Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

Broken Coast concentrated 81.31% of June 2026 sales in Flower with a 61.02% year-over-year increase and a 6.99% month-over-month gain, while Pre-Roll held 18.69% share with a -5.49% year-over-year decline but a 12.85% month-over-month lift. The brand’s average price rose 3.34% year over year to $29.55, alongside category pricing contrasts of $50.42 in Flower and $10.55 in Pre-Roll, indicating mix-driven revenue effects rather than broad price inflation. With overall brand sales up 42.30% year over year and Flower ranked 10 in Alberta, the pattern implies a scale-up anchored in premium Flower while Pre-Roll volatility adds incremental volume without displacing the core.

The widening skew toward Flower—up 61.02% year over year versus a -5.49% year-over-year shift in Pre-Roll and paired with a 6.99% vs. 12.85% month-over-month cadence—suggests the brand is prioritizing higher-ticket core products while using Pre-Rolls tactically for short-cycle traffic. Holding a 10th-place Flower rank in Alberta alongside a 3.34% average price increase and an 81.31% mix weight implies price elasticity headroom in the core, but also signals that further share gains likely depend on keeping Pre-Roll growth accretive to mix rather than dilutive to margin.

Competitive Landscape

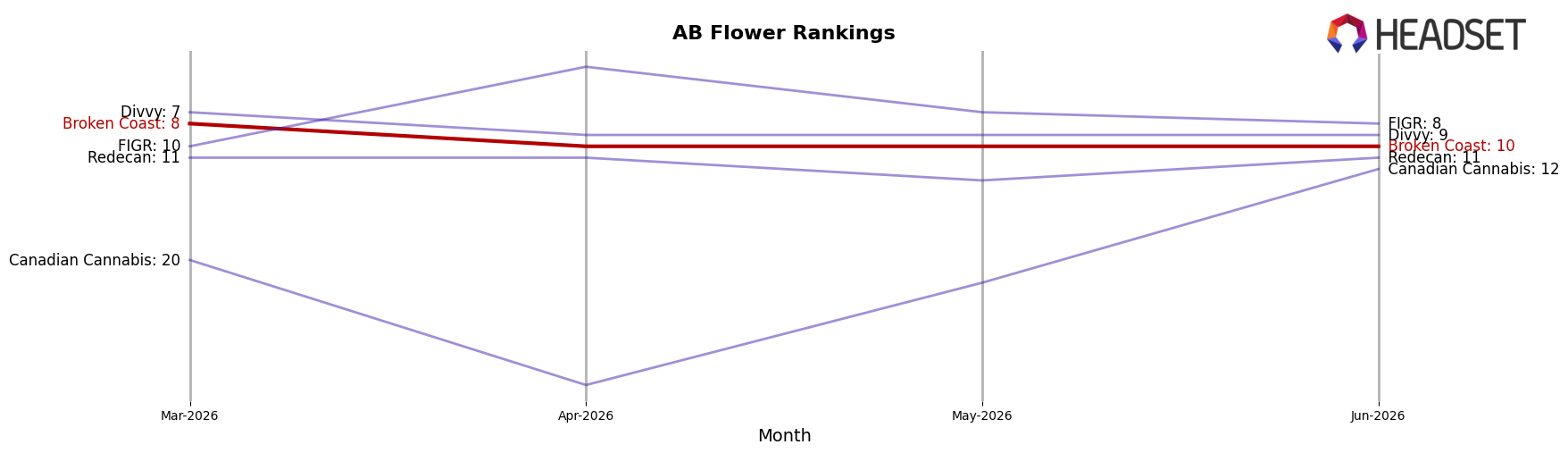

Broken Coast sits at rank #10 in AB Flower in June 2026, a 2-position improvement from #12 year over year, but a 2-position decline from #8 three months ago; this sits below its peak of #7 in January 2026 while the category’s top end tightened as Pure Sunfarms climbed from #4 to #1 and Big Bag O' Buds advanced from #7 to #3. In contrast, Good Supply fell from #1 to #5 with a 41.0% YoY sales decline while Back Forty / Back 40 Cannabis held at #2 despite a 23.5% YoY contraction, indicating that Broken Coast’s modest 2-rank YoY rise alongside a 2-rank slide since March places it in a stalled middle tier where upward mobility likely depends on displacing stable incumbents rather than benefiting from top-tier pullbacks.

Notable Products

Platinum Pave Blunt (1g) posted the steepest decline in June 2026, falling 28.8% month over month to rank 6, while Coffee Creamer (3.5g) also contracted 11.6% at rank 7. In contrast, Cherry Ztripez (7g) surged 38.8% to rank 2 and Blue Dream Blunt (1g) grew 14.2% to hold rank 1, creating a split where gains concentrate at the top despite mid-pack erosion. Flower dominates breadth with four of the top ten SKUs and Pre-Rolls hold the top spot, implying Broken Coast is leaning into dual pillars where premium 7g Flower lifts volume while flagship Blunts anchor velocity.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.