartridge (1.2g) softened -5.4% at rank 10, a spread that points to consumer migration toward Liquid Diamond SKUs at premium positions.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.