Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

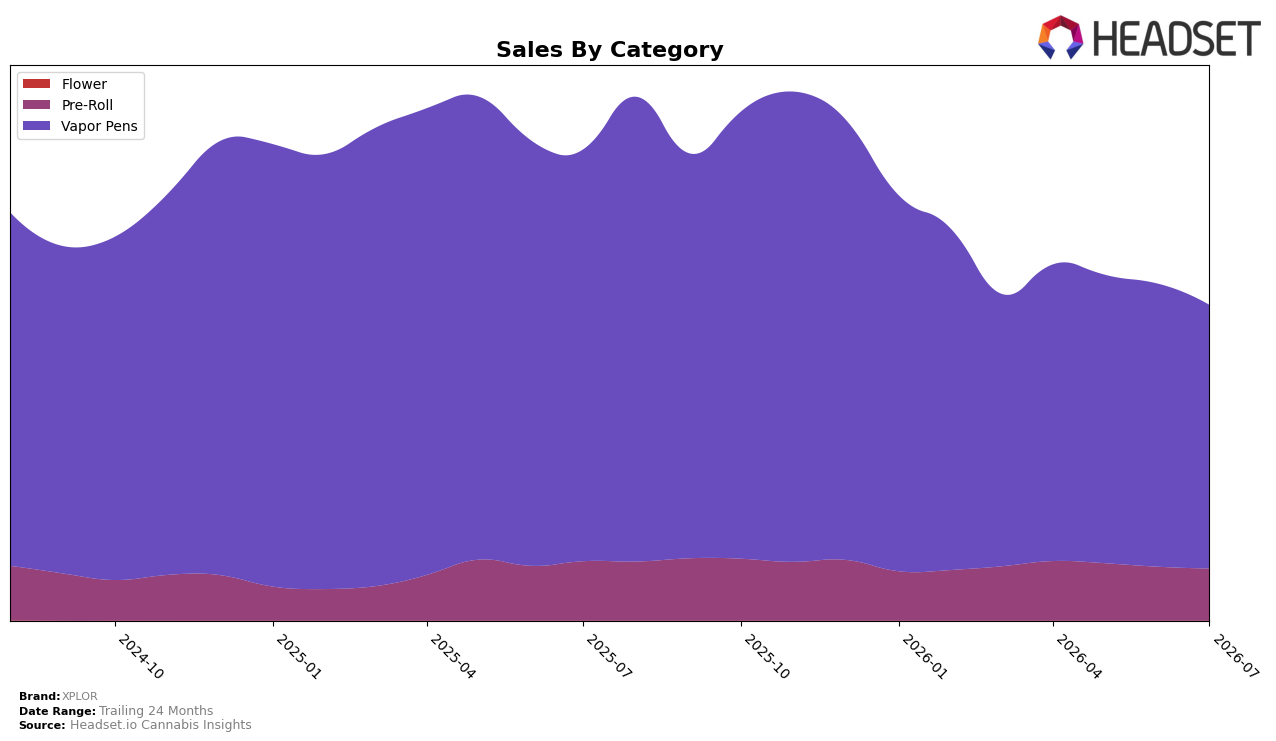

XPLOR concentrated 83.55% of July 2026 sales in Vapor Pens, with that category down 36.02% year over year and 6.88% month over month, while Pre-Roll held 16.45% share, declining 12.29% year over year and 3.28% month over month. Across the brand, sales fell 33.04% year over year and the average price dropped 8.81%, and within Vapor Pens the average price sat at $27.26 versus $10.53 in Pre-Roll; this mix and pricing profile implies volume leakage in the core segment as higher-priced Vapor Pens absorb most exposure to contraction.

The heavier weighting toward Vapor Pens in July 2026 alongside a 6th-place rank in Vapor Pens in Saskatchewan indicates that category-specific headwinds, not just overall demand, are shaping brand position, since the 36.02% Vapor Pens decline outpaced the 12.29% Pre-Roll decline and pulled total sales down 33.04%. With Vapor Pens still commanding 83.55% share but slipping faster month over month than Pre-Roll by 3.60 percentage points (6.88% vs. 3.28%), the current mix concentrates risk in a higher-price segment where elasticity is biting, suggesting that incremental share reallocation toward Pre-Roll could stabilize rank and mitigate further erosion in Vapor Pens-dependent markets.

Competitive Landscape

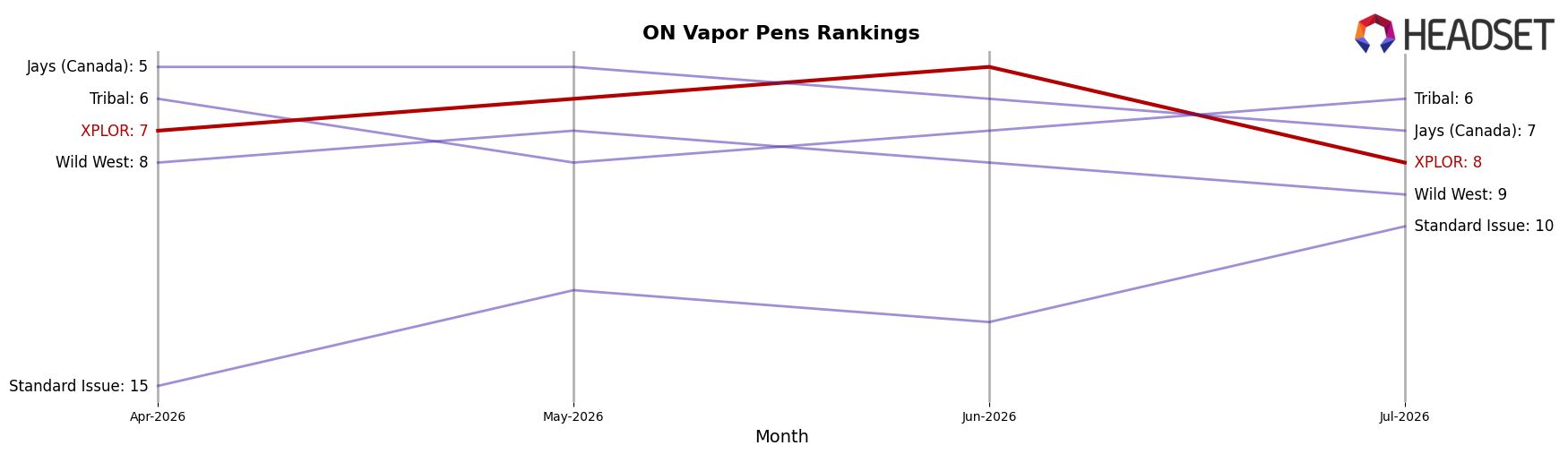

XPLOR sits at rank #8 in ON Vapor Pens in July 2026 after sliding 3 positions year over year from #5 and easing 1 place since April 2026 when it was #7, while its historical peak was #3 in February 2025. In contrast, Spinach advanced to #1 with a 144.7% year-over-year sales increase from a lower #4 base, and BoxHot holds #3 with a 4.6% YoY lift as General Admission sits at #4 despite an 19.0% YoY decline; this competitive reshuffle, paired with XPLOR’s drop from #7 to #8 over the past three months and from #5 to #8 year over year, implies XPLOR is ceding share to faster-moving leaders and must pivot to arrest a multi-quarter downtrend.

Notable Products

Nana's Jam CO2 Cartridge (1g) slid to rank 1 with a -12.9% month-over-month change in July 2026, while Red Hawaiian Co2 Cartridge (1g) at rank 2 fell -21.1%, and Jungle Fruit CO2 Cartridge (1g) at rank 8 dropped -17.0%. Beast Berry CO2 Cartridge (1g) at rank 4 was a counter-mover with +22.9% MoM, and Comet Clusters Distillate Cartridge (1g) at rank 5 added +5.5%, with six of the top ten coming from Vapor Pens, indicating a category concentration despite mixed momentum. The split between double-digit declines at the top and mid-pack gains suggests XPLOR is relying on a broader Vapor Pens lineup to hedge flagship volatility, pointing to a portfolio strategy that prioritizes width over singular hero SKUs.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.