May-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

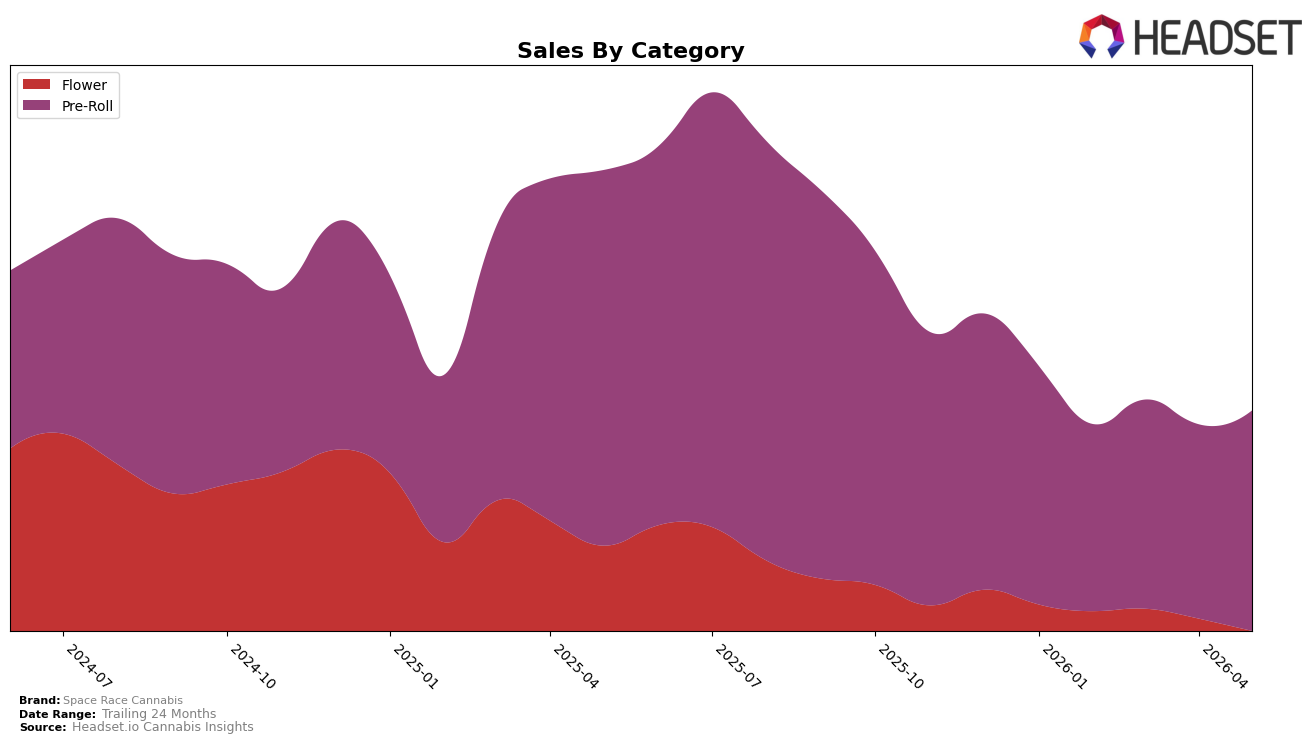

Space Race Cannabis concentrated 79.80% of May 2026 sales in Pre-Roll while Flower held 20.20%, with Pre-Roll up 9.72% month over month but down 34.50% year over year and Flower down 14.17% month over month and down 53.35% year over year; alongside a -4.45% average price change year over year and an overall brand sales change of -39.44% year over year, this mix points to reliance on a single category for volume. With Pre-Roll ranked 6 in Saskatchewan and the brand’s 24‑month sales down 30.15%, the combination of rising Pre-Roll momentum month over month and contracting Flower suggests the brand is leaning into price-accessible, repeatable formats to offset annual declines.

The tilt toward Pre-Roll at 79.80% share and its 9.72% month‑over‑month lift, versus Flower’s 20.20% share and 14.17% month‑over‑month drop, implies Space Race Cannabis is competing on convenience and frequency rather than premium basket builders, reinforced by a -4.45% average price change year over year and a Pre-Roll position of rank 6 in Saskatchewan. This pattern implies near‑term share stability will depend on sustaining Pre-Roll velocity while selectively pruning or repositioning Flower, because the current configuration trades year‑over‑year depth (-34.50% in Pre-Roll and -53.35% in Flower) for month‑over‑month wins in the core format.

Competitive Landscape

Space Race Cannabis sits at rank #9 in AB Pre-Roll for May 2026, down 7 positions from #2 year over year and slipping 3 spots from #6 in February 2026, while its peak rank was #2 in September 2025; meanwhile, General Admission held at #1 year over year despite a -29.3% sales change and Back Forty / Back 40 Cannabis advanced from #7 to #2 with +72.7% YoY sales, indicating that Space Race Cannabis’s descent from a top-3 peak to #9 signals share reallocation toward faster-rising leaders and a need to counter competitors’ upward mobility.

Notable Products

Stargirl Pre-Roll (1g) posted the sharpest move in May 2026 with a 39.36% month-over-month increase while climbing to rank 4, as Voyager Pre-Roll (0.4g) rose 7.77% at rank 3, indicating mid-table momentum shifting toward larger single joints. At the top, Sputnik Pre-Roll (0.4g) grew 4.49% to hold rank 1 and Apollo Pre-Roll (0.4g) slipped 2.37% at rank 2, pointing to a narrowing spread among the leading 0.4g singles. Multipacks concentrated share with Sky Rockets Pre-Roll 20 Pack (8g) up 18.25% at rank 6 and Weedeorites Pre-Roll 20-Pack (8g) up 29.47% at rank 8, even as Astropauts Pre-Roll 10-Pack (4g) fell 5.48% at rank 9 and multipack revenue centered on one $167,698 leader, implying the brand is consolidating demand into higher-count and higher-gram formats rather than expanding breadth across smaller packs.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.