Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

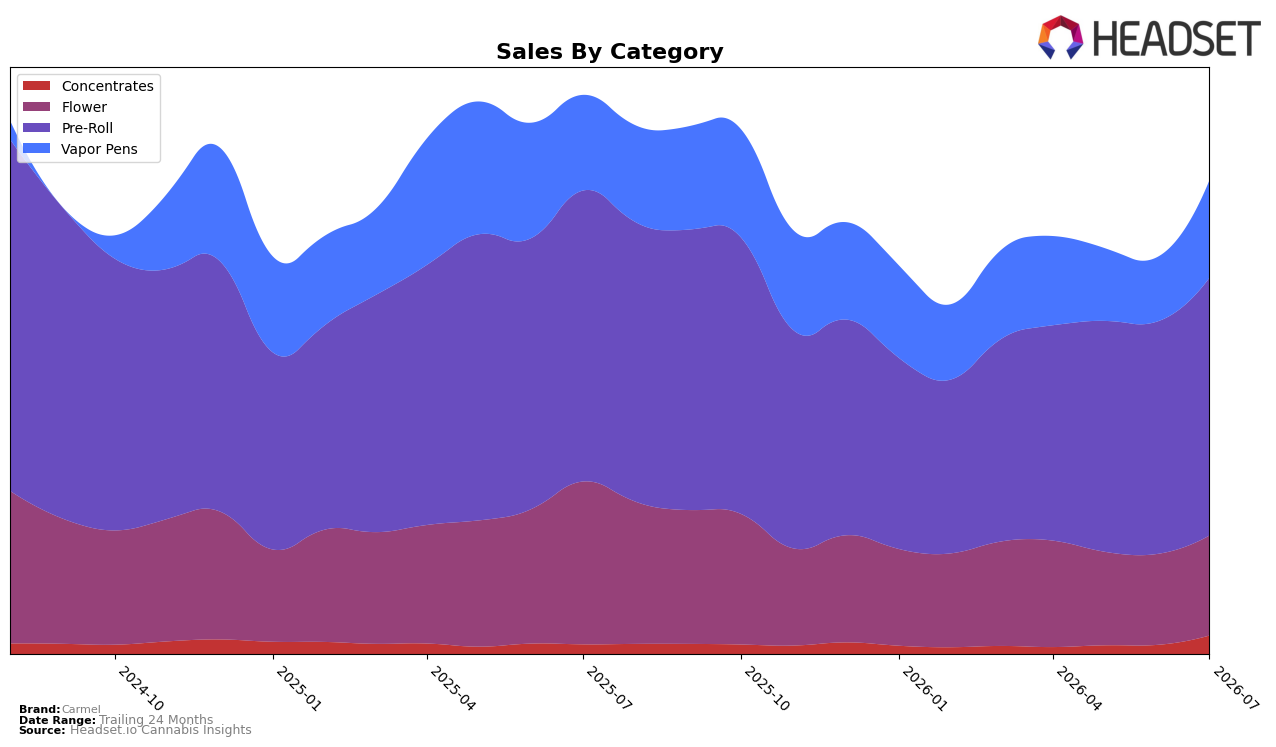

Carmel’s category mix in July 2026 tilted further toward Pre-Roll at 53.59% share, where sales were down 11.31% year over year but up 10.66% month over month, while Vapor Pens climbed to 20.70% share with a 1.89% year-over-year increase and a 48.51% month-over-month jump. Flower contracted to 21.21% share with a 37.81% year-over-year decline despite a 9.59% month-over-month lift, and Concentrates expanded to 4.51% share on a 67.00% year-over-year rise and a 73.47% month-over-month surge. With brand sales down 14.92% year over year and the average price down 4.81%, the pattern implies a shift toward lower-priced, faster-turning formats buffering declines in legacy Flower while momentum concentrates in Pre-Roll and Vapor Pens.

Positionally, Carmel’s weight in Pre-Roll and accelerating Vapor Pens suggests a pivot toward convenience-led formats, with July 2026 gains of 10.66% month over month in Pre-Roll and 48.51% month over month in Vapor Pens indicating short-cycle trial and repeat that can support share even as Flower’s 37.81% year-over-year decline compresses premium basket size. Holding rank 11 in Pre-Roll in Ontario while Pre-Roll share sits at 53.59% and Vapor Pens at 20.70% implies that tightening assortment and price architecture in these two lanes could translate into rank lift, as Concentrates’ 67.00% year-over-year growth and 73.47% month-over-month spike offer a high-growth niche rather than a scale driver.

Competitive Landscape

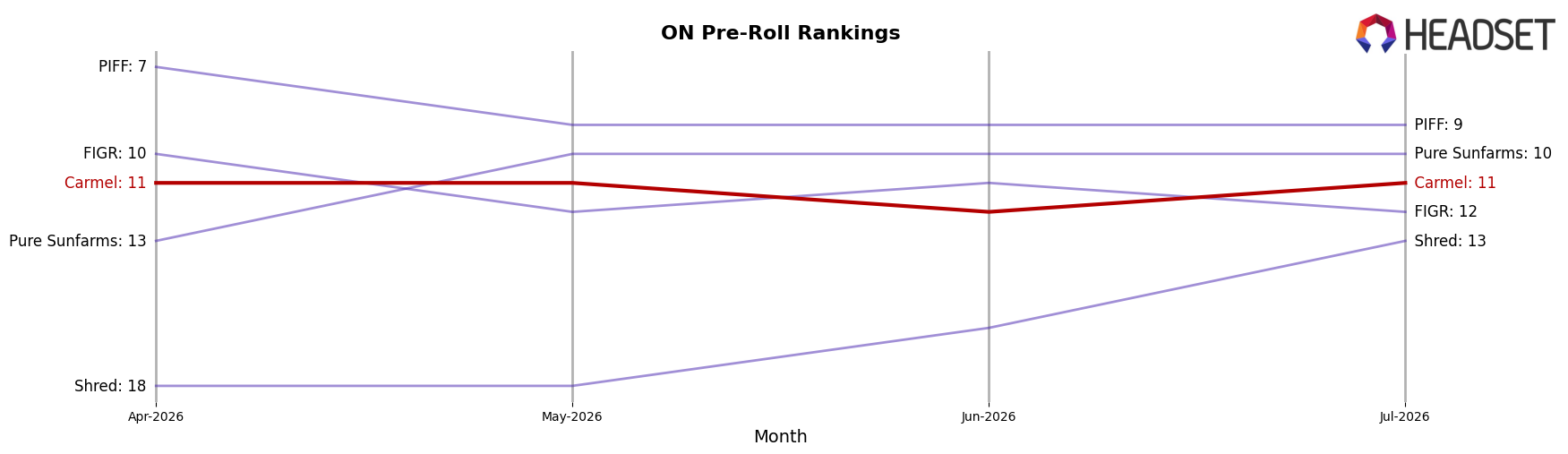

Carmel sits at rank #11 in ON Pre-Roll for July 2026, down 1 position year over year from #10, and flat versus April 2026 at #11; this compares with Back Forty / Back 40 Cannabis holding #1 after climbing from #2 year over year and General Admission slipping from #1 to #2 alongside a 23.2% sales decline, while Carmel’s trajectory also trails its historical peak of #6 from September 2024 by 5 ranks and lags the upward moves of Spinach rising from #14 to #5 with 65.3% sales growth; taken together, the flat three-month position at #11 and the one-rank YoY drop imply share is consolidating below the top 10 unless Carmel re-accelerates to close the five-rank gap back to its prior peak.

Notable Products

Animal Face Pure Live Resin Cartridge (1g) posted the standout move in July 2026 with +54.96% MoM, lifting it to rank 2, while Animal Face Temple Ball Hash (2g) also surged +51.95% MoM into rank 7. Animal Face Pre-Roll 3-Pack (1.5g) grew +16.93% MoM to hold rank 1, and Animal Face Pre-Roll 14-Pack (7g) advanced +19.63% MoM at rank 3, indicating that pre-rolls occupy four of the top ten and concentrate share at the top of the lineup. Big Apple Pure Live Resin Cartridge (1g) added +10.18% MoM at rank 6 versus a -4.06% MoM dip for Mai Tai X Jungle Cake Pre-Roll 3-Pack (1.5g) at rank 8, showing that gains are centered in flagship Animal Face SKUs rather than spread evenly across flavors. The pattern implies Carmel is consolidating around the Animal Face platform with momentum in Vapor Pens and flagship pre-rolls, suggesting a tilt toward fewer, higher-velocity formats rather than broad flavor proliferation.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.